What to Do When Insurers Reject Diminished Value Claims

When your car loses market value after an accident, even with perfect repairs, insurance companies often deny or undervalue diminished value claims. Here's how you can fight back:

- Understand Diminished Value: This refers to the reduced resale value of your car after an accident, even if repairs are flawless. It can take three forms: loss due to accident history, poor repairs, or immediate value drop pre-repair.

- Why Insurers Deny Claims: Common excuses include policy exclusions, lack of documentation, or claims that repairs restored your car’s value. Many insurers use flawed formulas like the "17c formula" to minimize payouts.

- Steps to Take:

- Check Your Policy: Review exclusions and coverage terms. Get the denial in writing to understand the insurer’s reasoning.

- Gather Evidence: Hire an independent appraiser, collect repair records, market data, and dealership trade-in offers.

- Negotiate: Use your evidence to counter low offers and request a supervisor review if needed.

- File a Complaint: If negotiations fail, submit a complaint to your state’s insurance regulator.

- Consider Legal Action: For unresolved claims, file in small claims court or hire an attorney for larger disputes.

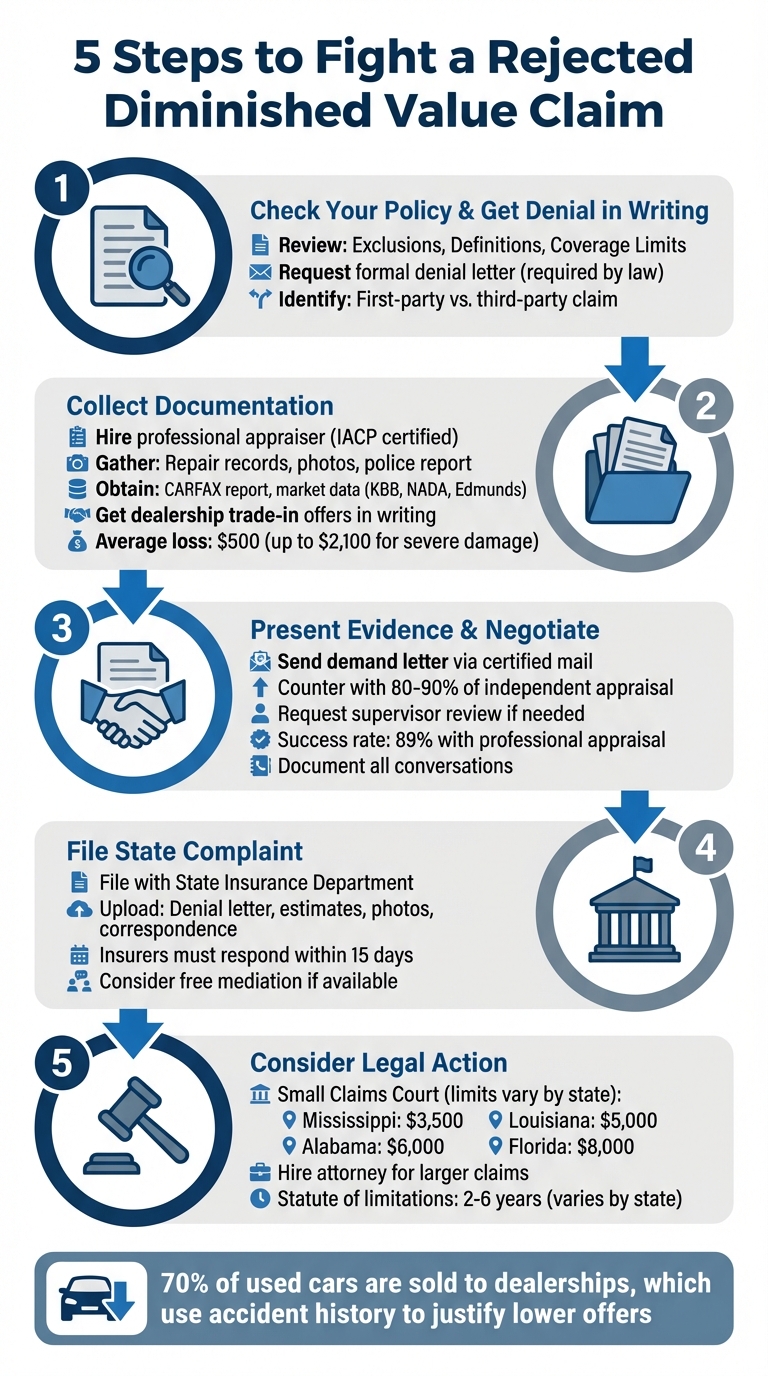

5 Steps to Fight a Rejected Diminished Value Claim

What Is Diminished Value and Why Do Insurers Deny These Claims?

Diminished Value Explained

Diminished value refers to the decrease in a car's market value after it has been in an accident and repaired. It comes in three main forms:

- Inherent diminished value: This is the depreciation that occurs simply because the vehicle now has an accident on its record, even if repairs were done perfectly.

- Repair-related diminished value: This happens when repairs are subpar, such as mismatched paint or the use of OEM vs aftermarket parts.

- Immediate diminished value: This is the loss in value that occurs right after the accident but before any repairs are made.

The financial hit can be substantial. Around 70% of used cars are sold to dealerships, and dealers often use vehicle history reports to justify lower trade-in offers. Even with excellent repairs, the accident history can make your car less appealing on the market. This inherent loss often becomes a sticking point in insurance claims.

Why Insurance Companies Reject These Claims

Understanding the nuances of diminished value sheds light on why insurers frequently deny these claims. For one, if you are at fault for the accident, most insurers won’t allow you to file a diminished value claim against your own policy. Many standard policies explicitly exclude "first-party" diminished value claims, meaning claims made by the policyholder against their own insurance. Only a handful of states, like Georgia, North Carolina, and Kansas, require insurance companies to cover these claims under a policyholder's own coverage.

Another common obstacle is documentation. Without a certified appraisal from an independent expert, insurers often rely on their own internal estimates, which tend to undervalue the claim. Factors like high mileage or prior accidents give insurers additional grounds to justify lower payouts.

Insurers also frequently use the "made whole" argument. They claim that if repairs have restored your car to its pre-accident condition, then no value has been lost. However, this overlooks the reality that buyers often view an accident history as a red flag, regardless of repair quality. This disconnect between the insurer's stance and market realities is a major reason why diminished value claims are so contentious.

sbb-itb-6a9d141

How to Stop Your Insurance From DENYING Your Claim After a Georgia Car Accident

Step 1: Check Your Policy and Get the Denial in Writing

The first step in disputing a denied diminished value claim is understanding your insurance policy and knowing what to do after an accident to protect your claim. Carefully review three critical sections: Exclusions (which might state that diminished value isn’t covered), Definitions (clarifying terms like "loss" and "damage"), and Coverage Limits and Clauses that address diminished value. If your policy defines "loss" as only covering physical repairs, insurers often use this as grounds to deny your claim.

It’s also important to know whether you’re filing a first-party claim (against your own insurance) or a third-party claim (against the at-fault driver’s insurance). Additionally, check if your state mandates coverage for first-party diminished value claims under your policy.

If your claim is denied verbally, make sure to request a formal denial letter right away. This is a crucial document. Ralph Mureti, a licensed appraiser at Diminished Value Carolina, highlights its importance:

"By law, they must provide a reason, and knowing this reason can guide your next steps".

Jeff David Stewart, Managing Partner at Stewart Bell, PLLC, agrees:

"A claim denial letter... typically outlines the reason for the denial, references the relevant sections of your policy, and may provide instructions on how to appeal".

Once you receive the denial letter, review it carefully. Look for details like whether the denial is based on a policy exclusion, lack of documentation, or some other reason. Cross-check the insurer’s explanation with the actual terms of your policy to spot any inconsistencies. If the insurer made a low offer instead of a denial, don’t hesitate to ask the adjuster questions like: "What is your offer based on?" or "Do you have a certified diminished value appraisal supporting this offer?". Keith Smith from Diminished Value Method warns:

"If they can't produce a certified appraisal from an independent, qualified appraiser, then their offer is likely arbitrary - and not based on real market evidence".

This denial letter becomes your roadmap for the next steps. With it in hand, you can start gathering the evidence and documentation needed to challenge the insurer’s decision effectively.

Step 2: Collect Documentation to Support Your Claim

To strengthen your case, you'll need solid evidence that demonstrates your vehicle's loss in value. Building on Step 1, where you identified weaknesses in the insurer's argument, this step focuses on gathering the documentation needed to back your claim.

Hire a Professional Appraiser

Insurance companies often rely on formulas, like the "17c formula", which typically limit payouts to about 10% of your vehicle's pre-accident value. A professional appraiser, however, can provide a more accurate assessment. By conducting a physical inspection and analyzing real-world market data, they determine the actual loss in value.

Look for appraisers with credentials such as IACP certification or similar qualifications. These experts evaluate repair-related diminished value, including issues like mismatched paint, poorly aligned panels, or subpar welding - all factors that can further reduce your car's worth beyond the "accident stigma". Richard Hixenbaugh, Owner of Collision Claim Associates, emphasizes the importance of an appraisal:

"An appraisal is the first step to a successful claim once you've contacted the insurer, even if you don't plan to sell the car."

While hiring an appraiser involves an upfront cost, it’s often worth it, especially for newer or high-value vehicles. Additionally, many appraisers can serve as expert witnesses if your claim leads to legal proceedings. Once you’ve obtained the appraisal, it’s time to bolster your case with additional documents.

Gather Sales Data and Repair Documentation

To support the appraisal, collect detailed records that substantiate your vehicle's loss in value. Start with repair documents, including initial estimates, final invoices, and before-and-after photos of the damage.

Next, obtain a vehicle history report from services like CARFAX. This report permanently records the accident, highlighting the "stigma" that can lower resale value. According to CARFAX, the average loss in value after an accident is $500, but for vehicles with severe damage, it can climb to as much as $2,100.

You’ll also need market data to determine your car's post-accident worth. Use resources like online listings, Kelley Blue Book (KBB), NADA, and Edmunds. Additionally, request a written trade-in value from local dealerships. Dealer statements carry weight because around 70% of used cars are sold to dealerships, which often factor accident history into lower offers.

Finally, include a copy of the police report, especially for third-party claims, to establish that you weren’t at fault. If applicable, add records of recent maintenance or upgrades that boosted your car’s value before the accident. Combine all this documentation with a formal demand letter to set the stage for negotiations in the next step.

Step 3: Present Your Evidence and Negotiate

Now that you've gathered all your evidence from Step 2, it's time to send your claim to the insurer. This starts with a demand letter that includes your appraisal, repair records, vehicle history, market data, and trade-in letters. Be sure to send this via certified mail with a return receipt to establish a verifiable paper trail. This step not only creates a legal timeline but also shows your seriousness about the claim.

Once the adjuster responds, ask specific questions to challenge any weaknesses in their offer. If their offer lacks independent appraisal evidence, push back. Request a copy of their valuation report and inquire whether they relied on wholesale auction data, such as Manheim. This type of data is inappropriate for retail diminished value claims. Many insurers use restrictive industry formulas that often limit payouts to just 10% of your car’s pre-accident value.

Remember, negotiation is a process - it’s not a one-and-done conversation. As Richard Hixenbaugh, Owner of Collision Claim Associates, explains:

"It's a negotiation... Some insurers may maintain that there is no such thing as diminished value, or offer a token amount calculated by an industry formula."

Don’t accept lowball offers. Instead, counter with 80–90% of your independent appraisal, backed by market data. If the adjuster refuses to budge, ask for a supervisor review and remind them of your legal right to recover diminished value under tort law.

Throughout this process, document everything. Record dates, times, names, and conversation details for every interaction. After phone calls, follow up with emails to confirm what was discussed. This meticulous documentation can make all the difference if you need to escalate your claim. In fact, claimants who present professional appraisals successfully recover compensation in 89% of cases after negotiation. Keep these records organized - they’ll be crucial if you need to file state complaints or take legal action.

If you hit a dead end in negotiations, don’t hesitate to seek expert help. Resources like Collision Help | Nationwide Accident Help can assist you in compiling evidence and navigating disputes.

Step 4: File a Complaint with Your State Insurance Department

When negotiations with your insurance company don’t resolve the issue, your next step is to file a complaint with your state’s insurance regulator. Every state has a Department of Insurance or an Insurance Commissioner responsible for overseeing insurers, agents, and adjusters. These entities step in when companies violate state laws or fail to honor policy terms. You can find your state’s Department of Insurance or Insurance Commissioner by searching online. Most departments provide an online complaint system where you can upload essential documents like your denial letter, repair estimates, photos, and any related correspondence.

Before filing a formal complaint, make sure you’ve exhausted all direct negotiation options. When submitting your complaint, include a detailed account of the situation, the diminished value amount you’re seeking, and all supporting documentation you’ve collected.

Some states, such as California, offer mediation programs specifically for auto damage disputes, provided certain conditions are met. For instance, in California, the total claim must exceed $7,500, and the disputed amount must be more than $2,000. The California Department of Insurance describes this process as:

"It's an informal, inexpensive and non-adversarial way to resolve your dispute with your insurance company".

However, it’s important to note that state insurance departments generally cannot force insurers to make payments or assign fault unless there’s a clear violation of policy terms or state laws. For example, the Texas Department of Insurance clarifies:

"We can help with complaints against the insurance companies, agents, and adjusters we regulate. We can't help with complaints about service providers, including body shops".

Additionally, many state regulators are limited in their ability to assist with third-party claims - those involving another driver’s insurance company.

Once your complaint is filed, insurers are typically required to respond within 15 days, although some states, like Texas, allow insurers to request a 10-day extension. The regulator will review the insurer’s response to determine if any violations occurred. While they can’t guarantee a payout, they can pinpoint errors in the claims process and help facilitate a resolution. If your state offers free mediation - often funded by the insurer - it’s worth considering. This mediation process not only provides a chance to resolve the dispute but also creates an official record that could strengthen your case if you need to take further legal action.

Step 5: Consider Legal Action

If the state regulator doesn't resolve your dispute, the next step may involve legal action. This option should only be considered after exhausting all non-legal avenues. Carefully evaluate whether the potential recovery outweighs the legal costs before proceeding.

File in Small Claims Court

Small claims court provides a simple and cost-effective way to handle diminished value claims without needing an attorney. Most states allow individuals to represent themselves in these cases, which are designed to be accessible to the public. However, it's important to check your state's dollar limit for small claims. For instance, Mississippi caps claims at $3,500, Louisiana at $5,000, Alabama at $6,000, and Florida at $8,000.

To succeed in small claims court, you'll need to prove three things: the defendant's negligence, that the accident caused damage, and that this negligence resulted in your car's diminished value. Supporting evidence is crucial - this can include photos, repair bills, police reports, and a professional appraisal. When filing, you can also request reimbursement for recoverable filing fees and appraisal costs.

Small claims court is most suitable for lower-value disputes. If your claim exceeds the small claims limit in your state, it might be time to consider legal counsel.

Hire an Attorney for Larger Claims

For claims that exceed your state’s small claims court limit, filing in civil district court or hiring an attorney becomes necessary. Legal representation is especially worthwhile for high-value claims, such as those involving expensive or nearly-new vehicles where the loss in resale value is enough to justify the legal expenses. However, for claims under $5,000 to $8,000, attorney fees could consume much of your settlement, making small claims court a more practical choice.

"For many people, the cost of an attorney won't make sense, either because they're driving older cars that aren't worth much, or the claim is so small that it will get lost in legal fees." – Chris Kissell, CarInsurance.com

Before hiring an attorney, weigh the potential recovery against the estimated legal costs. Also, be mindful of your state’s statute of limitations for filing property damage lawsuits, which typically ranges from two to six years. If you decide to proceed with legal representation, an attorney can guide you through complex disputes and ensure you’re on equal footing, especially when dealing with insurance companies that have their own legal teams.

Conclusion

Dealing with the rejection of a diminished value claim requires persistence and careful preparation. Insurance companies often rely on lowball offers or outright denials, hoping frustrated vehicle owners will give up instead of fighting for fair compensation. Don’t let that discourage you. Start by asking for written justification for the denial and gather solid evidence, such as an independent appraisal that clearly outlines your vehicle’s loss in value. These hard numbers can carry significant weight during negotiations.

If your claim continues to be denied or negotiations reach a standstill, there are steps you can take to escalate the matter. Filing a complaint with your state insurance department can bring external oversight into the process. Alternatively, if your claim falls under your state’s small claims court limit - like $8,000 in Florida, $5,000 in Louisiana, or $3,500 in Mississippi - you can pursue legal action there. For larger claims, consulting an attorney may be the best way to ensure your case is taken seriously.

Keep in mind that the responsibility to prove your vehicle’s loss in market value lies with you. This can feel overwhelming, but expert support can simplify the process. Whether it’s understanding your policy, compiling documentation, or navigating the appeals process, professional guidance can make a significant difference between accepting a low offer and receiving the settlement you’re entitled to.

Act quickly, as property damage claims are subject to statutes of limitations, which vary by state but typically range from two to six years. Use the initial rejection as a starting point for negotiations, not a final decision. Don’t settle for less than what you deserve.

For personalized support, consider reaching out to Collision Help | Nationwide Accident Help. They offer nationwide assistance, from uploading photos of your vehicle damage to creating a customized plan for your claim. With their expertise on your side, you’ll be better equipped to secure a fair settlement.

FAQs

How do I prove my car lost value after an accident?

To demonstrate your car's diminished value, obtain an independent, certified appraisal that evaluates its market value before the accident and compares it to its current value after repairs. Gather supporting documents like repair invoices, photos showing the damage and subsequent repairs, and a detailed vehicle history report. These materials serve as solid evidence of the loss in value, helping you build a stronger case when negotiating with insurers.

What can I do if my insurance company denies my diminished value claim?

If your insurance company rejects your diminished value claim, the first step is to ask for a written explanation of their decision, along with any appraisal or documentation they relied on. This gives you a clear understanding of their reasoning and allows you to prepare a response.

Next, consider hiring an independent certified appraiser to review the situation. They can provide an unbiased assessment and evidence to strengthen your case. This independent evaluation can be a powerful tool when challenging the insurer's decision.

If discussions with your insurance company still don’t lead to a resolution, you have other options. You can file a complaint with your state’s insurance department, which oversees insurance practices and may intervene on your behalf. Alternatively, you can take the matter to small claims court, where you can present your case without needing extensive legal representation. For more complicated disputes, consulting an attorney experienced in insurance claims can help ensure your rights are protected.

Do all states require insurers to pay for diminished value claims?

Most states mandate that insurance companies address diminished value claims, but there are exceptions to this rule. For instance, Nebraska does not acknowledge diminished value claims, and Michigan law does not require insurers to compensate for them. If you're uncertain about the regulations in your state, it’s wise to check local laws or seek advice from a knowledgeable expert.