What to Do After a Car Accident: 7 Steps to Take

If you're in a car accident, the steps you take immediately after can protect your safety, health, and legal rights. Here's a quick guide to handle the situation effectively:

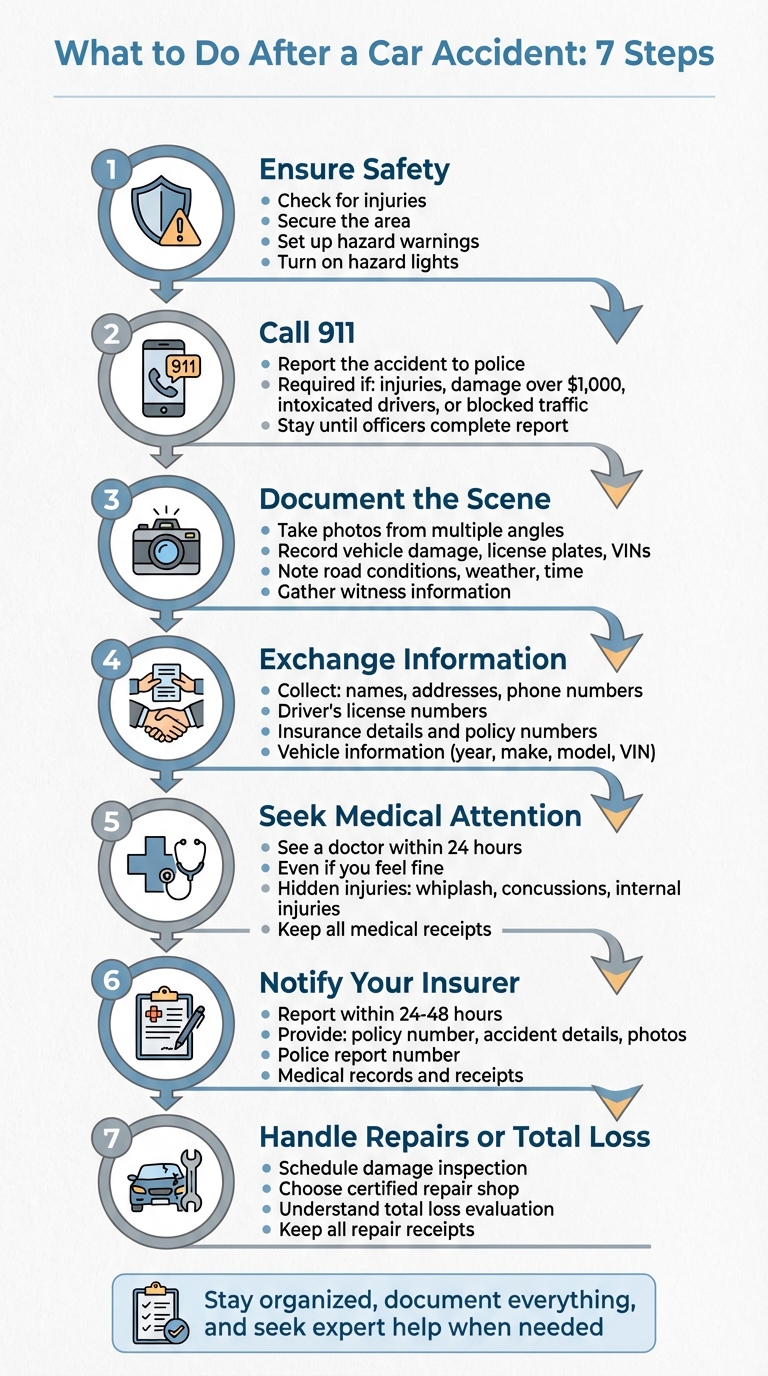

- Ensure Safety: Check for injuries, secure the area, and set up hazard warnings.

- Call 911: Report the accident to the police, especially if injuries or significant damage occur.

- Document the Scene: Take photos, record details, and gather witness information.

- Exchange Information: Share and collect contact, insurance, and vehicle details with other drivers.

- Seek Medical Attention: Even if you feel fine, see a doctor to identify hidden injuries.

- Notify Your Insurer: Report the accident promptly and provide all necessary documentation.

- Handle Repairs or Total Loss: Work with your insurer to address vehicle damage or replacement.

7 Essential Steps to Take After a Car Accident

What To Do RIGHT AFTER a Car Accident?

Step 1: Check for Safety and Injuries

Start by assessing the situation calmly. Look around for any immediate hazards - like oncoming traffic, fire, or leaking fluids from damaged vehicles - that could make the scene more dangerous. Your first priority is to secure the area and address any urgent risks.

Look for Immediate Dangers

Turn on your hazard lights to alert other drivers. If your car is blocking traffic but still drivable, carefully move it to the side of the road. However, if it's unsafe or you're injured, stay where you are and move away from any immediate threats. Use items from your emergency kit - like road flares, reflective triangles, or cones - to warn approaching drivers and reduce the risk of additional accidents.

Check Everyone for Injuries

Once the scene is secure, check yourself and others for injuries. Look for visible signs like bleeding, bruising, or difficulty breathing. If someone is unresponsive or showing serious symptoms, call 911 right away. Avoid moving anyone who appears seriously hurt unless there's an immediate danger, such as a fire, that leaves no other choice. Moving them unnecessarily could make their injuries worse.

"Appropriate medical care for people injured in a crash to prevent their injuries from becoming fatal is critical." - U.S. Department of Transportation

Keep in mind that not all injuries are obvious right away. Conditions like whiplash, concussions, or internal injuries can be masked by adrenaline. Even if you feel fine, it's a good idea to see a doctor within 24 hours to rule out any hidden issues.

Set Up Safety Warnings

After checking for injuries, focus on alerting other drivers. Set up flares, cones, or reflective triangles behind your vehicle to make the scene more visible. If you're in a risky situation - like heavy traffic, poor weather, or an unstable vehicle - stay inside your car with your seatbelt on until professional help arrives.

Step 2: Call Police and Record the Scene

Once everyone is safe, it’s time to document the accident. This involves contacting law enforcement and gathering evidence to support your claim.

When to Call the Police

Dial 911 in the following situations:

- Someone is injured

- Property damage is over $1,000

- A driver seems intoxicated

- Vehicles are blocking traffic

- A driver leaves without sharing information

- Public property, like street signs or fire hydrants, is damaged

A police report serves as an official, unbiased account of the accident. This can be critical if the other driver denies responsibility or lacks insurance.

"The best and easiest way to ensure you are in compliance with the law is to call 911 after any accident. Even if it is minor and you do not believe you are required to call, it is always better to err on the side of caution when it comes to legal matters." - Liao Firm

When you call 911, give them your exact location, a brief description of what happened, the number of vehicles involved, any injuries, and whether traffic is blocked. Stay on the scene until the officers finish their report - leaving too soon could lead to legal issues. Before you go, ask for a copy of the report for your records.

Once the police have arrived, turn your attention to collecting your own evidence.

Take Photos and Notes of the Scene

Grab your phone and take clear pictures from multiple angles. Include details like:

- Vehicle damage (both close-ups and wide shots)

- License plates and VINs (Vehicle Identification Numbers)

- Skid marks, broken glass, and debris

- Vehicle positions on the road

- Road conditions, weather, and lighting

- Traffic signs, signals, or other relevant surroundings

Make sure to note the date, time, and exact location. If there are witnesses, ask for their names and contact information.

Write Down What Happened

As soon as possible, write a detailed account of the accident. Stick to the facts - where you were going, what you saw, and how the collision happened. Avoid guessing about details you didn’t directly observe. When speaking with the police, provide a factual statement but avoid admitting fault or apologizing. These statements could be used against you later during the claims process.

Step 3: Exchange Information with Other Drivers

Once you've documented the scene, the next step is to share and collect information with everyone involved. In many states, like California, this is not just a good idea - it’s legally required. Providing accurate details ensures your insurance company has everything they need to process your claim efficiently. Plus, thorough documentation can help avoid disputes about liability later on.

What to Collect from Other Drivers

Start by gathering some essential details from each driver. This includes their full name, address, phone number, and email address. You’ll also need to note their driver's license number, vehicle registration, and license plate number.

For their vehicle, jot down specifics like the year, make, model, color, and the Vehicle Identification Number (VIN). You can usually find the VIN on the dashboard near the windshield or on the driver’s side door jamb.

Make sure to get their insurance company name, policy number, and coverage dates. If they don’t have their insurance card on hand, ask them to send you a photo of it later. When sharing your own details, stick to the basics: your name, vehicle information, VIN, and insurance details. Avoid letting anyone take photos of your driver’s license or registration unless law enforcement specifically asks for it.

Collect Witness Information

Witnesses can provide neutral accounts that might be helpful for your claim. Politely ask for their full name, phone number, email address, and a brief description of what they saw. If possible, record their statement - either by writing it down or using a voice recorder - and ask them to review and sign it for accuracy. Throughout this process, stay calm and courteous, and avoid discussing fault. Leave that determination to the authorities and your insurance provider.

Note Tow Truck and Responder Details

If police are on the scene, make sure to note their names and badge numbers. Also, ask how you can obtain a copy of the police report for your records.

If your car needs to be towed, write down the tow company’s name, the driver’s contact information, and the destination of your vehicle. Don’t forget to get a receipt - this information will be critical for coordinating repairs and retrieving your vehicle through your insurance company.

Step 4: See a Doctor and Keep All Receipts

After documenting the scene and exchanging information, the next priority is taking care of your health.

Get Checked by a Doctor

Even if you feel fine right after the accident, it’s essential to see a doctor as soon as possible. Shock can often mask injuries, and conditions like whiplash, concussions, or internal injuries might not show symptoms immediately.

In the U.S., you have several options for medical care. If you’re experiencing severe symptoms - like chest pain, trouble breathing, or loss of consciousness - head directly to the emergency room. For less urgent issues, an urgent care center can provide a quick evaluation, or you can schedule an appointment with your primary care doctor shortly after the accident. Seeking medical attention promptly not only ensures your well-being but also creates a clear record of how the accident affected your health, which could be critical for your insurance claim.

Save All Accident-Related Expenses

Keep track of every expense tied to the accident. This includes hospital bills, medication receipts, therapy costs, and even small purchases like bandages or over-the-counter pain relievers.

Don’t forget to log transportation costs for medical visits, any additional caregiving or household help you might need, and document lost wages with pay stubs or a letter from your employer. Maintaining a personal injury journal can also be incredibly useful. Use it to record your daily pain levels, mobility struggles, and how the accident has impacted your work and personal life.

"Medical records are more than just notes from your doctor's office. They serve as concrete evidence showing the link between the accident and your injuries." - Rogan Law Firm

These records and receipts will play a key role when it’s time to file your insurance claim.

sbb-itb-6a9d141

Step 5: Contact Your Insurance Company

Once you've completed your medical evaluation and gathered all relevant receipts, the next step is to notify your insurance company. It's important to report the accident as soon as possible. Many insurers require notification within 24 to 48 hours, though some policies may extend this window to seven days.

"Most insurance companies have strict deadlines for reporting accidents, often within 24 to 48 hours." – Brandon J. Broderick, Attorney at Law

What Your Insurer Will Need

When contacting your insurer, be ready to provide key details, including:

- Your policy number

- Vehicle registration details

- Accident specifics (location, date, time, and weather conditions)

- Information about the other driver

- Police report number and details of the responding officers

- Photos, videos, and witness contact information

- Injury details and medical records

Having this information on hand will make the process smoother and quicker.

Understanding the Claims Process

After you report the accident, a claims adjuster will take over your case. Their job is to review all the evidence, such as photos, police reports, and witness statements. They’ll also explain your policy details, including coverage, deductibles, and limits. For example, in New York, insurers generally have 15 days to investigate a claim, while in Florida, the timeline may extend to 30 days.

Stay Organized

To keep the claims process manageable, organize all related documents in one place. This includes communications with your insurer, the police report, photos, medical bills, repair estimates, and receipts. Staying on top of your paperwork now will help you respond quickly to any requests and ensure the process runs as smoothly as possible.

Step 6: Handle Vehicle Repairs and Total Loss

Once your claim has been reviewed, it’s time to address the damage to your vehicle. Understanding how inspections and total loss evaluations work can help you manage repairs with confidence.

How Damage Inspections Work

Your insurance company will arrange for a damage inspection to determine the extent of the repairs needed. This inspection, conducted by a claims adjuster or an approved repair facility, results in an estimate that outlines all necessary repairs. If your vehicle requires major repairs - especially those involving critical safety components - it’s a smart idea to request a post-repair inspection. This ensures the work was done properly and that your vehicle meets safety standards.

When selecting a repair shop, consider choosing one with certifications like I-CAR Gold Class, ASE, or ADAS Calibration. These facilities use manufacturer-approved parts and adhere to strict repair procedures. Keep in mind, you’re not required to use the repair shops recommended by your insurance company. You have the freedom to choose a facility that you trust.

What Total Loss Means

A vehicle is declared a "total loss" when the cost to repair it exceeds its actual cash value (ACV) or a state-specific percentage of its ACV. Additionally, if the vehicle would be unsafe to drive even after repairs, it may also be considered a total loss.

The ACV represents your car’s value before the accident, factoring in depreciation. Insurers calculate this by starting with the replacement cost of your vehicle and subtracting depreciation. They evaluate details like the car’s make, model, year, mileage, and overall condition.

If you believe the insurance company’s total loss valuation or repair estimate is inaccurate, you have the right to challenge it. Insurance companies may undervalue vehicles, so their initial offer could be lower than what your car is truly worth. If you disagree, there are steps you can take to dispute the valuation.

Get Expert Help for Complicated Claims

Navigating damage inspections, repair disputes, or total loss evaluations can feel overwhelming. If you’re dealing with a particularly tricky claim or don’t agree with your insurer’s assessment, services like Collision Help | Nationwide Accident Help can provide expert support. Simply upload photos of your vehicle’s damage through their secure platform, and you’ll receive tailored advice within 24 hours. They’ll give you a clear roadmap for managing your claim and repairs, helping you understand your options - all at no cost for the initial evaluation.

Step 7: Stay in Touch with Your Insurer

Keeping open and precise communication with your insurer can significantly influence the outcome of your claim.

How to Communicate with Your Insurer

Report the accident to your insurance company as soon as possible. Most policies require prompt notification, and delays could jeopardize your claim. When speaking with the claims adjuster, stick to the basics - share details like the time and location of the accident, the people involved, and the extent of the damage. Focus on facts that can be verified.

If you're unsure about what to say, consult an attorney before giving detailed statements. You can also request that future communication be handled in writing for added clarity and documentation.

Keep a detailed record of all interactions with your adjuster. Note dates, times, key discussion points, the name of the person you spoke with, and your claim number. Familiarizing yourself with your insurance policy is also a smart move. It allows you to ask informed questions about the claims process, timelines, and how settlement offers are calculated.

"Remember, insurers are for-profit businesses concerned with protecting their own bottom line. To that end, the primary job of adjusters is to save their company money by denying as many claims as possible within the constraints of the governing policy and law." - Rob Wilhite, The Wilhite Law Firm

Mistakes to Avoid

Even with clear communication, it’s important to steer clear of common missteps. For starters, never admit fault or apologize, even if it feels like the polite thing to do. An apology can be misinterpreted as an admission of guilt. Similarly, avoid exaggerating or downplaying your injuries. If your condition changes later, misrepresenting it could harm your claim. Be consistent in every conversation - contradictions can raise suspicions and weaken your case.

Watch for New Problems

Some injuries don’t show up right away. If you notice delayed symptoms, report them immediately. Keeping a daily journal of how your injury affects you can also be helpful. Document pain levels, missed work, and any limitations on your daily activities - these details could prove invaluable.

Stay organized by creating a dedicated system for all claim-related documents. This should include receipts, photos, medical bills, correspondence, and any other relevant paperwork. Regularly update your records as your claim progresses. Having everything in order will make it easier to handle disputes or reference details when needed. Staying consistent and organized throughout the process can help ensure a smoother resolution.

Documents and Information Checklist

Staying organized with your documents is key to avoiding delays in your claim process. Use this checklist to gather and manage all the necessary paperwork from the accident and its aftermath. As mentioned earlier, your documentation - like photos, witness information, medical records, and receipts - plays a vital role in safeguarding your claim.

At the scene: Double-check that you’ve collected photos, driver information, witness details, and officer reports as described in Steps 2 and 3.

Medical documentation: Hold on to every piece of medical paperwork. This includes doctor visit notes, diagnostic test results, imaging scans, therapy summaries, and discharge instructions. Keep itemized bills from ambulance services, hospitals, doctors, radiology centers, pharmacies, and physical therapists. Don’t forget receipts for prescriptions, medical equipment, and even travel costs for attending appointments.

Financial records: Collect multiple repair estimates from certified shops, along with all repair invoices. Save receipts for towing, rental cars, and any other accident-related expenses, such as parking fees or childcare costs. Additionally, make sure you have your insurance policy, a government-issued photo ID, and the completed claim form ready.

Ongoing documentation: Keep track of every interaction with your insurance company. Note the date, the name of the representative, and the main points discussed during each conversation. Store these records - along with all other documents - in both physical and digital formats. For added security, back up your files in multiple locations.

Take time to periodically review your documents to ensure you haven’t missed anything as your claim moves forward. This proactive approach can save you headaches down the road.

Conclusion

Car accidents can be overwhelming, but following a clear and structured plan helps you take control of both your safety and your claim. As Progressive points out, "Accidents are stressful, but keeping a calm, normal demeanor will help you stay in control of the situation". Similarly, the California Department of Insurance emphasizes that "knowing in advance what to do can help you avoid costly mistakes". These seven steps provide a reliable framework to guide your actions and strengthen your claim.

Taking timely and deliberate steps can make all the difference. By sticking to the facts, documenting everything thoroughly, and avoiding hasty remarks, you protect yourself from missing critical deadlines or accepting settlements that fall short. The immediate aftermath of an accident is crucial - what you say and do matters. As Adam Loewy from Loewy Law Firm explains, "The words you use - especially when you're still shaken or unsure - can end up shaping your entire case". Avoid admitting fault or minimizing injuries, as these actions can impact the outcome of your claim.

If you run into challenges, remember that professional help is just a call away. For complicated claims or repair disputes, Collision Help | Nationwide Accident Help offers expert advice within 24 hours. You can securely upload photos of your vehicle damage and receive a free, personalized roadmap to navigate your claim.

Stay organized, communicate with care, and seek expert assistance when needed. By following these steps - from ensuring everyone's safety to maintaining clear and thorough communication - you protect the integrity of your claim and set yourself up to receive the compensation you deserve.

FAQs

What should I do if my car can't be moved safely after an accident?

If your car is stuck and can't be moved after an accident, your safety comes first. If the area around you is dangerous or heavy traffic makes it risky to step outside, stay inside the vehicle. Call 911 right away to report the accident and request help from emergency services. Only move someone who is seriously injured if there's an immediate threat, like a fire or potential explosion. While waiting for assistance, switch on your hazard lights to warn other drivers and focus on staying calm.

How can I dispute my insurance company’s total loss valuation?

If you think your insurance company’s total loss valuation doesn’t reflect your vehicle’s true worth, you can take steps to challenge it:

- Carefully review their valuation report to see how they calculated the number.

- Collect evidence that supports your car’s actual market value. This might include examples of recent sales for similar vehicles in your area, receipts for repairs, or maintenance records.

- Get an independent appraisal from a professional to back up your claim with an unbiased opinion.

- Submit your evidence to the insurance company, along with a clear explanation of why you believe their valuation is too low.

If these efforts don’t lead to a resolution, you might want to consult a lawyer or reach out to your state’s insurance department for guidance. Staying organized and presenting solid evidence can make a big difference in your case.

What are common hidden injuries to watch for after a car accident?

After a car accident, some injuries might not show up right away. These hidden injuries often include whiplash, concussions, soft tissue damage, back or spine injuries, and even internal injuries. The tricky part? Symptoms can take time to surface.

Watch out for delayed signs like headaches, dizziness, nausea, numbness, or any unexplained pain. These could show up days - or even weeks - after the accident. If you notice any of these symptoms, don’t wait. Getting medical attention quickly is crucial, not just for your health but also to have proper records for your insurance claim.