Total Loss vs Repair: Which Is Better for Your Car?

When your car is damaged in an accident, deciding whether to repair it or declare it a total loss depends on several factors:

- Repair Costs vs. Value: If repair costs exceed your car's actual cash value (ACV), it's likely a total loss. State laws and insurance companies use thresholds or formulas to make this determination.

- Safety: Even if repairs are possible, structural or safety concerns (like frame damage or deployed airbags) may lead to a total loss decision.

- Financial Impact: A total loss means you'll receive the ACV minus your deductible. If you're financing or leasing, gap insurance can help cover any remaining balance if the payout is less than what you owe.

- Resale Value: Cars repaired after major damage often lose resale value, while a new replacement vehicle retains its market value.

- Time and Convenience: Repairs can take weeks, while a total loss may require quickly finding a replacement.

Your choice should balance repair costs, safety, and financial considerations. If repairs approach 70% or more of your car's value, or if safety remains a concern, a total loss may be the better option.

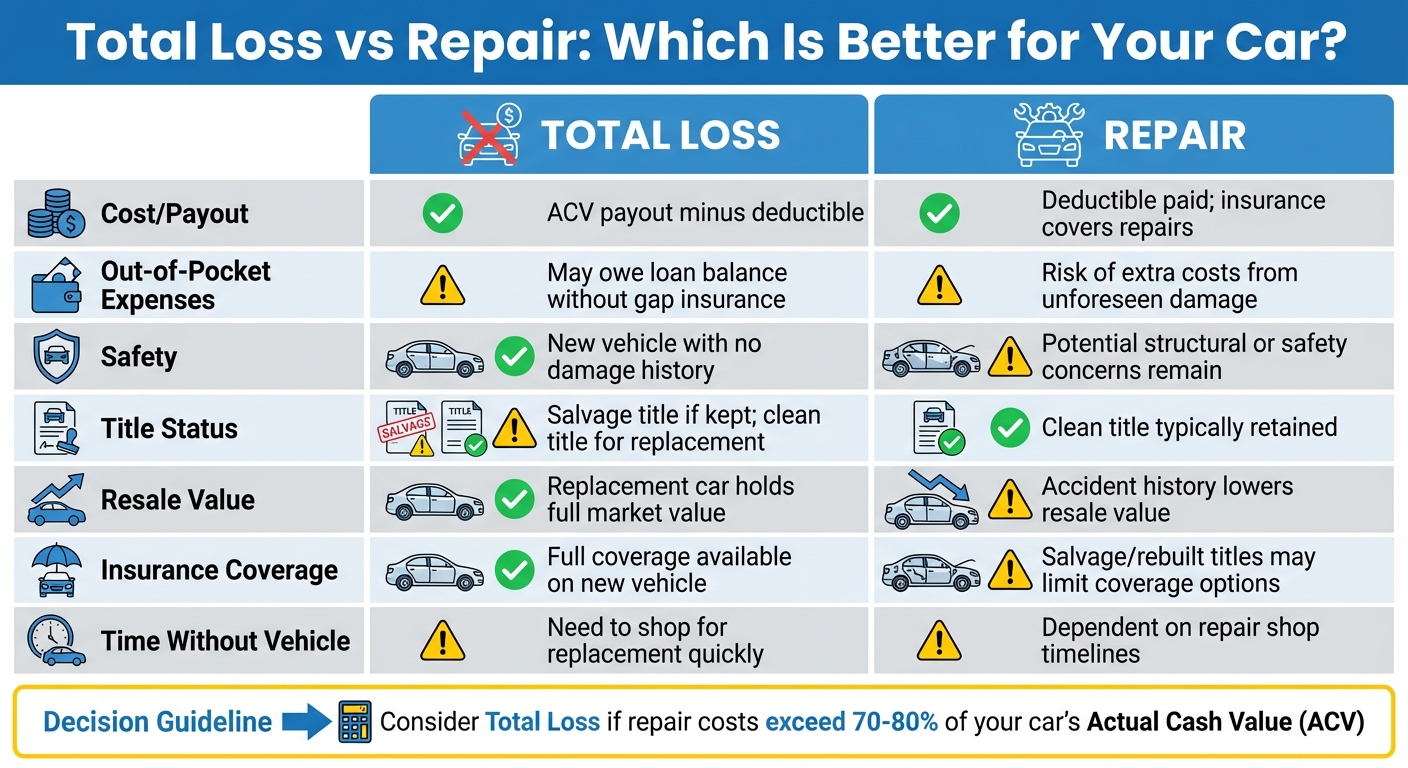

Quick Comparison:

| Factor | Total Loss | Repair |

|---|---|---|

| Cost | ACV payout minus deductible | Deductible paid; insurance covers repairs |

| Safety | New vehicle with no damage history | Potential lingering safety concerns |

| Resale Value | Replacement car retains market value | Accident history lowers value |

| Insurance | Full coverage available | Limited coverage for rebuilt titles |

| Time Without Car | Need to shop for a new car | Dependent on repair timelines |

Deciding between these options depends on your car's condition, financial situation, and long-term needs.

Total Loss vs Repair: Complete Financial and Safety Comparison

What Total Loss and Repair Mean for Your Car

What Total Loss Means in U.S. Insurance

A car is considered a total loss (or "totaled") when the estimated repair costs surpass its actual cash value (ACV) at the time of the accident. Sometimes, even if repair costs are lower than the ACV, a car might still be totaled if it can't be made safe to drive.

Each state has its own total loss threshold (TLT) - the percentage of a vehicle's ACV that, once exceeded, automatically classifies the car as a total loss. For example, Alabama sets its threshold at 75%, Oklahoma at 60%, and Colorado at 100%. In states without a set threshold, insurers use the Total Loss Formula (TLF): a car is totaled if repair costs exceed the difference between its fair market value and salvage value.

Insurance companies sometimes use stricter thresholds than state laws require. This is because initial damage assessments may underestimate hidden or internal damage.

Now, let’s look at what makes a car repairable.

What Makes a Vehicle Repairable

A car is considered repairable when repair costs are less than its ACV and it can be safely restored to working condition. Insurers evaluate several factors, including the extent of the damage, availability of replacement parts, labor costs, and whether the car’s structural integrity remains intact. Safety is a top priority - if critical components like airbags, the engine, or the frame are compromised, repairs may not be feasible. Additionally, hidden damage discovered during the repair process can increase costs, sometimes turning a repairable car into a total loss.

Key Terms: ACV, Salvage Value, and Total Loss Formula

Grasping these key terms can help you better understand how total loss decisions are made.

- Actual Cash Value (ACV): This is the market value of your car right before the accident, factoring in depreciation, mileage, age, and condition. It’s not the same as the car’s original purchase price or the balance left on a loan.

- Salvage value: This is the amount an insurer can recover by selling the damaged car to a salvage yard. Salvage value plays a big role in deciding whether repairs make financial sense.

- Total Loss Formula (TLF): This formula compares repair costs to the difference between the car’s fair market value and its salvage value. If repair costs exceed that difference, the car is declared a total loss. This ensures insurers don’t spend more on repairs than the car is worth after salvage.

How Insurers Decide Between Total Loss and Repair

The Claim and Inspection Process

When you file a claim after an accident, the process starts with an adjuster inspecting your vehicle. They assess both visible and potential hidden damage, documenting everything with photos and detailed notes. From there, they estimate the repair costs by consulting body shops, pricing replacement parts, and calculating labor expenses. This estimate is then compared to your car's Actual Cash Value (ACV) to determine whether repairing it is financially justifiable.

If the repair estimate surpasses your state’s total loss threshold or meets the criteria of the total loss formula, the insurer will likely declare your car a total loss. However, if additional hidden damage is uncovered during a deeper inspection, repair costs might rise, turning a repairable car into a total loss instead. These evaluations, combined with state-specific rules, ultimately guide the insurer’s decision.

State-Specific Rules and Formulas

Where you live plays a big role in whether your car is repaired or declared a total loss. States follow one of two methods: the Total Loss Threshold (TLT) or the Total Loss Formula (TLF). The TLT sets a percentage of your car’s ACV as the tipping point - if repair costs exceed that percentage, the car is totaled. Meanwhile, in states without a fixed threshold, the TLF is used. Under this formula, a car is totaled if repair costs exceed the difference between its fair market value and its salvage value.

Insurers must follow these state-specific guidelines, but they may also enforce stricter internal policies to account for unexpected repair complications. This ensures they remain compliant while managing potential risks during the repair process.

Safety and Structural Factors

Cost isn't the only factor insurers consider - your car’s safety and structural integrity are equally important. Even if repair costs are within limits, your car might still be declared a total loss if it can’t be safely restored. Issues like frame damage, compromised structural integrity, or deployed airbags often lead to a total loss decision because they directly affect the vehicle’s safety.

"Also, insurers total a car that they consider would still be unsafe to drive even after making all the needed repairs. They may also declare it a total loss if it would be unsafe to drive, even if you fix it." - Kelley Blue Book

Insurers also weigh the legal risks of repairing a vehicle that could still be unsafe. If a repaired car is involved in another accident due to lingering structural issues, they could face liability. This concern over safety and potential legal exposure heavily influences their final decision.

Comparing the Financial Impact: Total Loss vs Repair

How Total Loss Payouts Are Calculated

When your vehicle is declared a total loss, the insurance company will pay out its Actual Cash Value (ACV) - essentially, the market value of your car right before the accident. This isn’t based on what you originally paid but rather takes into account depreciation due to factors like age, mileage, wear and tear, and prior accidents. Insurers also research comparable vehicles in your local market to determine this value. Once the ACV is calculated, your deductible is subtracted from the payout. For example, if your car's ACV is $15,000 and your deductible is $500, you’ll receive $14,500.

It’s worth noting that new cars lose value quickly - typically about 20% in the first year, and 15–25% annually after that. If you feel the insurer’s valuation is too low, you can challenge it. Supporting evidence such as maintenance records, photos, or videos of your car’s condition before the accident, and documentation of upgrades (like the original window sticker) can strengthen your case. Tools like Kelley Blue Book or local dealer listings can also help you prove your car’s worth.

Now, let’s explore how financing can complicate this process.

Loan and Lease Considerations

If you’re still paying off your car loan or lease, a total loss can create additional financial hurdles. Insurance payouts are typically sent directly to your lender or leasing company. But here’s the catch: if the ACV of your car is lower than what you still owe - a situation called being "upside down" on your loan - you’ll need to cover the difference out of pocket.

This is where gap insurance can be a lifesaver. Gap insurance bridges the gap between the ACV payout and your remaining loan or lease balance. Costing around $20 to $40 per year, this coverage can save you thousands if your car is totaled. It’s especially important if you made a small down payment - or none at all - when buying your car.

For instance, in March 2023, a driver in Arizona faced this exact situation. Their 2023 Toyota Corolla was declared a total loss after an accident. The insurance company took 10 weeks to process the claim and offered a payout based on the ACV, which fell significantly short of the remaining loan balance. Without gap insurance, the driver had to pay the difference out of pocket.

Finally, let’s examine how ownership and title status come into play after a total loss.

Ownership and Title Status

When you accept a total loss payout, the insurance company typically takes ownership of your vehicle and reports it to the DMV. At this point, the car usually receives a salvage title, indicating it has been totaled. However, in some states, you can choose to keep the car instead. If you go this route, the insurer will deduct the salvage value from your payout.

Holding onto a totaled car comes with its own set of challenges. You’ll be responsible for repairs, and the vehicle must pass state inspections to receive a rebuilt title. Even then, getting comprehensive or collision coverage can be tough. Many insurers will only offer liability coverage for salvaged or rebuilt-titled vehicles.

"Some insurance companies only insure salvaged or rebuilt-titled vehicles for liability only. They wouldn't cover it for comprehensive or collision coverage because it's difficult to assess the current condition of the vehicle." - Josh Damico, Vice President of Insurance Operations at Jerry

Even if you decide to repair the vehicle instead of accepting a total loss payout, the accident history can still hurt its resale value. This is known as diminished value - a reduction in the car’s worth simply because it’s been in an accident. Unfortunately, this financial hit can stick with the car, no matter how well the repairs are done.

When Total Loss or Repair Makes More Sense

Key Factors to Consider

If you're dealing with an older car with high mileage, its lower market value often means it’s more likely to be declared a total loss if repair costs come close to its worth. On the other hand, a newer car with fewer miles might still hold enough value to justify repairs - especially if the damage is minor.

The severity of the damage and safety concerns are just as important. If critical systems are heavily damaged, going with a total loss is often the safer choice. Structural damage, in particular, can compromise the vehicle’s safety, making replacement a more sensible option.

Your financial situation also plays a big role. When repair costs hit 70-80% of your car’s Actual Cash Value (ACV), it’s a strong indicator that the car might be better off totaled. If you’re still paying off a loan, consider whether you have gap insurance to cover the difference between the insurance payout and your loan balance. Without it, you could face out-of-pocket costs. It’s also worth noting that even if repairs are completed, an accident history can lower your car’s resale value down the road.

Reliability is another factor to weigh. A car that’s been through major repairs might not perform as it once did. As McCready Law explains, "A car which requires a significant amount of repairs is never the same". You could face higher maintenance costs and reduced dependability, which might make replacing the car a smarter long-term decision.

Here’s a quick comparison of the key factors to help you decide:

Comparison Table: Total Loss vs Repair

| Factor | Total Loss | Repair |

|---|---|---|

| Payout/Cost | Insurance pays ACV minus deductible. | Deductible paid; insurance covers repair costs. |

| Out-of-Pocket | Could owe on loan balance without gap insurance. | Risk of extra costs from unforeseen damage. |

| Safety | New vehicle with no damage history. | Potential structural or safety concerns remain. |

| Title Status | Salvage title if you keep the car; clean title for a replacement. | Clean title typically retained. |

| Resale Value | Replacement car holds full market value. | Accident history may lower resale value. |

| Insurance Coverage | Full coverage available on a new vehicle. | Salvage or rebuilt titles may limit coverage options. |

| Time Without Vehicle | Need to shop for a replacement quickly. | Dependent on repair shop timelines. |

How Collision Help | Nationwide Accident Help Can Assist

Collision Help | Nationwide Accident Help takes the guesswork out of the process. Their team offers a free 24-hour evaluation - just upload photos of the damage through their secure platform. They’ll review your claim, break down insurance offers, and guide you toward the most cost-effective solution.

sbb-itb-6a9d141

Navigating the Claims Process

Reviewing Estimates and Offers

After filing your claim, the next step is to carefully examine the estimates and offers provided by your insurer. Start by requesting the full valuation report that explains how your car's Actual Cash Value (ACV) was calculated. Insurers often rely on valuation sources that result in lower figures. To ensure you're being treated fairly, conduct your own research by comparing prices for similar vehicles in your local market.

Match the insurer’s settlement offer with these market values to see if it aligns. If your car has new tires, upgraded parts, or custom additions like aftermarket rims, make sure these are accounted for in the offer. Provide any receipts or documentation for these improvements. Even maintenance records or the original window sticker can help support your case by showing the car’s condition and upgrades. When seeking repair estimates, gather multiple quotes. A lower repair estimate might keep the damage below the threshold for declaring the car a total loss.

Taking the time to review these estimates thoroughly can help you avoid disputes and make the claims process smoother.

Handling Disputes with Insurers

If the settlement offer seems too low, challenge it with documented evidence. Submit a counteroffer supported by your research, market comparisons, and independent appraisals. Josh Damico, Vice President of Insurance Operations at Jerry, advises:

"If you can't resolve it with the adjuster, you can go out and hire a private appraiser."

While hiring an appraiser comes with an out-of-pocket cost, their assessment can give you a strong advantage in negotiations.

If the insurer remains unwilling to adjust their offer, review your policy for an "appraisal clause", which outlines steps for resolving disputes. You can also file a complaint with your state’s insurance regulatory department or consult an attorney who specializes in insurance claims.

When all else fails, professional assistance can help you pursue a fair outcome.

How Collision Help | Nationwide Accident Help Supports You

Expert guidance can make a big difference during this challenging process. Collision Help | Nationwide Accident Help offers free damage evaluations and personalized advice. Their team specializes in resolving disputes, ensuring the insurer’s offer is fair, uncovering hidden costs in repair estimates, and helping you decide whether to repair your car or accept a total loss payout. They provide a clear roadmap to help you move forward, whether through better negotiations or making the best decision for your situation.

Is it Better to Get Your Car Totaled Out or Fixed?

Conclusion: Making the Right Choice for Your Car

Deciding between repairing your car or accepting a total loss payout boils down to a mix of financial practicality, safety concerns, and your personal circumstances. Start by weighing the repair costs against your car’s actual cash value. Typically, if repair expenses hit 50–70% or more of the car’s value, opting for a total loss payout often makes more financial sense. Plus, even with extensive repairs, a car may never drive or feel the same again.

Safety should always come first. Significant frame damage or deployed airbags are red flags that repairs might not restore the car’s full structural integrity. A compromised vehicle could pose risks to you and your passengers, no matter how thorough the repairs.

Don’t overlook your financial obligations, especially if you owe more on a loan or lease than the car’s value. In such cases, GAP insurance can save you from covering the difference out of pocket. Additionally, keeping a totaled car means dealing with a salvage or rebuilt title, which can make getting insurance or reselling the car much more challenging.

Navigating the claims process can be tricky, but having expert guidance can make a world of difference. Collision Help | Nationwide Accident Help offers free evaluations and professional advice to help you choose the option that best fits your needs and protects your interests.

FAQs

How can I tell if my car should be repaired or declared a total loss?

To figure out whether your car can be repaired or is considered a total loss, you’ll need to compare the estimated repair costs to its actual cash value (ACV). If the repair costs exceed the ACV or hit your state’s total loss threshold, your car will likely be classified as a total loss.

It’s worth noting that every state has its own rules for determining a total loss, so checking local regulations is essential. Your insurance company will evaluate the situation and help you navigate the process based on these guidelines.

How does safety influence the decision between repairing your car or declaring it a total loss?

Safety plays a crucial role when deciding whether to repair a car or consider it a total loss. If the damage affects the vehicle's structural integrity - like a bent frame or deployed airbags - repairs might not be enough to make it safe to drive again. In such cases, declaring the car a total loss is often the more sensible and safer option.

Even when repairs are technically possible, they need to meet strict safety standards to ensure the vehicle can protect you in future accidents. If there's any uncertainty about the car's ability to perform safely after being repaired, it’s always wiser to put safety ahead of cost.

What does gap insurance cover if my car is totaled?

Gap insurance is a financial safety net if your car is totaled in an accident. It steps in to cover the gap between your car’s actual cash value (ACV) - essentially what it’s worth at the time of the loss - and the remaining amount you owe on your auto loan.

Without this coverage, you could end up owing money on a car you can no longer use, particularly if its value has dropped significantly. Gap insurance ensures you’re not left paying for a vehicle that’s no longer drivable.