Insurance Adjuster Lowball Offer: What to Do Next

If an insurance adjuster gives you a lowball offer, don’t accept it right away. Low offers are often designed to save the insurer money, not to fairly compensate you. Here’s what you should do:

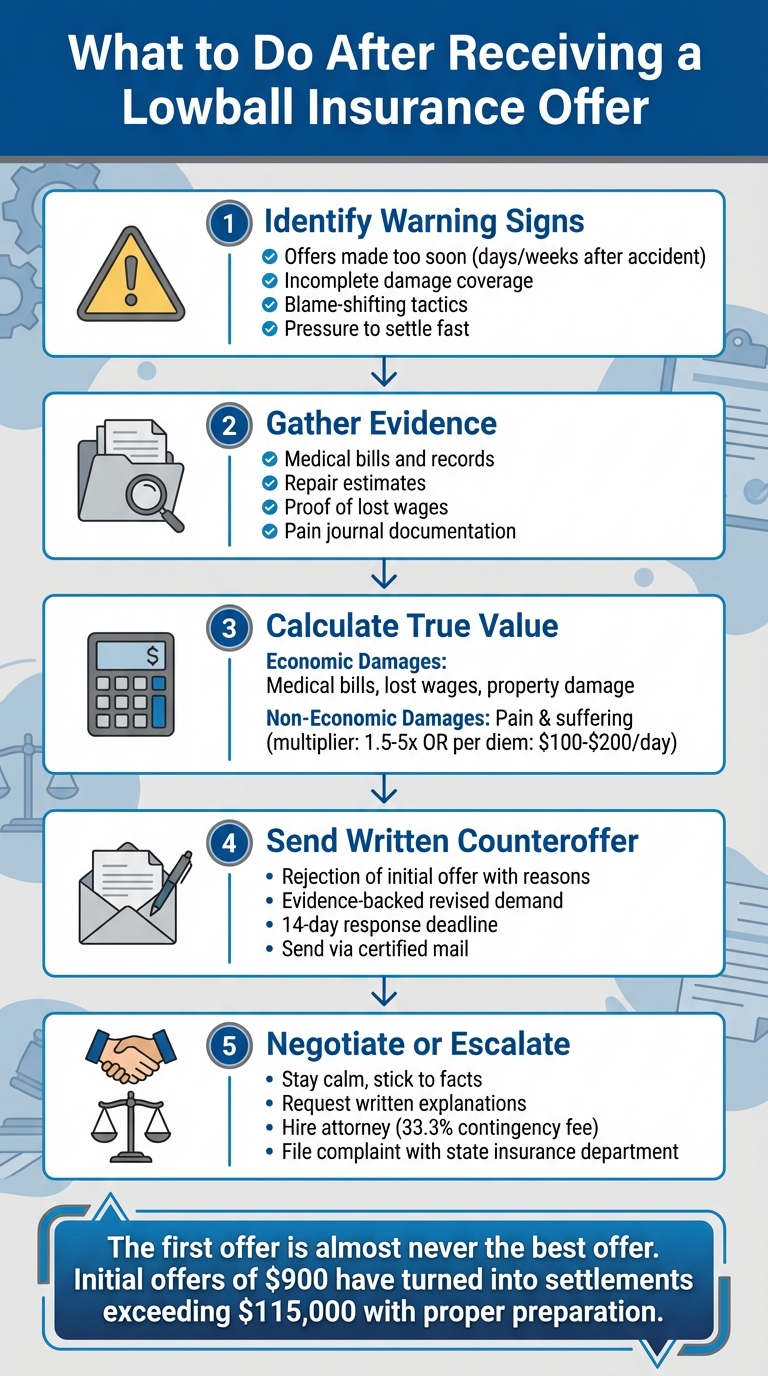

- Identify the Warning Signs: Offers made too soon, incomplete coverage, or tactics like blame-shifting and pressure to settle fast are red flags.

- Gather Evidence: Ensure your claim includes all documentation - medical bills, repair estimates, and proof of lost wages.

- Calculate Your Claim’s Value: Break down economic (medical, property damage) and non-economic (pain and suffering) losses. Use methods like multipliers or per diem for non-economic damages.

- Send a Counteroffer: Reject the low offer in writing with evidence-backed reasons and a revised demand. Include a deadline for response.

- Negotiate or Escalate: Stay calm and stick to facts during negotiations. If talks stall or bad faith practices arise, consider hiring an attorney or filing a complaint with your state’s insurance department.

Preparation and persistence can help you secure a fair settlement. If you feel overwhelmed, consult an expert or attorney for guidance.

5-Step Process to Counter Insurance Lowball Offers

How to Spot a Low Settlement Offer

Warning Signs of a Low Offer

Timing can be a major clue. If you receive an offer just days or weeks after your accident - especially before you've finished medical treatment - it’s a strong indication the offer is too low. This tactic is often aimed at closing your case before you fully understand the extent of your injuries or future medical needs.

Another red flag is incomplete damage coverage. Low settlement offers frequently address only your immediate medical bills and property damage, leaving out non-economic losses like pain, suffering, or emotional distress. If the adjuster avoids explaining how they arrived at their numbers, it’s a clear signal that something doesn’t add up.

Watch for blame-shifting tactics. Some adjusters might argue that you’re partially or entirely at fault to justify a reduced payout. This is especially concerning in states like Virginia, where pure contributory negligence laws mean even 1% fault can bar you from recovering anything. Similarly, they might downplay your injuries, labeling them as minor, exaggerated, or tied to pre-existing conditions - all to minimize their payout.

Pressure tactics are another warning sign. Statements like "This is the best offer you’ll get" or "If you don’t accept now, the offer might be withdrawn" are designed to rush you into accepting a low settlement. Keep in mind that, for example, in Nevada, you typically have up to two years from the accident date to file a claim, regardless of any artificial deadlines an adjuster might try to impose.

These warning signs highlight the strategies adjusters use to limit payouts, setting the stage for more common lowball tactics.

Common Tactics Adjusters Use to Pay Less

Insurance companies often rely on systematic strategies to reduce settlements. One widely used approach is the "3 D's" - Delay, Deny, Defend. These tactics allow insurers to stall your claim, reject coverage, or aggressively defend against your case. The scale of this strategy is significant: the U.S. insurance industry is worth over $1.4 trillion, with profits reaching $95 billion in the first half of 2024 alone.

"Insurance companies know that many people will be facing financial difficulties after suffering an injury... They will routinely delay processing a claim until you've reached the point where you're desperate enough to settle for just about anything." – Dickerson Oxton

Recorded statement traps are another common tactic. Adjusters might ask for an early recorded statement or broad medical authorization, using casual remarks or your full medical history to weaken your claim. For instance, even a polite response to "How are you today?" could be twisted to suggest you’re not seriously injured.

If an adjuster stops responding to your calls or emails after you reject their initial offer, they could be using a delay tactic to increase financial pressure. While they may claim they’re overwhelmed with cases, this is often a calculated move to wear you down. Adjusters may also monitor your social media profiles, looking for posts or photos that contradict your reported injuries. Another trick involves presenting a memo from a supervisor that falsely claims a "cap" on what the company can pay, pushing you to settle for less than your case is worth.

These tactics reveal the lengths insurers may go to in order to minimize their payouts, underscoring the importance of staying vigilant throughout the claims process.

Injury Lawyer EXPLAINS: How to Counter a Lowball Settlement Offer & Get What You Deserve

What to Do After Getting a Low Offer

If you’ve received a lowball offer from an insurance company, don’t rush into negotiations just yet. First, make sure your claim is complete and accurately calculated.

Check That Your Claim Is Complete

Before challenging a low offer, double-check that all your documentation is in order and that the adjuster has everything they need. Missing or incorrect information can often lead to claim denials.

Start by reviewing your insurance card to confirm key details like your policy number and the correct claims submission address. Your claim should include your full name, date of birth, current address, and Social Security number to avoid any identity mix-ups. If you’re covered by more than one insurance plan, clearly state which is your primary insurer and which is secondary. Also, verify your financial responsibility details - such as deductibles, co-pays, coinsurance percentages, and your out-of-pocket maximum - and confirm that your services or damages are covered under your policy. Keep a detailed record of all communications with your insurance company, including the names of representatives, reference numbers, and dates of contact.

Once you’ve confirmed your documentation is complete, it’s time to calculate the true value of your claim.

Calculate What Your Claim Is Actually Worth

To determine how much your claim is worth, break your losses into two categories: economic and non-economic damages.

- Economic damages cover tangible costs like medical bills, lost wages, and property damage. For instance, a single x-ray can cost up to $1,599, while serious vehicle repairs, such as frame or engine damage, can climb to $10,000. If you’re claiming lost wages, request a formal letter from your employer that confirms the days you missed and the exact income you lost.

- Non-economic damages account for pain, suffering, and emotional distress. Insurers often estimate these losses using a multiplier method, where they multiply your economic damages by a factor between 1.5 and 5. Alternatively, you can use the per diem method, assigning a daily value (commonly $100–$200) to your pain and suffering and multiplying it by the number of recovery days. Keeping a pain journal that tracks your daily discomfort, mood changes, and activity limitations can strengthen this part of your claim.

"The insurance company's goal is not to award you a fair settlement. Their goal is to pay you as little as possible. The easiest way for them to do this is to manipulate the math in their favor." – Hughes & Coleman

For vehicle-related claims, consider consulting experts like Collision Help. By uploading photos of your car’s damage, you can get professional guidance within 24 hours, along with a tailored roadmap for your claim and repair process.

Once you’ve established the true value of your claim, it’s time to formalize your counteroffer.

Write and Send a Counteroffer

Always submit your counteroffer in writing rather than negotiating over the phone. A written record helps prevent misunderstandings and keeps everything transparent. In your counteroffer letter, include these key elements:

- Your contact information and claim number

- A clear statement rejecting the initial offer, with specific reasons why it doesn’t cover your losses

- A bulleted list of overlooked expenses and losses, backed by evidence

- A revised demand amount, supported by documentation like medical records, pay stubs, or repair estimates

- A response deadline - typically 14 days - to keep the process moving

Ask the adjuster to provide written reasons for their low offer before you consider lowering your demand. Your counteroffer should be lower than your initial demand but still above your minimum acceptable amount. Avoid reducing your demand more than once without first receiving a higher offer from the adjuster. Finally, send your letter via certified mail with tracking to create a verifiable paper trail.

"A 'settlement authority' is just a negotiating tactic. If an adjustor tells you about their authority, he or she is trying to convince you to accept the offer on the table." – Wilhite Law Firm

sbb-itb-6a9d141

How to Negotiate and When to Escalate

How to Negotiate Effectively

Once you've submitted your counteroffer, be prepared for a back-and-forth negotiation. Stay professional and stick to the facts, even if the adjuster challenges you. A calm, fact-based approach helps reinforce your position and builds on the evidence you’ve already presented in your counteroffer.

If the insurer’s offer falls short, ask for a written explanation. Should their justification seem weak or fail to address key evidence - like medical records or repair estimates - you can use those gaps to dispute their evaluation.

Before agreeing to any concessions, double-check your policy limits and confirm that all damages, such as rental car costs or lost wages, are accounted for. Use the adjuster’s written justification to pinpoint any discrepancies in their valuation and back up your argument with the documentation you’ve already provided.

Once you’ve reached a verbal agreement, follow up immediately with a written confirmation. This letter should outline the agreed-upon amount, the damages it covers, and the expected payment timeline. A written record helps ensure clarity and prevents any last-minute misunderstandings.

When to Get Professional Help

If negotiations hit a deadlock despite your best efforts, it might be time to bring in professional help. For example, if the insurer’s offer remains far below your claim’s value, consider consulting an expert.

You should also seek assistance if you suspect bad faith practices. This could include the insurer denying your claim without valid reasoning, making threatening remarks, or misrepresenting your policy’s terms. Many personal injury attorneys work on a contingency basis, typically charging around 33.3% of the final settlement. This means they only get paid if your claim is successful.

"If you can communicate effectively in writing and in person with your insurance company, with confidence, polite aggression, and insistence on your rights, you may not need an attorney... If you are feeling frustrated, angry or anxious or are unsure about your rights, a qualified attorney (or PA) can help." – United Policy Holders

Before hiring a lawyer, consider requesting a manager review within the insurance company to explore an internal resolution. If that doesn’t work, you can file a formal complaint with your state’s Department of Insurance or invoke your policy’s appraisal clause. This clause allows independent experts to assess and determine the value of your loss.

Conclusion: Getting the Settlement You Deserve

A lowball offer is just the beginning. The first offer is almost never the best offer - it's often a test to see if you know the true value of your claim. By staying composed, gathering solid evidence, calculating the full extent of your damages, and presenting a well-supported counteroffer, you position yourself for a much better outcome.

Preparation and persistence are key. Insurance companies often rely on claimants giving in to frustration or settling quickly out of desperation. Keeping detailed records of your expenses, maintaining documentation, and waiting until you've fully recovered can demonstrate your determination to receive fair compensation. This method can lead to dramatic results - there have been cases where initial offers of $900 turned into verdicts exceeding $115,000 with the right approach. This level of preparation allows you to make decisions with confidence.

You don’t have to navigate this process alone. If you're unsure about the value of your claim or feel overwhelmed by negotiations, Collision Help can provide expert advice within 24 hours. By securely uploading photos of your vehicle damage, you'll receive a personalized plan for your claim and repair process - at no cost for the initial evaluation.

Stand your ground - you deserve fair compensation for all your damages, including medical bills, lost income, property damage, and emotional distress. With careful preparation and determined negotiation, a fair settlement is within reach.

FAQs

What should I do if an insurance adjuster offers me a low settlement after an accident?

If you get a low settlement offer, the first step is to take a close look at its details. Collect solid evidence that backs up the actual value of your claim. This could include repair estimates, medical bills, or any other relevant documents. Once you have your evidence, respond in writing with a counteroffer that reflects a fairer value for your damages - typically about 10–20% higher than the minimum amount you’re willing to accept.

Keep your tone calm and professional when communicating. Clearly explain why the initial offer doesn’t meet the mark, and point to the evidence you’ve gathered to support your case. If negotiations hit a standstill or you’re unsure how to proceed, it might be a good idea to consult an attorney. They can help guide you toward achieving a fair settlement.

How can I accurately determine the value of my insurance claim?

To determine the total value of your insurance claim, you'll need to account for all your losses. This includes medical expenses, lost wages, future costs, pain and suffering, and property damage. Gather supporting documents such as medical records, receipts, repair estimates, and police reports to substantiate your calculations. If you're unsure about the process or want expert guidance, consider consulting a personal injury attorney. They can help evaluate your claim's value and assist in negotiations with the insurance adjuster.

When should I think about hiring an attorney during settlement negotiations?

If dealing with negotiations feels like too much to handle or the insurance company isn’t offering a fair deal, it might be time to seek help from an attorney. A skilled attorney can review your claim, manage negotiations for you, and, if necessary, take legal steps to secure a fair settlement.

You should think about consulting a professional if the adjuster is dragging their feet, denying valid claims, or drastically undervaluing your losses. Legal support can not only ease your stress but also give you a stronger footing throughout the process.