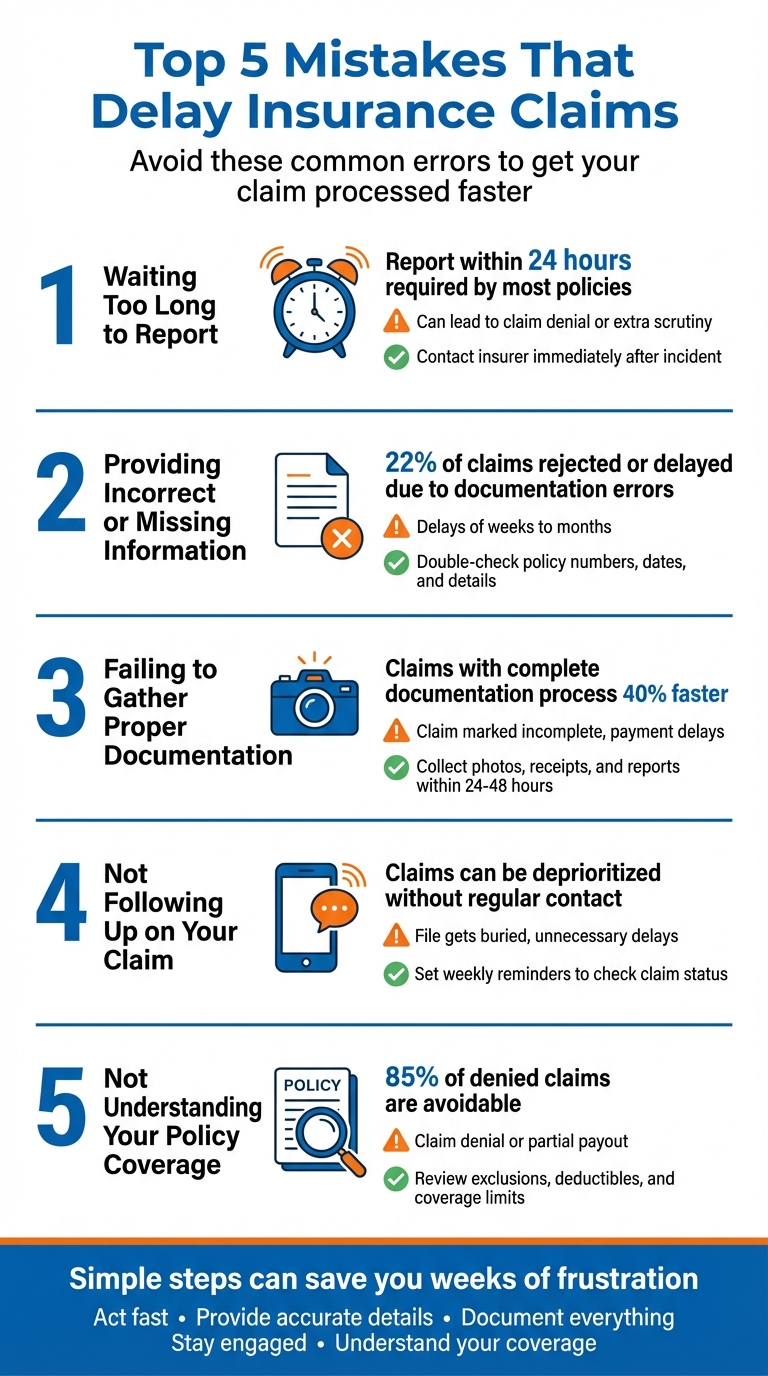

Top 5 Mistakes That Delay Insurance Claims

Filing an insurance claim can be stressful, especially when mistakes lead to delays. Here are the five most common errors that slow down the process - and how to avoid them:

- Waiting Too Long to Report: Most policies require prompt reporting, often within 24 hours. Delays can result in lost evidence, extra scrutiny, or even claim denial.

- Providing Incorrect or Missing Information: Typos, missing documents, or wrong details (like dates or policy numbers) can halt your claim. Double-check everything before submission.

- Failing to Gather Proper Documentation: Missing photos, receipts, or reports can mark your claim as incomplete. Collect evidence immediately after the incident.

- Not Following Up: Without regular updates, your claim could be deprioritized or delayed. Stay in touch with your adjuster and document all communication.

- Misunderstanding Your Policy: Filing for uncovered damages or mislabeling incidents (e.g., calling water damage a “flood”) can lead to denials. Review your policy carefully.

Key Takeaway: Avoid delays by acting fast, providing accurate details, documenting everything, staying engaged, and understanding your coverage. Simple steps can save you weeks of frustration.

5 Common Insurance Claim Mistakes That Cause Delays

Insurance Claim Nightmares: 10 Worst Mistakes PAs & Homeowners Make - Insurance Claims Basics

sbb-itb-6a9d141

1. Waiting Too Long to Report Your Claim

After an accident, the clock starts ticking. Reporting promptly isn’t just a good idea - it’s often required by your insurance policy. Most policies demand "prompt" notification, which generally means within 24 hours. Waiting longer could violate your contract and create unnecessary hurdles in the claims process.

Delays can also give insurance companies a reason to invoke the "prejudice" defense. This means they might argue that late reporting hindered their ability to investigate the scene, interview witnesses, or gather evidence to determine fault. Attorney Dan Ray highlights that postponing a claim can seriously disrupt the insurer’s investigation and evidence collection efforts.

The risks don’t stop there. Delayed reporting can lead to extra scrutiny, slower claim processing, or even outright denials. Evidence doesn’t last forever - physical damage fades, and witness recollections become less reliable over time. While reporting deadlines differ by state, ranging from 24 hours to several days, even a short delay can weaken your case.

To protect yourself, act immediately. Contact the police, document the damage, and notify your insurer within 24 hours. Quick action is essential to preserve evidence, comply with your policy, and ensure a smoother claims process.

2. Providing Wrong or Missing Information

Submitting incorrect or incomplete information is a common mistake that can bring your claim to a grinding halt.

Even something as minor as a typo can disrupt the process. Insurance companies rely on accurate details to verify claims, and when that information is missing or wrong, it often leads to delays that can stretch from weeks to months. In fact, around 22% of insurance claims are initially rejected or delayed due to documentation errors.

"One of the quickest ways to delay your claim is by submitting incomplete or incorrect details. Whether it's a typo in your policy number or an error in your reported date of loss, small mistakes can cause big problems." - Alliance Adjustment Group

Mistakes like these create roadblocks for insurers trying to process your claim. For example, an incorrect policy number might prevent the claim from even being opened. Providing the wrong date of loss could raise suspicions of fraud, while missing receipts might result in the insurer offering only a depreciated value instead of a full payout. Under the Pennsylvania Unfair Insurance Practices Act, incomplete information can legally pause the claim process.

Another potential consequence of these errors is receiving a "reservation of rights" letter. This document essentially puts your claim on hold while the insurer reassesses liability and resets their response timeline. To avoid such setbacks, take the time to:

- Double-check your policy number.

- Confirm the exact date and time of the incident.

- Attach all necessary supporting documents before submitting your claim.

"The insurance company would rather you ask questions than send a form that is incomplete or filled out incorrectly." - Law Office of Matthew L. Sharp

If you're uncertain about any part of the claim form, don't hesitate to reach out to your adjuster for guidance. A little clarification upfront can save you a lot of headaches down the line.

3. Failing to Gather Proper Documentation

Missing essential paperwork can bring your claims process to a screeching halt. Insurance companies rely on documentation to confirm the event, evaluate the damage, and calculate compensation. Without it, your claim might be marked "incomplete", leading to frustrating delays in processing payments.

"Documentation serves as the cornerstone of the insurance claims process, fulfilling multiple critical functions that protect both policyholders and insurers." - Paca Insurance

Claims submitted with thorough documentation are processed 40% faster than those missing key details. So, what should you have on hand? Start with visual evidence: take photos from multiple angles, capture the scene (including road conditions and traffic signals), and secure any dashcam or security footage. Next, gather official reports like the police accident report and financial records such as repair estimates from certified shops, towing receipts, and rental car agreements. Don’t forget your policy documents - these include your insurance card, declarations page, and any records of other drivers or witness contacts.

"Missing or incomplete documents can cause delays or even lead to a denial of the claim." - OnderLaw

Timing is everything. Aim to collect photos and witness statements within 24–48 hours while the evidence is still fresh. Many insurers now offer mobile apps that allow you to upload photos and track your claim status in real time, making the process more efficient. If you're unsure about what to include or how to organize everything, platforms like Collision Help can assist. They enable you to upload vehicle damage photos and receive expert advice within 24 hours, ensuring your claim package is complete before submission. Up next, learn how timely follow-ups can further speed up claim resolution.

4. Not Following Up on Your Claim

Filing your claim is just the first step in a longer process. Once your documentation is submitted, regular follow-ups are critical to ensure your claim doesn’t get lost in the shuffle. Without consistent communication, your file could end up buried under a mountain of other cases or delayed due to something as simple as a missing form. Insurance companies juggle thousands of claims at a time, so staying on top of yours is your responsibility.

"If you're not checking in or asking for updates, your claim could get buried under a pile of others." - Alliance Adjustment Group

Failing to follow up might even give the impression that you’ve abandoned your claim. Long gaps in communication could lead to your case being deprioritized. This is especially important when you consider the strict timelines many states impose on insurance companies. For example, in Florida, adjusters must acknowledge your claim within 14 days, make a decision within 60 days, and issue payment within 20 days. These deadlines only work in your favor if you’re actively tracking your claim’s progress.

To stay organized, set a weekly reminder to check in with your adjuster. During each call, ask specific questions like, “When will the inspection report be reviewed?” or “What’s the next step, and when should I expect it?” Follow up with an email to create a paper trail and document all communication.

"Regular follow-ups demonstrate that you are serious about getting your claim resolved." - Dick Law Firm

If your emails or calls go unanswered, don’t hesitate to escalate the matter. Politely request to speak with a supervisor who has the authority to move your claim forward. If delays continue, you can mention filing a complaint with your state’s Department of Insurance. By combining consistent follow-ups with detailed documentation, you can avoid unnecessary delays and show the insurer that you’re committed to resolving your claim without unnecessary setbacks.

5. Not Understanding Your Policy Coverage

Never assume you know all the details of your policy - take the time to read it thoroughly. Around 85% of denied insurance claims are deemed avoidable, with many stemming from misunderstandings about coverage terms. For instance, filing a claim for damage caused by a slow leak or pest infestation - issues often excluded from standard policies - can lead to outright denial or delays as the insurer reviews your policy.

"If you don't know the type of insurance you need, the mistakes you make in choosing coverage will come back to haunt you at claim time." - David Miller, Founder, Miller Public Adjusters

Using the right terminology is crucial. Mislabeling a burst pipe as a "flood" could result in a denied claim due to the flood exclusion in most policies - even though water damage from plumbing is typically covered. It's also essential to understand whether your policy reimburses based on Actual Cash Value (ACV) or Replacement Cost Value (RCV). With ACV, you'll only receive the depreciated value of damaged items, not the cost to replace them.

Before filing a claim, review the fine print. Look at exclusions, deductibles, and coverage limits. Many homeowner policies don’t cover sewer backups, earthquake damage, or maintenance-related issues unless you've purchased specific riders. Additionally, some policies require prior authorization for major repairs; skipping this step could result in partial payouts or outright denials. Make sure your premiums are up to date, as a missed payment could leave you without coverage when you need it most.

If anything is unclear, reach out to your insurance agent. Ask pointed questions about terms like "sudden and accidental" or how your deductible applies - whether it’s per incident or per year. Knowing these details ahead of time can save you from the frustration of a denied claim weeks down the road.

Get Help with Your Insurance Claim

Navigating an insurance claim after an accident can feel overwhelming, especially with the potential for errors that delay or derail the process. That’s where Collision Help | Nationwide Accident Help comes in. This service offers a simple way to get expert assistance, tackling common issues like documentation mistakes and claim handling errors - two of the biggest culprits behind claim delays and denials.

Using their secure portal, you can upload photos of the damage and receive professional guidance within 24 hours. This ensures your claim is accurate, complete, and submitted on time, helping you meet tight reporting deadlines with confidence.

"Incomplete documentation introduces uncertainty, causing delays as insurers work to clarify details." - Earl Carr, Jr., Gulf 52

But it’s not just about paperwork. The service also provides tailored advice on your policy, evaluates settlement offers, and supports you in resolving disputes. This level of expertise is especially valuable when some major insurers have been found to process claims with accuracy rates as low as 61%.

The best part? The initial evaluation is completely free. You’ll get a personalized roadmap for your claim and repair process without any upfront cost. Whether it’s a minor fender bender or a complex total loss situation, having expert guidance can help you sidestep the errors that often lead to delays or denials. To get started, visit collisionhelp.org.

Conclusion

Getting your insurance claim resolved quickly requires avoiding common pitfalls. The five mistakes - delaying your report, providing incorrect details, skipping proper documentation, neglecting follow-ups, and misunderstanding your policy - often lead to unnecessary delays. A large portion of these delays can be traced back to documentation errors.

To steer clear of these issues, focus on key actions: report the incident right away, double-check your forms for accuracy, gather all necessary evidence like photos and receipts, stay in contact with your adjuster, and thoroughly review your policy details. These straightforward steps can mean the difference between a claim that’s resolved promptly and one that drags on.

"One small mistake could delay your claim - or worse, get it denied altogether." - Elite Insurance Law PLLC

Many people lose trust in the process after experiencing just one claim-related setback. By submitting a complete and accurate claim from the beginning, you can sidestep most of the delays and uncertainties that often plague the process.

FAQs

What should I do if I can’t report a claim within 24 hours?

If you're unable to report a claim within 24 hours, make sure to file it as soon as you can to prevent delays or the risk of denial. Many insurance policies emphasize the importance of prompt reporting to keep your coverage intact. Acting quickly helps ensure your claim is processed more efficiently.

What documents speed up an auto insurance claim the most?

Providing the right documents can make your auto insurance claim process much faster. Here's what you'll need:

- Police accident report: This document provides an official account of the incident.

- Clear photos of vehicle damage: High-quality images help illustrate the extent of the damage.

- Relevant medical records: If injuries occurred, these records support your claim.

Getting these documents submitted quickly can help keep the process moving and prevent avoidable delays.

When should I escalate a delayed claim to a supervisor or my state?

If you've repeatedly followed up on a delayed insurance claim, submitted all required documents, and the insurer keeps stalling without a valid explanation, it's time to take action. Escalate the issue if they fail to respond, suddenly change their requirements, or don't provide clear timelines for resolution.

When internal escalation doesn't work, you can take it a step further by filing a formal complaint with your state insurance department. They can help mediate and ensure your concerns are addressed.

What's the difference between ACV and RCV payouts?

The main distinction between ACV (Actual Cash Value) and RCV (Replacement Cost Value) lies in how depreciation is handled. RCV pays the full cost to repair or replace your property without factoring in depreciation, meaning you get enough to restore the item to its original condition. On the other hand, ACV accounts for depreciation, offering a payout based on the item's current value. While RCV usually provides larger payouts, it often comes with higher premiums. In contrast, ACV results in smaller payouts but is generally more affordable upfront.

How can Collision Help | Nationwide Accident Help help with my claim?

Nationwide Accident Help offers expert support to make your insurance claim process smoother and less stressful. They assist in avoiding common pitfalls, such as submitting incomplete paperwork, and work to ensure your claim is processed as efficiently as possible. Their services extend across the country, guiding you through repair processes, disputes over total loss claims, and other challenges that can arise after an accident.