Complete Guide to Navigating Auto Insurance Claims

When dealing with auto insurance claims, here's what you need to know upfront:

- Filing a Claim: You request financial help from your insurer after an accident, theft, or damage. This process involves providing evidence, notifying your insurer, and working with an adjuster.

- Key Coverage Types: Liability covers damage you cause to others. Collision and comprehensive handle your car's damage - whether from accidents or non-accident events like theft. Other options like PIP/MedPay cover medical costs, while UM/UIM protects against uninsured drivers.

- Costs and Risks: Filing a claim can raise your premiums by up to 54%. Evaluate whether filing is worth it, especially for minor damages close to your deductible.

- Steps After an Accident: Stay safe, call the police, exchange details, document everything, and notify your insurer within 24 hours.

- Handling Disputes: If the settlement feels unfair, you can negotiate, provide additional evidence, or seek legal help.

Quick Tip: Always document incidents thoroughly and use your insurer's mobile app for faster claims processing. Avoid admitting fault at the scene, and know your policy's limits to avoid surprises.

How to File an Auto Insurance Claim in 5 Steps

Auto Insurance Basics You Need To Know

Auto Insurance Coverage Types Comparison Chart

Before you file a claim, it's essential to understand your policy. Different types of coverage protect against specific risks, and knowing the details can save you time and money.

Types of Coverage

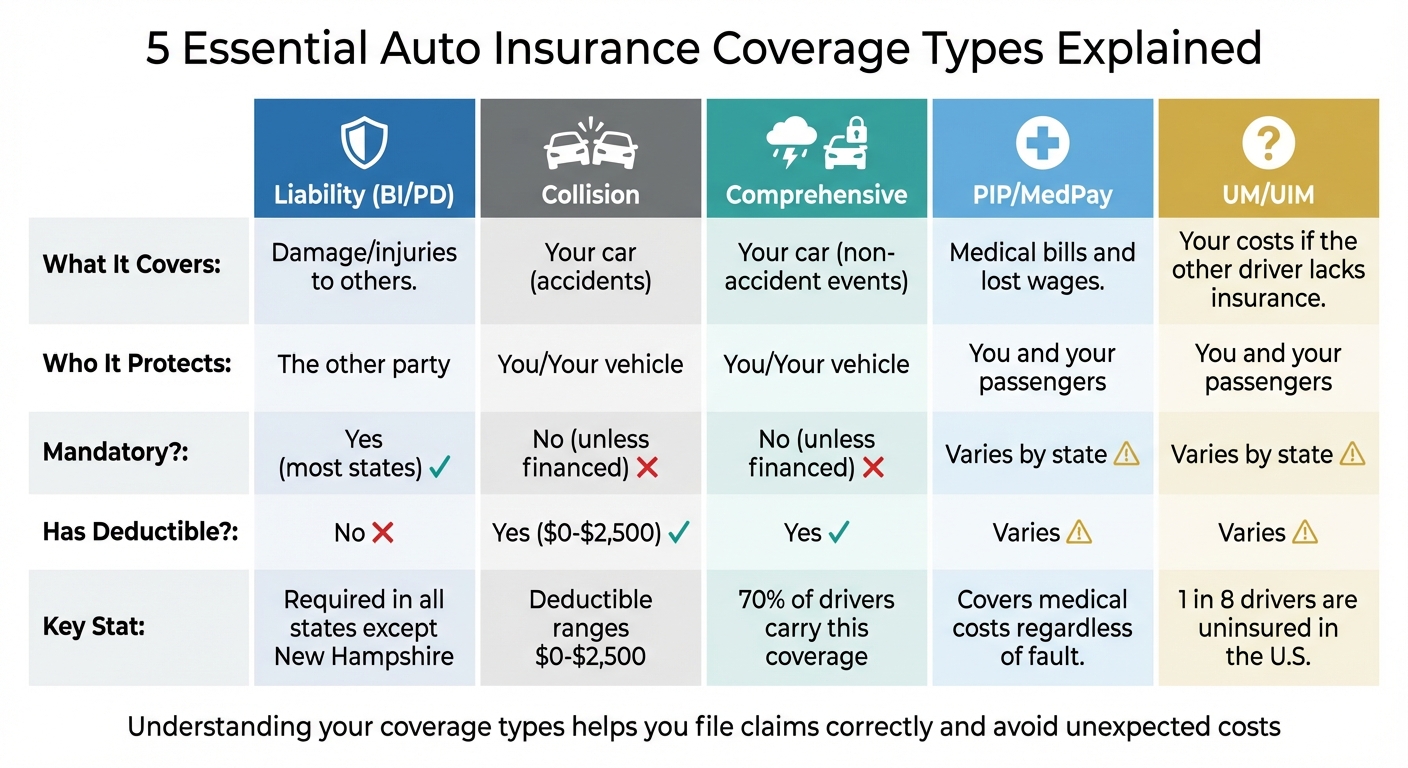

Liability insurance forms the core of most auto policies in the U.S. It's required in nearly every state except New Hampshire. This coverage pays for injuries and property damage you cause to others when you're at fault. Unlike other coverages, liability insurance typically doesn't involve a deductible - your insurer starts covering costs right away.

Collision coverage takes care of repairs to your own vehicle after an accident. Whether you hit another car, a tree, or even a pothole, this coverage has you covered. While optional, it's usually required if you're financing or leasing your car. Keep in mind, you'll need to pay a deductible - ranging from $0 to $2,500 - before your insurance kicks in.

Comprehensive coverage handles non-collision-related incidents, like theft, vandalism, fire, or weather damage. If your car is stolen or damaged by a falling tree, comprehensive coverage steps in. Like collision coverage, it requires a deductible and is often mandated by lenders. Around 70% of drivers carry this type of coverage.

Personal Injury Protection (PIP) and Medical Payments (MedPay) address medical expenses for you and your passengers, no matter who caused the accident. PIP goes further by covering lost wages and services like childcare, while MedPay focuses solely on medical and funeral costs. In no-fault states, PIP benefits are filed with your insurer, even if the other driver is at fault.

Uninsured/Underinsured Motorist (UM/UIM) coverage steps in when the at-fault driver either has no insurance or doesn't have enough to cover your damages. This coverage ensures you're not left footing the bill for medical expenses or car repairs.

Your coverage type determines who you file a claim with. If you're at fault, you'll typically use your collision coverage. If someone else is responsible, you can file a third-party claim with their liability insurance to avoid paying your deductible. If your insurer pays a claim where you weren't at fault, they might pursue subrogation to recover costs - including your deductible - from the responsible party's insurer.

| Coverage Type | What It Covers | Who It Protects | Mandatory? | Has Deductible? |

|---|---|---|---|---|

| Liability (BI/PD) | Damage/injuries to others | The other party | Yes (most states) | No |

| Collision | Your car (accidents) | You/Your vehicle | No (unless financed) | Yes |

| Comprehensive | Your car (non-accident events) | You/Your vehicle | No (unless financed) | Yes |

| PIP/MedPay | Medical bills and lost wages | You and your passengers | Varies by state | Varies |

| UM/UIM | Your costs if the other driver lacks insurance | You and your passengers | Varies by state | Varies |

Understanding these coverage types is the first step to navigating your policy effectively.

Common Insurance Terms

Deductible: This is the amount you pay out of pocket before your insurance takes over. For example, if your deductible is $500 and your repair costs $3,000, you'll pay $500, and your insurer will cover the remaining $2,500. Choosing a higher deductible can lower your premiums but increases what you pay upfront during a claim.

Policy limits: These represent the maximum amount your insurer will pay for a covered loss. If your property damage liability limit is $50,000 and you cause $75,000 in damage, you'll be responsible for the extra $25,000.

Actual Cash Value (ACV): This is your vehicle's market value at the time of the loss, not what you originally paid for it. Cars depreciate quickly, so if your three-year-old car is totaled, you'll likely receive its current market value minus your deductible. If there's a gap between what you owe on a loan and what the insurer pays, gap insurance can help.

Total loss: This happens when repair costs exceed a certain percentage of your car's ACV. In such cases, your insurer pays the vehicle's value (minus your deductible) rather than covering repairs.

When To File A Claim

Once you understand your coverage, the next step is deciding whether to file a claim. Most insurance policies require you to report accidents promptly, even if you're unsure about filing a claim. However, not every situation warrants filing.

Filing a claim can increase your premiums by an average of 54%. If your repair costs are only slightly higher than your deductible - say, a $600 repair with a $500 deductible - it might be cheaper to pay out of pocket.

You should always file a claim if there are injuries, significant damage, or another driver involved. Even minor accidents should be reported, as hidden damage or injury claims could surface later. Some states also require you to report accidents to the DMV if injuries occur or if property damage exceeds a set amount - $750 in California, for example.

Modern cars have advanced safety systems, like automatic emergency braking, which can make even minor repairs expensive. For single-car incidents with minor damage, consider paying out of pocket if the repair costs are close to your deductible. Also, check if your policy includes accident forgiveness, which might prevent a rate hike after your first at-fault claim.

| Scenario | Recommended Action | Reason |

|---|---|---|

| Injuries involved | Always file | High liability risk and medical costs |

| Single-car, minor damage | Evaluate costs | Paying out-of-pocket may save on future premiums if costs are near deductible |

| Other driver at fault | File with their insurer | Use their liability coverage to avoid your deductible |

| Theft or vandalism | Always file | Covered under comprehensive; requires a police report |

| Hit-and-run | Always file | Use uninsured motorist or collision coverage; requires police notification |

Avoid settling privately with cash at the scene. Doing so could jeopardize your ability to claim full insurance benefits if complications arise later. Even if you decide not to file a claim, always document the incident thoroughly with photos and notes.

How To File And Manage Your Claim

Filing an insurance claim can feel overwhelming, but understanding the process makes it much easier. From what you do at the accident scene to communicating with your insurer, each step matters. Here's how to handle it effectively and protect your interests.

What To Do Right After an Accident

Focus on safety first. Check for injuries - yours, your passengers', and anyone else involved. If there's serious damage or injuries, call 911 immediately. If your car is drivable but blocking traffic, move it to the side of the road and turn on your hazard lights.

Contact the police, even for minor accidents. A police report can be critical for the claims process and is often required when injuries or significant damage occur. Make sure to get the officer’s name, badge number, and the report number for your records.

Exchange details with the other driver. Collect their name, phone number, address, driver’s license number, insurance company, policy number, and vehicle information (license plate, VIN, make, and model). Taking clear photos of their license and insurance card can save time later.

Document everything. Snap photos and videos of the vehicles, damage, road signs, traffic signals, skid marks, and the overall scene. If there are witnesses, ask for their names and contact information.

Be cautious with your words. Avoid admitting fault or apologizing to anyone, including the police. Stick to the facts, as any statements you make could impact the liability investigation. Many insurers now let you start a claim directly from the accident scene using their mobile app.

| Information Type | Details to Collect |

|---|---|

| Other Driver(s) | Name, phone, address, driver’s license number, insurance company, and policy number |

| Vehicle(s) | License plate, VIN, make, model, year, and color |

| Witnesses | Names and contact phone numbers |

| Scene Details | Date, time, location, weather conditions, and photos of damage |

| Police Info | Officer’s name, badge number, and police report number |

These steps lay the groundwork for a smoother claims process, which we’ll cover next.

Reporting Your Claim To Your Insurer

After documenting the accident, report the claim to your insurer as soon as possible. File the claim within 24 hours, even if you’re unsure who’s at fault. Most insurers offer multiple ways to file, including by phone, online portals, or mobile apps.

When filing, provide key details like the accident’s date, time, location, weather conditions, the other driver’s information, your vehicle’s details (make, model, year, VIN, and license plate), and the police report number. Don’t worry if you’re missing some details - your insurer can help fill in the gaps.

During the initial report, ask about your deductible, coverage limits, and whether your policy includes rental car coverage. Many states require insurers to respond to claims within 30 days, and in New York, property damage claims must receive a settlement offer within six business days.

Keep a detailed log of all claim-related communications, noting the names of representatives you speak with and the topics discussed.

Working With a Claims Adjuster

Once your claim is filed, an adjuster will be assigned to investigate. They’ll review statements, inspect the accident scene, and examine the police report to determine liability. They’ll also assess the damage to your vehicle, either through photos, repair estimates, or in-person inspections.

The adjuster will evaluate your policy to determine which coverages apply - such as collision, comprehensive, or Personal Injury Protection (PIP) - and calculate repair costs or the actual cash value if your car is deemed a total loss. Based on their findings, they’ll provide a settlement offer.

Make sure you have all your documentation ready for the adjuster, including photos, police reports, and witness information. Attend vehicle inspections to point out all damage and ask questions. If they request additional documents, like medical bills or repair estimates, respond quickly to keep the process moving. Many insurers also allow you to upload photos through their app to speed things up.

Verify the adjuster’s identity when they arrive. If you don’t hear back within a week, follow up for updates. If you disagree with their settlement offer, ask for a written explanation of how it was calculated and which policy limits were applied.

If you weren’t at fault, your insurer might cover your repair costs and then pursue subrogation to recover those expenses - and possibly your deductible - from the at-fault driver’s insurance.

Getting Your Vehicle Repaired

Once the adjuster approves the repairs, you can move forward. Many insurers have preferred repair shops that guarantee their work and bill the insurer directly. You can also choose an independent shop, but you might need to pay upfront and wait for reimbursement.

It’s a good idea to get two estimates to compare costs. If hidden damage is found during repairs, the adjuster may need to reinspect your car. Your insurer will cover the repair costs minus your deductible. For instance, if repairs cost $4,000 and your deductible is $500, you’ll pay $500, and your insurer will handle the rest.

If repair costs exceed your car’s pre-accident value - or a state-specific percentage - the insurer may declare it a total loss. In that case, you’ll receive the car’s depreciated value minus your deductible. If you owe more on your car loan than the insurer pays, gap insurance can cover the difference.

Managing Medical Bills and Lost Wages

If you or your passengers are injured, Personal Injury Protection (PIP) or Medical Payments (MedPay) coverage can help cover medical costs, regardless of fault. PIP may also reimburse lost wages and services like childcare, while MedPay focuses on medical and funeral expenses.

In no-fault states, you’ll file PIP claims with your own insurer, even if the other driver caused the accident. Keep detailed records of medical treatments, prescriptions, and work absences. Submit medical bills as you receive them instead of waiting until treatment is complete.

If the other driver is at fault and their bodily injury liability coverage applies, you can also file a claim with their insurer for medical expenses and lost wages. Save every receipt, medical record, and pay stub - it’s essential for negotiating settlements or disputing claims.

sbb-itb-6a9d141

Complex Claims and Dispute Resolution

After mastering the basics of filing and managing claims, you should be prepared for situations where disputes arise. Not every claim goes smoothly - sometimes the at-fault driver's insurer denies responsibility, your own insurer undervalues your vehicle, or the other driver lacks insurance. Knowing how to navigate these challenges and when to stand your ground can make all the difference between receiving a fair settlement and walking away with less than you deserve.

Filing a Claim With the Other Driver's Insurer

If the other driver is at fault, you can file a third-party claim directly with their insurance company instead of relying on your own coverage. This approach can save you from paying your deductible, but it comes with its own set of challenges. The other insurer represents their policyholder, not you, and will only pay if they determine their driver was at fault and cooperates with the investigation.

Start by contacting the at-fault driver's insurer as soon as possible. Provide all the documentation you gathered at the scene, such as photos of the damage, the police report number, witness contact details, and information about the vehicles involved. Keep all communication in writing, ideally via email, to create a clear record in case disputes arise.

Be aware that many states follow comparative negligence laws. If you're partially at fault, your settlement may be reduced accordingly. For instance, if you were speeding and the other driver ran a red light, the insurer might assign you 10% of the blame, reducing your settlement by that percentage. In Utah, you cannot collect damages if you're found more than 50% responsible.

If dealing with the other driver's insurer becomes too frustrating, you can file through your own collision coverage. Your insurer will then seek reimbursement - along with your deductible - through subrogation from the at-fault driver's insurance. If the settlement offer still falls short, there are steps you can take to challenge it.

Challenging Fault Decisions or Settlement Offers

When a third-party insurer offers a low settlement, don't accept it without question. Initial offers are often "lowball" figures meant to test your knowledge of your claim's value.

"The insurance adjuster's first settlement offer is just the initial step in a (sometimes difficult) negotiation process, so be prepared to fight for the best result." - David Goguen, J.D., University of San Francisco School of Law

If the offer doesn't meet your expectations, respond with a detailed demand letter. Break down your expenses, including medical bills, lost wages, repair costs, and pain and suffering. Attach any additional evidence the adjuster may have overlooked, such as photos of traffic signals, skid marks, vehicle debris, or witness statements. If you're disputing a total loss valuation, you can request an independent appraisal to determine your vehicle's actual cash value.

For bodily injury claims, wait until all medical treatments and physical therapy are complete before settling. Signing a "release for damages" means you give up the right to seek further compensation, even if new injuries emerge later. In California, insurers must notify you of their claim decision within 40 days of receiving proof of claim. If your insurer fails to meet these obligations, you can file a formal complaint with your state's insurance department.

If negotiations stall or your case involves serious injuries, it may be time to consult a personal injury attorney to guide you through the litigation process.

Uninsured and Underinsured Motorist Claims

Roughly 1 in 8 drivers in the U.S. are uninsured. If you're hit by an uninsured driver - or involved in a hit-and-run - your Uninsured Motorist (UM) coverage can help cover medical bills and vehicle damage. For hit-and-run incidents, there usually needs to be physical contact between the vehicles, and you must report the accident to both the police and your insurer within 30 days.

Underinsured Motorist (UIM) coverage becomes essential when the at-fault driver has insurance, but their policy limits are too low to cover your damages. For example, California's minimum liability requirement is $15,000 for bodily injury to one person and $30,000 for multiple people. These amounts may barely cover basic expenses like an ambulance ride or an emergency room visit.

To file a UIM claim, you must first exhaust the at-fault driver's liability limits by accepting a policy-limits settlement. Your insurer will then pay the difference between your UIM limit and the amount recovered from the at-fault driver. For instance, if the at-fault driver's policy covers $15,000 and your UIM limit is $100,000, you could receive up to $85,000 in additional damages.

Before accepting a low policy-limit settlement, investigate the at-fault driver's personal assets. An asset search can reveal whether pursuing a lawsuit might yield more than the insurance claim. Be sure to obtain written verification of the at-fault driver's policy limits and any payments made, and share this documentation with your insurer. In California, UM claims typically have a two-year statute of limitations.

Organizing Your Claim Documentation

Good documentation is key to resolving disputes effectively. Create a dedicated file - digital or physical - for all claim-related materials. Track expenses as they occur, rather than waiting to compile them later. Submit medical bills promptly and maintain a detailed log of all communications, noting the names of representatives and the topics discussed. If an adjuster requests additional documents, respond quickly to keep the claim moving forward.

Many insurers now allow you to upload photos and documents through their mobile apps, which can speed up the review process. For more complex claims involving multiple parties or serious injuries, consider using a spreadsheet to track dates, amounts, and follow-up tasks. Staying organized strengthens your position when negotiating settlements or addressing disputes.

Tools and Services That Make Claims Easier

Streamlining the claims process can save time and reduce stress. Alongside efficient filing and document management, these tools and services aim to simplify your experience even further.

Using Mobile Apps and Online Portals

Many major insurers - like GEICO, Progressive, and AAA - offer mobile apps that allow you to handle claims quickly and efficiently. You can report incidents, upload photos of damage, check your deductible, and monitor the status of your claim in real time. These tools help cut down on delays by avoiding the need for mail or lengthy phone calls.

To be prepared, download and log in to your insurer’s app ahead of time so it’s ready when you need it. Some insurers now require app-based photo submissions, so it’s worth confirming their preferred process.

"The faster they get what they need from you, the quicker you'll get paid." - Consumer Reports

Some advanced apps even let you recreate the scene of the accident using diagrams, arrows, or videos to provide a clear picture of what happened. Through these platforms, you can also schedule appraisals, book rental cars, and arrange for glass repairs. Glass repairs typically take less than 30 minutes, while replacements may take around an hour. If you’re not receiving push notifications, it’s a good idea to check the online portal regularly for updates.

These digital tools enhance the overall claims process by offering real-time updates and seamless communication, making it easier to stay informed and on track.

Getting Professional Claim Assistance

While apps and portals simplify routine tasks, professional help can be invaluable in complex or disputed claims. If your claim is denied, undervalued, or you suspect bad faith practices, turning to specialized assistance can make a big difference.

Attorneys experienced in insurance disputes can negotiate on your behalf to secure fair settlements. Many work on a contingency fee basis, meaning you only pay if they recover compensation for you.

"Insurance companies aim to protect their profits. They don't make money by paying out every claim - they profit by doing the opposite: denying your claim." - Morgan & Morgan

If you feel your settlement offer is too low, these professionals can advocate for a better resolution or even initiate an independent appraisal if necessary. Additionally, you can contact your state’s insurance department if you encounter unreasonable delays or suspect unfair practices.

For straightforward guidance on repair disputes or total loss claims, services like Collision Help | Nationwide Accident Help offer quick evaluations. By securely uploading photos, you can receive expert advice and a personalized plan within 24 hours. These evaluations are free, providing a risk-free way to better understand your options and next steps.

Conclusion

Handling an auto claim effectively calls for preparation, detailed documentation, and persistence. Understanding the basics - like liability, collision, and comprehensive coverage - helps set realistic expectations about what your insurance will cover and what costs you’ll need to handle yourself. These key points emphasize the need for prompt action and careful record-keeping.

Act quickly after an accident and document everything thoroughly. Take photos of the damage, gather witness information, record the vehicle’s VIN, get the police report number, and keep track of all conversations with insurance adjusters.

Technology has also made the claims process faster and more manageable. Many insurers offer mobile apps that let you upload photos, track your claim’s progress, and schedule appraisals in real time. If you face challenges like disputed fault or a low settlement offer, consider seeking professional help. Services like Collision Help | Nationwide Accident Help provide free 24-hour evaluations and expert advice to guide you through the process.

FAQs

How do I know if filing an auto insurance claim is the right choice?

Deciding whether to file an auto insurance claim often comes down to two key factors: the cost of the damage and how it might affect your insurance rates. Start by estimating the repair costs or medical expenses and comparing them to your deductible. If the damage is minor - like a small dent or scratch - and costs less than your deductible, it may be smarter to pay for the repairs yourself to avoid a possible hike in your premiums.

On the other hand, if the damage is more serious, involves injuries, or affects someone else’s property, filing a claim is usually the better option. In these cases, your insurance can help cover the larger expenses and shield you from financial responsibility. Just remember, filing a claim for smaller issues could lead to higher premiums, so it’s important to weigh the long-term costs.

Here’s a quick checklist to help you decide:

- Estimate repair costs and see how they compare to your deductible.

- Check your coverage type (liability, collision, or comprehensive) to ensure it applies.

- Think about potential rate increases from filing a claim.

- Report incidents involving injuries or third-party damage, as your policy may require it.

If the repair costs are higher than your deductible or you’re accountable for someone else’s damages, filing a claim is usually the right move. For smaller, less expensive issues, handling it out of pocket might save you money over time.

What should I do right after a car accident?

First, prioritize safety. Check yourself and your passengers for any injuries. If anyone needs medical attention, call 911 right away. If your car is still drivable, carefully move it to a safe location, such as the shoulder of the road, and switch on your hazard lights to warn other drivers. Stay at the scene and contact the police to file a report. Be sure to get the officer’s name, badge number, and a copy of the report for your records.

Next, gather as much information as possible about the accident. Exchange insurance and contact details with the other driver, and jot down the make, model, and license plate number of their vehicle. Use your phone to snap pictures of the damage, the accident scene, and any nearby road signs. If there are witnesses, ask for their contact information as well. Once you have all this, notify your insurance company promptly and provide them with the collected details to begin your claim.

What should I do if I disagree with my insurance company’s settlement offer?

If the settlement offer seems too low or unclear, the first step is to review your policy carefully to understand your coverage and limits. Then, ask your insurer for a detailed explanation of their decision. Look for any overlooked damages or errors in their assessment. To strengthen your case, gather solid evidence like police reports, photos of the damage, repair estimates, medical bills, and witness statements, and use this to negotiate for a better settlement by clearly presenting your documented costs and reasoning.

If negotiations hit a dead end, consider escalating the matter by requesting to speak with a supervisor or the claims-resolution department. Many insurance companies also provide options like mediation or independent appraisals to settle disputes. Should these efforts not yield results, filing a complaint with your state’s Department of Insurance is another route - they can investigate the issue on your behalf. Throughout the process, keep detailed records of all communications and maintain a polite but assertive tone. If the situation still doesn’t resolve, consulting an attorney can help you explore legal options and ensure your rights are protected.