Car Insurance Claim Denied: 5 Reasons Why

Having your car insurance claim denied can be frustrating, but it’s often due to common issues. Here’s a quick breakdown of the top reasons why claims get rejected and how to avoid them:

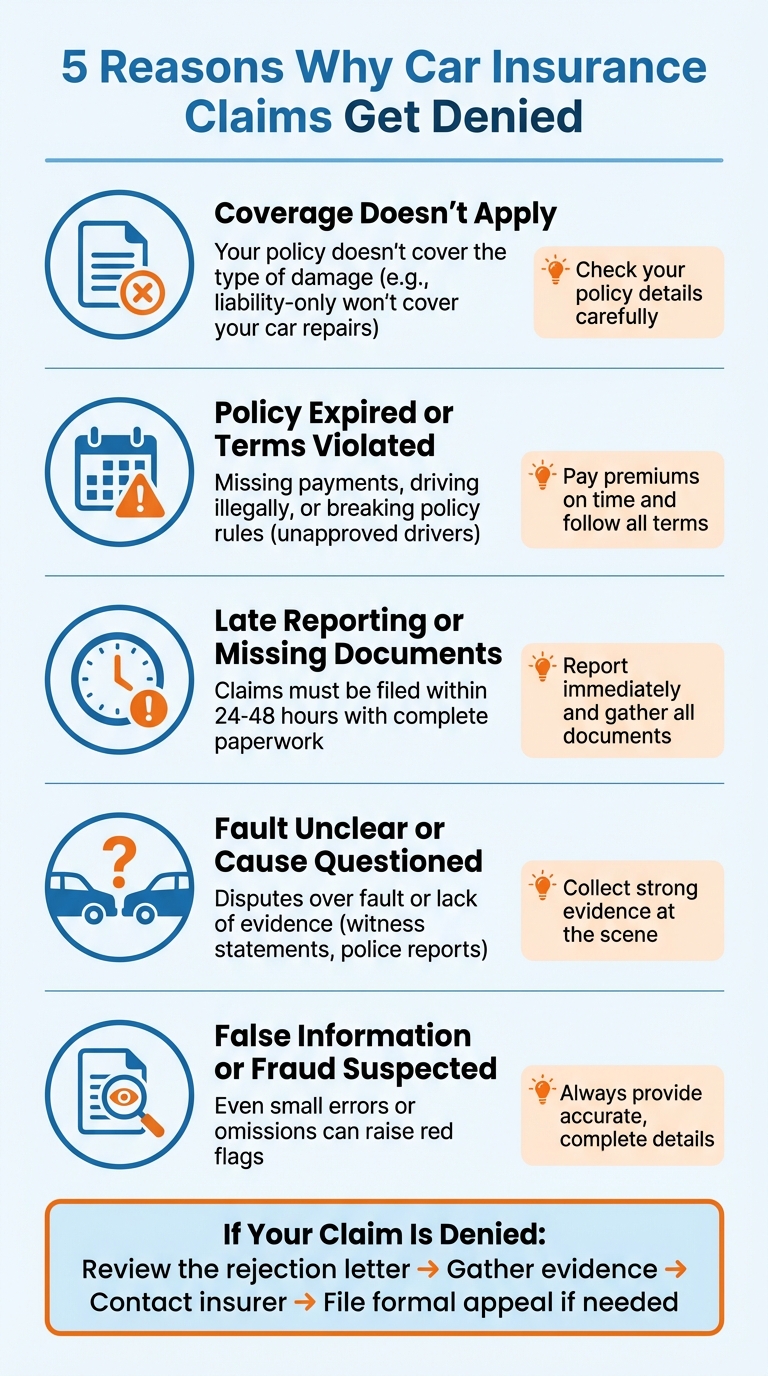

- Coverage doesn’t apply: Your policy may not cover the type of damage (e.g., liability-only policies won’t cover your car’s repairs). Check your policy details carefully.

- Policy expired or terms violated: Missing payments, driving illegally, or breaking policy rules (like letting an unapproved driver use your car) can lead to a denial.

- Late reporting or missing documents: Claims often need to be filed within 24–48 hours with complete paperwork, such as police reports and photos.

- Fault unclear or cause questioned: Disputes over fault or lack of evidence (like witness statements) can complicate claims.

- False information or suspected fraud: Even small errors or omissions in your claim can raise red flags, so always provide accurate details.

To challenge a denial: Review the rejection letter, gather evidence, and contact your insurer for clarification. If needed, file a formal appeal or seek legal advice. Staying informed about your policy and acting promptly can help avoid these issues.

5 Common Reasons Car Insurance Claims Get Denied

Best tips for avoiding auto insurance claim denials

1. The Type of Coverage Doesn't Apply

Insurance claims often get denied when the damage falls outside the scope of your policy. Car insurance policies clearly outline what they cover - and, just as importantly, what they don't.

For example, if you only carry liability insurance - the bare minimum required by law - your insurer won’t pay for repairs to your vehicle. Liability coverage only applies to damages you cause to others. To cover your own car, you'd need collision coverage for accidents or comprehensive coverage for events like theft or natural disasters. It’s always a good idea to double-check your policy to understand exactly what’s included.

Here’s how gaps in coverage can impact your claim:

"Every policy is unique. Your policy likely has many limitations and exclusions. The insurance company may claim you are seeking compensation for damage that occurred because of an excluded cause." - Ged Lawyers

Another common issue is damage exceeding your policy limits. In California, for instance, the minimum property damage liability is $5,000, but modern repair costs can easily surpass that amount. Experts often suggest opting for $50,000 to $100,000 in property damage coverage to avoid being underinsured. Without this extra protection, you could find yourself paying out of pocket for the difference.

Additionally, standard policies often don’t cover exotic, customized, or classic cars. As Karen Axelton from Experian explains, "Exotic cars, customized or classic cars may require specialized auto insurance". If you own a unique vehicle, you’ll need a tailored policy to ensure you’re fully protected and avoid claim denials.

2. Policy Expired or Terms Were Violated

Sometimes, claim denials stem from issues beyond coverage limits - internal compliance problems can also play a role.

If your policy wasn’t active at the time of the accident, your claim will be denied automatically. This can happen if you missed premium payments and your policy lapsed. Without active insurance, the company won’t cover any accident-related claims.

Driving without insurance isn’t just risky - it’s illegal in every state. Beyond a denied claim, you might face fines, license suspension, vehicle impoundment, or even jail time. If you’re uninsured and cause an accident, you could be personally responsible for covering significant damages.

Violating policy terms can also lead to problems. Actions like driving under the influence, using an expired or revoked license, letting an unapproved driver use your car, or engaging in reckless behavior - such as speeding, running red lights, or texting while driving - can all result in a denied claim.

Even poor vehicle maintenance can be an issue. If the accident was caused by something like faulty brakes or neglected repairs, your insurer could reject the claim.

To avoid these pitfalls, take proactive steps. Pay your premiums on time - setting up autopay can help. Keep track of policy renewal dates and ensure all drivers are properly listed on your insurance. Regularly maintain your vehicle to prevent issues that could jeopardize a claim. If you receive a cancellation notice, review it immediately and resolve any problems. Following these practices not only keeps your coverage valid but also protects your rights in the event of an accident. Staying compliant with your policy terms is crucial to avoiding unnecessary complications.

3. Claim Reported Too Late or Documents Missing

When it comes to filing an insurance claim, timing and proper documentation can make or break your case. Even if your policy is active and within coverage limits, missing a deadline or failing to provide the right paperwork could lead to a denial.

Most insurance policies require claims to be filed within 24–48 hours of an incident. It's crucial to check your policy's specific reporting requirements to avoid any automatic denials.

"Each and every auto insurance policy has certain regulations about when a vehicle collision must be reported to the insurer. If you do not report the incident within the given timeframe, your accident claim will be denied by the insurer." - Siegfried & Jensen

Delays in reporting can hinder the insurer's ability to investigate properly and may even cast doubt on whether your injuries are directly related to the accident.

Another common issue is incomplete or inaccurate documentation. Key items like medical records, accident photos, police reports, witness statements, repair estimates, and receipts are often required. Missing any of these can result in a denied claim.

To avoid these pitfalls, act quickly. File your claim as soon as possible. Take photos of the scene, contact the police for an official report, gather witness information and insurance details, and seek medical attention right away. Early medical records can help confirm that your injuries are tied to the accident. Keep copies of everything you submit to the insurer to ensure nothing gets lost in the process.

sbb-itb-6a9d141

4. Fault Is Unclear or Cause Is Questioned

When drivers offer conflicting stories about an accident, it can throw a wrench into the claims process. For example, one driver might accuse the other of running a red light, while the other argues speeding was the real issue. These disagreements make it harder to determine fault, especially when key evidence is missing.

Without crucial records - like police reports, witness statements, or photos - insurance companies often can't figure out who's at fault, which can lead to denied claims. This problem becomes even trickier in hit-and-run cases, where proving the other driver's involvement is particularly challenging.

Your own actions can also play a big role in whether your claim gets approved. Driving under the influence, using a phone while driving, or even having an invalid license can lead to outright denials. On top of that, neglecting vehicle maintenance - like ignoring faulty brakes - could shift the blame squarely onto you.

A legal expert points out:

"If the reason for the collision was avoidable but you did not take proper action to prevent it from happening, or your actions somehow contributed to the accident, your auto insurance claim may be denied by the insurer." - Siegfried & Jensen

In states with contributory negligence laws, being even 1% at fault could mean you’re not entitled to any compensation. Insurance companies might also try to pin more blame on you to lower their payout, even if their policyholder shares some fault. That’s why collecting strong evidence right from the start is absolutely essential to safeguarding your claim.

5. False Information or Fraud Suspected

Insurance companies take fraud very seriously, and even small inaccuracies can lead to an immediate claim denial. This includes both intentional falsehoods and innocent mistakes that might raise suspicions. If an insurer finds any false information on your claim or policy application - whether it's lying about details, leaving out key facts, or submitting fake documents - they can reject your claim outright.

And it doesn’t stop there. The repercussions of providing false information can go beyond just losing your claim. As Brandon J. Broderick, Attorney at Law, points out:

"If the insurance company discovers you made false information on your claim or policy, that may be a reason for them to deny your claim. When filing a claim, all information should be correct to the best of your knowledge. Falsifying information is illegal and can lead to more trouble."

Insurers also keep a sharp eye on various forms of misrepresentation to assess the validity of a claim. Fraud can take many shapes. For instance, they look for staged accidents, intentional damage caused by arson or vandalism, or any material misrepresentation during the policy application process. This might include hiding previous accidents, misreporting how a vehicle is used, or providing incorrect details about your driving history. Even honest errors, like small paperwork mistakes or incomplete filings, can raise red flags and potentially lead to a denial if they meet certain legal thresholds.

April Collins, Founder of Collins Law, LLC, emphasizes the importance of honesty:

"Always tell the truth in your applications and claim reports, and don't embellish, exaggerate, or speculate. Deliberate post-loss misrepresentations, and even some honest misstatements, can lead to a denial."

To avoid any issues, make sure every detail on your claim is accurate and complete before submission. Keep thorough records, including photos, receipts, maintenance logs, and medical documents. Respond promptly to any requests from your insurer, and don’t hesitate to ask for clarification if something is unclear. In the end, being precise and upfront is your best protection against fraud-related complications.

What to Do If Your Claim Is Denied

Getting a denial letter from your insurance company might feel like a dead end, but it doesn’t have to be. You have options to challenge the decision and potentially turn things around.

Start by carefully reading the denial letter and comparing it with your policy. This will help you understand why your claim was rejected. Next, gather all relevant documents that support your case. These might include police reports, medical records, photos, repair estimates, witness statements, and receipts - anything that backs up your claim.

Once you’ve collected your documents, reach out to your insurance company directly. Ask for a detailed explanation of their decision. Sometimes, a simple conversation can resolve misunderstandings. If that doesn’t work, it’s time to take the next step: filing a formal appeal.

When submitting your appeal, make sure it’s in writing and includes all the supporting documents you’ve gathered. As Ged Lawyers advises, don’t hesitate to seek legal guidance if you’re unsure about the process. Additionally, you can file a complaint with your state insurance department. Insurers are legally required to act in good faith, and state resources are available to assist consumers facing disputes.

For personalized assistance, you can also reach out to Collision Help | Nationwide Accident Help, which offers free 24-hour evaluations to guide you through the process.

Attorney Scott Callahan offers this straightforward advice:

"If you feel your claim was unjustly denied, don't hesitate to challenge the decision or seek legal advice."

Handling a denial can be overwhelming, but having professional support early on can make a big difference in achieving a favorable outcome.

Conclusion

We've covered the typical pitfalls and shared practical tips to help you navigate the tricky world of claim denials. Recognizing the most common reasons - incorrect coverage type, policy violations, delayed reporting, unclear fault, and suspected fraud - can help you take steps to avoid these issues altogether.

Start by familiarizing yourself with your insurance policy. Know what’s covered, what’s excluded, and any limits that apply. Stay on top of your premium payments and review your policy details regularly. If an incident occurs, report it immediately to avoid complications. Seeking prompt medical attention is also crucial - it helps establish a clear link between your injuries and the event.

Good documentation is your best ally. Keep photos, witness accounts, official reports, and medical records organized and accessible. And remember, honesty is non-negotiable. Misrepresenting information not only risks a denial but could also lead to fraud allegations.

FAQs

What can I do if my car insurance claim is denied?

If your car insurance claim gets denied, the first step is to carefully go through the denial letter. This will help you pinpoint the exact reason for the rejection. Next, gather any missing or additional evidence to strengthen your case - think photos, receipts, or even witness statements. Once everything is in order, reach out to your insurance provider to request a reconsideration or formally appeal the decision.

If your efforts don’t lead to a resolution, it might be time to seek advice from a lawyer who specializes in insurance claims. In some situations, mediation or legal action could be necessary to challenge the denial. Staying organized and proactive can make a big difference in resolving the issue in your favor.

How can I make sure my car insurance covers potential damages?

To make sure your car insurance has you covered for any potential damages, start by thoroughly reviewing your policy. Take a close look at the coverage limits, exclusions, and any optional add-ons you might need, like comprehensive or collision coverage.

Keep your policy documents well-organized, and if an accident happens, report it to your insurer as soon as possible to prevent unnecessary delays. If your circumstances change - like buying a new car or moving to a new address - let your insurance company know immediately. For extra confidence, work with your insurance agent to tailor your policy to match your unique needs and ensure you’re fully protected.

What documents do I need to prevent my car insurance claim from being denied?

Having proper documentation is key to making sure your car insurance claim goes through without a hitch. Here’s what you’ll need to have ready:

- Police report: This document provides an official account of the incident.

- Photos: Capture the accident scene, vehicle damage, and any other details that may be important.

- Medical records: If there were injuries, include diagnoses and treatment details.

- Eyewitness statements: These can help back up your version of events.

- Repair estimates or receipts: Show the costs related to fixing your vehicle.

Providing thorough and accurate information can greatly improve the chances of your claim being approved.