How Pre-Existing Damage Affects Settlements

Pre-existing damage can lower your insurance payout if not properly documented. Insurers use vehicle history, photos, and inspection reports to differentiate old damage from new. Without evidence, you risk a reduced settlement or claim denial.

Key Points:

- What Counts as Pre-Existing Damage: Scratches, dents, rust, or issues from before the accident.

- Insurer Tactics: Adjusters compare pre- and post-accident photos, use history reports, and apply formulas like "17c" to reduce payouts.

- How to Protect Your Claim:

- Take detailed, date-stamped photos of your car before and after the accident.

- Get expert evaluations to prove the accident worsened prior damage.

- Use independent appraisals to challenge low offers.

Pre-existing damage doesn’t mean you can’t get fair compensation. Document thoroughly, provide evidence, and seek expert help to strengthen your claim.

Get the Most from Your Property Damage Claim After a Car Accident!

sbb-itb-6a9d141

How Pre-Existing Damage Reduces Settlement Amounts

When an insurer discovers that your vehicle had damage before an accident, they might lower your payout - even if the accident caused more harm. Knowing how these evaluations work can help you spot when your claim might be undervalued.

Tactics Insurers Use to Lower Your Claim

Insurance adjusters often dig into your car's history, looking for past accidents or repairs that overlap with the current damage.

Another strategy involves comparing photos. Adjusters may use photos taken when your policy began and compare them with post-accident images to argue that certain dents or scratches were already there. In some states, such as New York, insurers even require a photo inspection when you first get your policy.

One widely used tool is the "Rule 17c" formula. This internal calculation limits the maximum diminished value to 10% of your car's pre-accident worth. Adjusters then apply multipliers based on factors like mileage and damage severity. For instance, a car with 85,000 miles might get a 0.20 mileage multiplier, while vehicles with over 100,000 miles often receive a multiplier of 0.00. These adjustments can significantly reduce your final settlement.

Insurers may also argue that high-quality repairs have restored your car to its original condition, using what's known as the "made whole" defense. Under this reasoning, they claim you haven’t experienced a true financial loss until you sell or trade in the vehicle.

"My claim isn't about the quality of the repairs; it's about the permanent loss in market value due to the accident history." – SnapClaim

A related concept, the "eggshell vehicle" principle, further impacts how settlements are calculated.

The Eggshell Vehicle Principle

This principle, similar to the "eggshell plaintiff" rule in personal injury law, requires insurers to compensate for any worsening of pre-existing damage caused by an accident. For example, if your car had a small dent that became much worse after the crash, the insurer should account for that additional loss in value.

Tort law in most states also mandates that at-fault parties "make the victim whole" by restoring the vehicle's full financial value - not just its physical appearance. Cases like Mabry v. State Farm in Georgia have clarified that owners are entitled to compensation for diminished market value, even after repairs.

"Making you whole means not just fixing the metal, but restoring the financial value of your asset." – Marcus Seneki, Auto Liability Expert, Surety Insights

This legal framework aims to ensure fair compensation for the added loss caused by the accident.

3 Steps to Protect Your Settlement

When pre-existing damage is part of the equation, safeguarding your settlement demands careful preparation and expert guidance. These three steps can help you counteract insurer tactics and secure the compensation you deserve.

Step 1: Document Your Vehicle Before and After the Accident

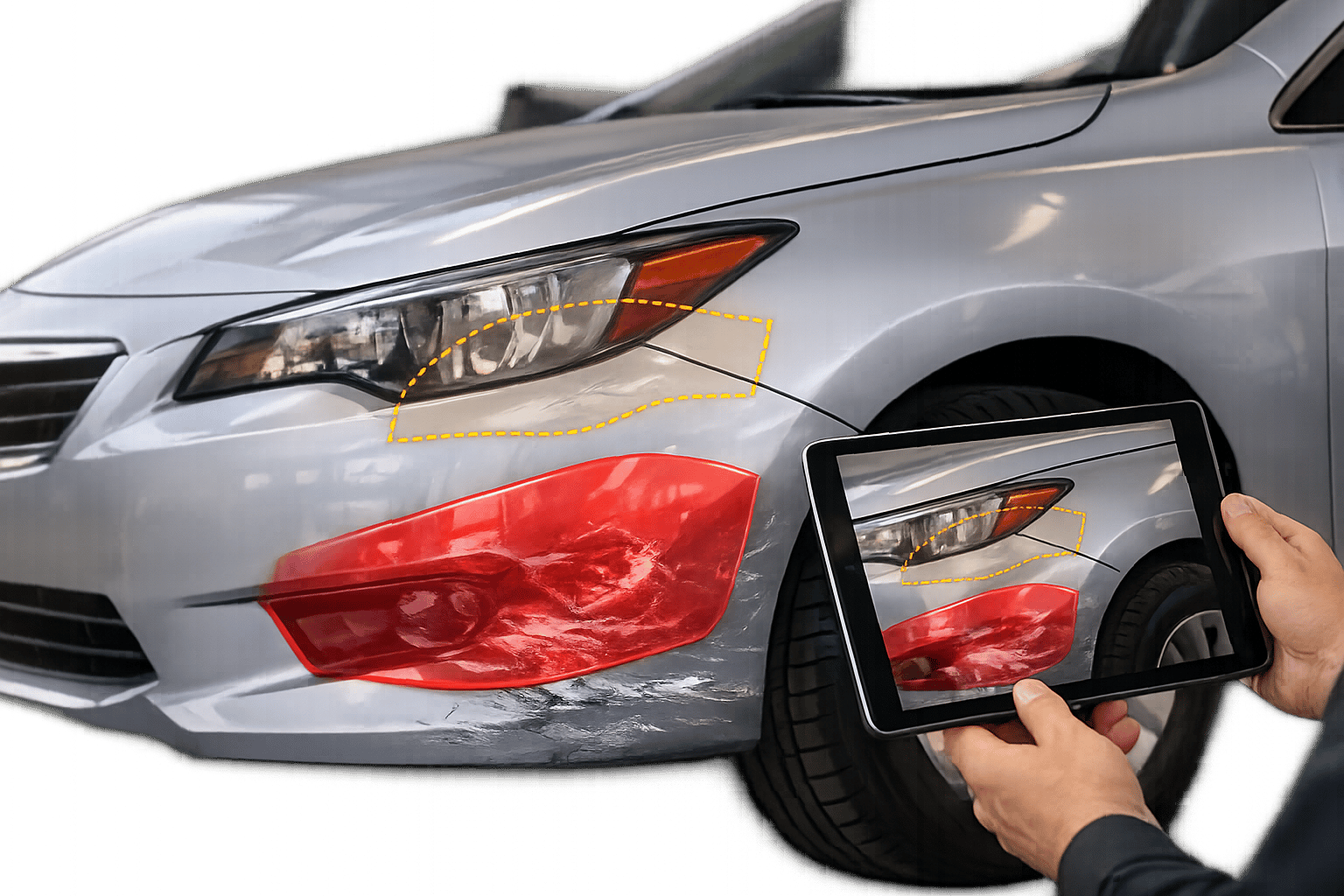

The first step is thorough documentation. Taking detailed, date-stamped photos of your vehicle establishes its condition before the accident, making it harder for adjusters to argue that new damage was pre-existing.

Capture images from multiple angles, covering all sides of the car, the VIN, and any existing dents or scratches. Keep a file with these photos, along with maintenance records, repair invoices (noting whether parts are OEM or aftermarket), and prior inspection reports. After the accident, have a trusted mechanic perform a post-repair inspection to confirm the quality of repairs and identify any lingering issues.

"Insurance companies have experts who check for hidden damage. If they find something you didn't mention, they might reject your claim. Being upfront avoids this problem." – Pittman Law Firm

Step 2: Prove the Accident Worsened Pre-Existing Damage

If your vehicle already had some damage, you’ll need to show that the accident made it worse. This requires objective evidence from professionals like mechanics or collision specialists who can differentiate between old and new damage. Police reports and witness statements can also support your case by documenting the severity of the accident.

Experts often rely on tools like paint thickness gauges and accident reconstruction data to provide unbiased proof. Additionally, vehicles with a documented accident history can lose 10% to 25% of their resale value, even if repairs are flawless. An independent appraisal based on local market data can help challenge an insurer’s valuation.

"The more evidence you can provide to support your claim regarding the new damages, the better positioned you will be in negotiations." – James Horne, Attorney, James Horne Law PA

Armed with this evidence, you’ll be better prepared to advocate for a fair settlement.

Step 3: Get Expert Help for Claims Disputes

Even with solid documentation and evidence, disputes with insurers can arise. This is where expert help becomes essential. Independent appraisals and professional analysis provide the kind of data-driven evidence insurers are required to consider.

For instance, Collision Help | Nationwide Accident Help offers a simple way to get expert guidance. You can upload photos of your vehicle damage securely and receive a personalized claim and repair plan within 24 hours. Their specialists can help you distinguish between diminished value caused by the accident and losses related to repairs, counter biased insurer formulas, and build a strong case using clear documentation.

"An independent appraisal changes the conversation. It's no longer your opinion versus theirs; it's an expert's documented, data-driven findings that an insurer is legally obligated to consider." – SnapClaim

What Determines Your Settlement Amount

Factors That Impact Auto Insurance Settlement Values

When it comes to pre-existing damage, insurers evaluate several factors to calculate your settlement. A key piece of this puzzle is your vehicle's Actual Cash Value (ACV).

The ACV serves as the cornerstone of your settlement. Insurers determine this value by assessing your car's year, make, model, mileage, condition before the accident, claim history, and maintenance records. However, automated valuation systems often miss factory-installed upgrades - like a sunroof or premium sound system - that can add real value to your car.

Beyond the ACV, the severity of the damage directly impacts your final settlement. Damage severity is a major factor. Structural or frame damage typically leads to higher settlements compared to damage to "bolt-on" parts like bumpers or mirrors. But here's the catch: many insurers use formulas like 17c, which limit the claim percentage based on damage severity and mileage, often leading to undervalued payouts. These formulas tend to ignore actual market losses.

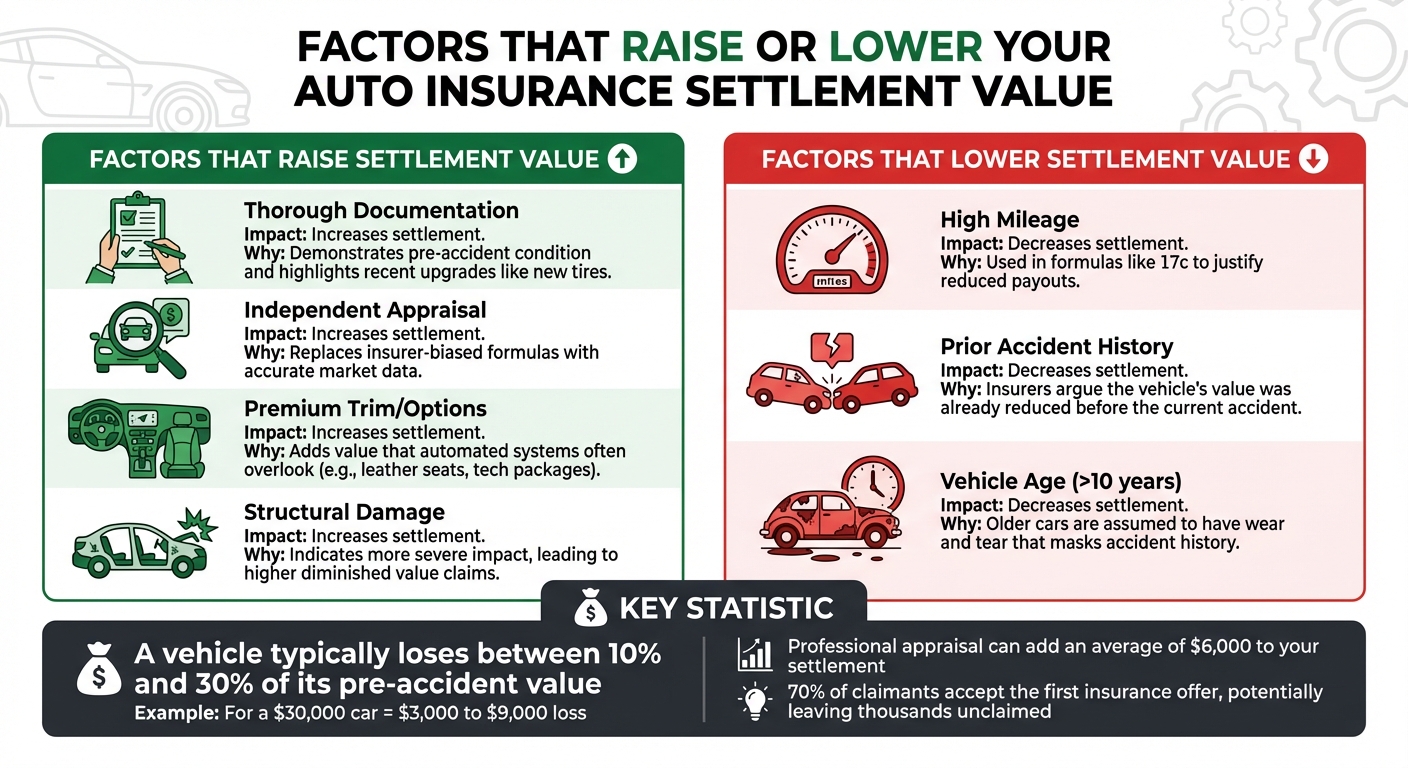

"A vehicle typically loses between 10% and 30% of its pre-accident value. For a $30,000 car, that's a $3,000 to $9,000 loss just for having an accident on its record." – SnapClaim

If you've made recent upgrades to your vehicle, those can also boost your settlement - provided you have documentation. Receipts for new tires, brakes, or a replaced transmission can increase your car's ACV. Yet, about 70% of claimants accept the first insurance offer, potentially leaving thousands of dollars unclaimed. A professional appraisal, which uses market-based data, could add an average of $6,000 to your settlement.

Factors That Raise or Lower Settlement Value

Several elements can either increase or decrease your settlement. Thorough documentation - like maintenance records, receipts for upgrades, and clear pre-accident photos - can significantly strengthen your case. Additionally, independent appraisals can replace insurer-biased formulas with actual market data, giving you more negotiating power.

On the downside, certain factors can hurt your settlement. High mileage often works against you, as insurers use it to justify lower payouts under formulas like 17c. Prior accidents on your vehicle's record can also reduce its value, as insurers argue the car was already diminished before the current incident. Similarly, older vehicles (those over 10 years old) usually receive smaller diminished value claims since standard wear and tear tends to obscure accident history.

| Factor | Impact on Settlement Value | Why It Matters |

|---|---|---|

| Thorough Documentation | Raises | Demonstrates pre-accident condition and highlights recent upgrades like new tires. |

| Independent Appraisal | Raises | Replaces insurer-biased formulas with accurate market data. |

| Premium Trim/Options | Raises | Adds value that automated systems often overlook (e.g., leather seats, tech packages). |

| Structural Damage | Raises | Indicates more severe impact, leading to higher diminished value claims. |

| High Mileage | Lowers | Used in formulas like 17c to justify reduced payouts. |

| Prior Accident History | Lowers | Insurers argue the vehicle's value was already reduced before the current accident. |

| Vehicle Age (>10 years) | Lowers | Older cars are assumed to have wear and tear that masks accident history. |

Carefully review the adjuster’s valuation report. Pay close attention to the "comparable" vehicles (comps) they use, ensuring they match your car's trim, mileage, and condition. If the insurer relies on the 17c formula, consider hiring a certified appraiser - this typically costs $350 to $600 - to provide a stronger, market-based counter to their offer.

Conclusion: Getting Fair Compensation Despite Pre-Existing Damage

Pre-existing damage doesn’t have to ruin your chances of a fair settlement. The key is acting quickly and building a solid case with documenting accident damage, clear evidence of worsening damage, and expert input.

Start by establishing a clear picture of your vehicle’s condition before the accident. Pre-accident photos, maintenance logs, and service receipts can help separate new damage from old wear and tear. This baseline is critical when proving that the accident caused additional harm.

Next, compare the vehicle’s condition before and after the accident. Highlighting how the damage has worsened can be the deciding factor in countering lowball offers or disputes from insurers.

Don’t hesitate to seek expert advice. Insufficient documentation often leads to lower payouts, but a professional appraisal can help restore your vehicle’s value and strengthen your claim. Taking these steps ensures you’re better equipped to negotiate a fair settlement.

If you’re facing challenges, Collision Help provides free expert assistance within 24 hours. Upload photos of your vehicle damage, and they’ll guide you with a personalized plan for your claim.

FAQs

What proof shows damage was from this accident, not old wear?

Insurance adjusters provide evidence to confirm that damage stems from the reported accident rather than prior wear and tear. They look for telltale signs like rust, mold, or other indicators of existing damage. Additionally, tools like the CLUE and A-PLUS databases play a crucial role. These systems track past claims and damages, helping to identify whether the damage is recent or occurred before the accident.

Can I still claim diminished value if my car had prior damage?

Yes, you can claim diminished value even if your car had prior damage. That said, the process might be a bit trickier since the existing damage could influence how the loss in market value is calculated. To strengthen your case, gather and present detailed evidence and documentation that clearly supports your claim.

When should I pay for an independent appraisal?

When you're seeking an unbiased valuation of your vehicle, paying for an independent appraisal can be a smart move. This is particularly useful if the insurance company's offer feels too low or if your car has been deemed a total loss. An independent appraisal provides a clearer picture of your car's value, helping you negotiate a fair settlement and ensuring you get the compensation you're entitled to.