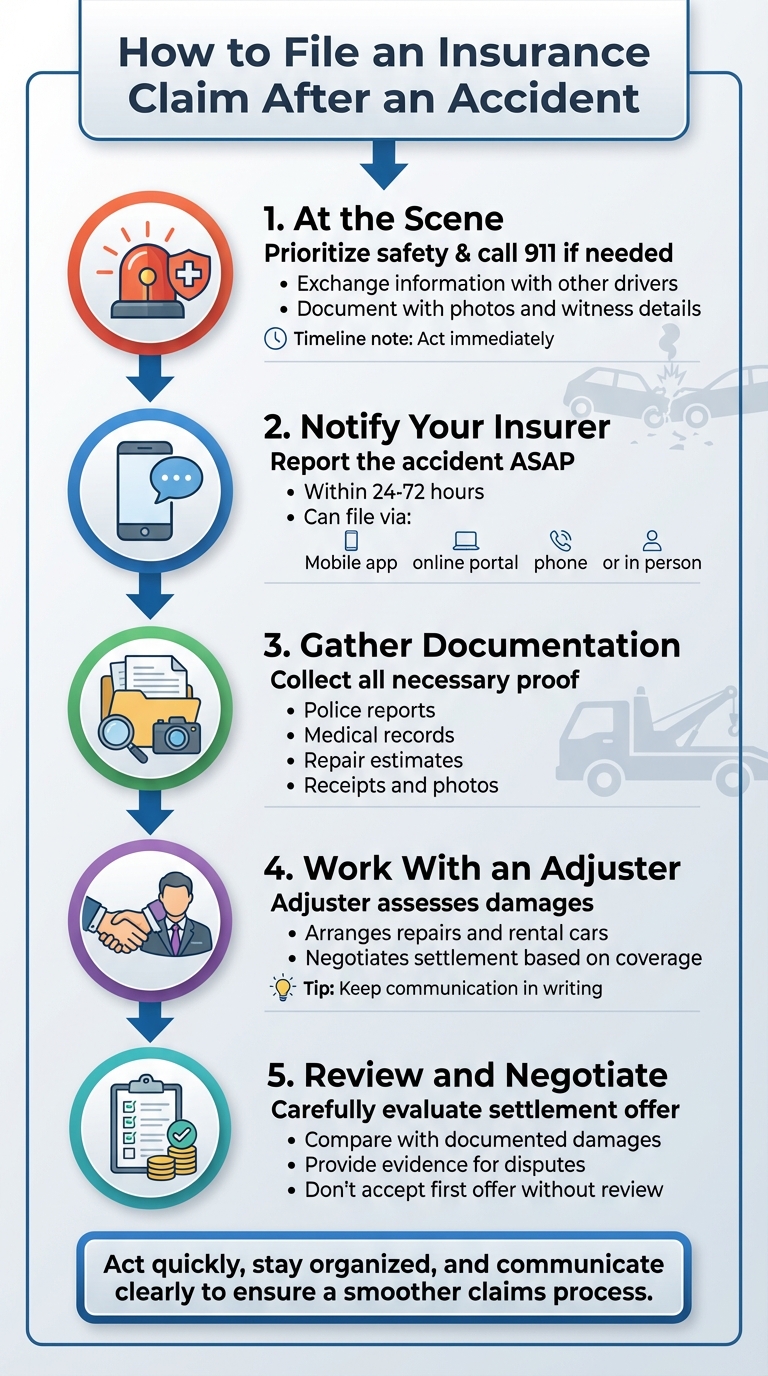

How to File an Insurance Claim After an Accident

Filing an insurance claim after an accident can feel overwhelming, but it's a straightforward process if you follow the right steps. Here's a quick breakdown:

- At the Scene: Prioritize safety, call 911 if needed, exchange information, and document the accident with photos and witness details.

- Notify Your Insurer: Report the accident to your insurance company as soon as possible - ideally within 24-72 hours.

- Gather Documentation: Include police reports, medical records, repair estimates, and any receipts or photos.

- Work With an Adjuster: They’ll assess damages and negotiate a settlement based on your coverage.

- Review and Negotiate: Carefully evaluate the settlement offer and provide evidence for any disputes.

Act quickly, stay organized, and communicate clearly to ensure a smoother claims process.

5 Steps to File an Insurance Claim After an Accident

How to File an Auto Insurance Claim in 5 Steps

What to Do at the Accident Scene

What you do immediately after an accident can shape everything that follows, from your safety to the strength of your insurance claim. These steps will help you protect yourself, handle the situation responsibly, and gather the evidence you’ll need later.

Secure the Scene and Call for Help

First, make sure everyone is safe. Check yourself, your passengers, and others involved for injuries. If it’s safe to do so, move your vehicle out of traffic and turn on your hazard lights. If someone is hurt or there’s significant damage, call 911 right away.

State laws often require you to report accidents under certain conditions. For instance, in California, any accident involving injuries must be reported to the California Highway Patrol within 24 hours. Additionally, the California Department of Motor Vehicles requires you to file an official Report of Accident form within 10 days if injuries occur or damages exceed $100. In Missouri, you must report incidents to the Driver License Bureau if an uninsured motorist is involved and property damage exceeds $500, or if someone is injured or killed. Always stay at the scene until law enforcement gives you the all-clear to leave.

Collect Information and Take Photos

Once safety is secured, exchange contact and insurance details with the other drivers. Get names, phone numbers, addresses, driver’s license numbers, insurance companies, and policy numbers. Also, note the make, model, and license plate numbers of all vehicles involved. If there are passengers, gather their contact information too. Using your phone to photograph these documents can save time and ensure accuracy.

Next, document the accident scene. Use your phone to take wide shots of the area, including all vehicles, road conditions, and traffic signs. Capture close-ups of vehicle damage, license plates, skid marks, broken glass, and debris. If anyone has visible injuries, photograph those as well - they may look different later. Be sure to include environmental details like weather, road conditions, and traffic signals.

"Photographs taken at the car accident scene are powerful evidence that will help you get maximum compensation".

Don’t forget to collect witness information. Write down their names, phone numbers, and any brief statements they are willing to provide.

When You Need a Police Report

Call the police if anyone is injured, there’s significant damage, or if the other driver leaves the scene. Even for minor accidents, involving the police can be helpful since hidden injuries or damages might surface later. If officers can’t come to the scene, you can usually file a report at your local police station or Department of Motor Vehicles.

If officers do respond, make sure you get their names, badge numbers, and the official report number. A police report provides an impartial account of the incident and can be critical for your insurance claim.

Getting Ready to File Your Claim

Once you've gathered evidence from the scene, the next step is to review your insurance policy and organize your documents. A little preparation can go a long way in avoiding delays and ensuring a smooth claims process.

Check Your Auto Insurance Policy

Start by reviewing your policy's declaration page. This page outlines the key details of your coverage, including the drivers and vehicles covered, your coverage limits, and deductibles. Familiarize yourself with the types of coverage you have. Most policies include liability coverage for bodily injury and property damage, but you may also have collision, comprehensive, uninsured/underinsured motorist, or medical payments (MedPay) coverage. Pay special attention to any exclusions or limitations, such as restrictions on aftermarket equipment, coverage in certain areas (e.g., Mexico), or deadlines for notifying your insurer about a new vehicle.

If you need a rental car, check your policy for rental coverage details. Many policies specify a daily allowance (e.g., $30 or $50 per day) and a maximum number of days covered. Additionally, confirm whether your insurer will pay for repairs or the actual cash value (ACV) of your vehicle if it's declared a total loss. Some policies may even include an appraisal clause to resolve disputes over settlement amounts.

"Unfortunately, if your car is damaged by something other than a collision and you lack comprehensive insurance coverage, you will likely need to pay for the repairs yourself. Your insurance company won't cover the damage." – Loretta Worters, Vice President of Media Relations, III

If you have any questions about your coverage, don't hesitate to contact your insurer for clarification.

Gather Required Documents and Evidence

Proper organization of your documents can help speed up the claims process. Be sure to collect the following:

- Police report

- Medical records

- Repair estimates or invoices

- Income documentation (if applicable)

- Photos, videos, and witness statements from the scene

Having these items ready will make it easier to provide your insurer with everything they need to process your claim.

When to Get Professional Help

While many claims are straightforward and can be handled without outside assistance, there are situations where professional help is valuable. For example, if you've suffered personal injuries or need to calculate non-economic damages like pain and suffering, consulting a personal injury attorney early on can protect your rights.

"As a general rule, I don't think it's necessary for policyholders to retain legal counsel when filing a claim… there are times when a policyholder needs or should retain counsel. For example, suppose an insurance company makes unreasonable requests. In that case, it can be helpful to have [a lawyer] guide the policyholder through the process." – Nathan D. Meyer, Attorney at Jaburg Wilk

If your claim involves significant losses or disputes - such as disagreements over liability or concerns that your insurer might undervalue your claim - seeking professional assistance is a smart move. Legal counsel can also manage communications with your insurer, allowing you to focus on recovery. For major commercial losses, such as a hotel owner dealing with lost revenue due to extensive damage, experts can help calculate financial losses accurately.

Once you've reviewed your policy and gathered the necessary documents, you'll be well-prepared to file your claim efficiently.

sbb-itb-6a9d141

How to File Your Insurance Claim

Once you have your policy and necessary documents ready, make sure to submit your claim right away. While the process is generally simple, acting quickly and providing accurate details are key to avoiding delays or potential denials.

Ways to Submit Your Claim

Most insurance companies give you several options for filing a claim: through a mobile app, online portal, over the phone, or even in person. For example, some insurers have dedicated phone lines specifically for claims.

Mobile apps often go beyond basic claim filing. GEICO, for instance, promotes its app as a quick and easy way to report claims online. These apps allow you to do much more, like check claim status, upload photos and documents, review your deductible, schedule appraisals, reserve rental cars, request reimbursements for towing or glass repairs, and even create a visual re-creation of the accident.

It’s best to report your claim as soon as possible - ideally within 24 hours to three days after the incident, even if you’re unsure about filing a formal claim. Missing this timeframe could lead to reduced settlements or even a complete denial of your claim. Check with your insurer to confirm their preferred method for filing.

Submit Complete and Accurate Information

When filing your claim, you’ll need to provide specific details, such as the location, date, and time of the incident, information about all parties involved, weather conditions, photos of the damage, and any police reports. Providing complete and precise information helps speed up the process and avoids unnecessary delays or disputes.

Make sure to include all relevant documents - police reports, photos, and any required forms. Stick to the facts when describing the accident, and avoid making guesses about fault or injuries. Once you’ve verified your information, review the claim options below to ensure you’re filing the right type of claim.

Types of Insurance Claims

The type of claim you file depends on factors like who was at fault, the nature of the damage, and your specific coverage. Here are the main types of claims:

- Collision claims: Cover damage to your vehicle caused by an impact, regardless of who’s at fault. Between August 2023 and August 2024, 104,857 collision claims were filed.

- Comprehensive claims: Handle non-collision-related damage, such as theft, vandalism, weather damage, or hitting an animal. During the same period, 27,804 claims were for glass or windshield damage, with over 90% occurring while driving.

- Liability claims: Filed against the at-fault driver’s insurance to recover damages.

- Uninsured/Underinsured Motorist (UM/UIM) claims: Protect you when the at-fault driver doesn’t have enough insurance or any at all.

- Personal Injury Protection (PIP): Covers your medical expenses regardless of fault in states with no-fault insurance laws.

Before filing, compare the repair costs to your deductible. If the damage costs less than your deductible, paying out of pocket might save you from a potential rate increase. Keep in mind that filing two at-fault claims within 36 months could raise your premiums by 20–40%. Additionally, many states require you to report accidents involving injuries or property damage exceeding $1,000, even if you choose not to file a claim.

Working With Your Insurance Adjuster

Once you file a claim, an insurance adjuster steps in to investigate the accident and assess the damages. Since adjusters work for the insurance company, it’s important to approach these interactions carefully. Here’s what you need to know about their role and how to communicate effectively.

What Insurance Adjusters Do

Using the evidence you’ve collected - like police reports, photos, and medical records - the adjuster evaluates fault and calculates compensation. They’ll provide an initial estimate for repairs and may request additional details if needed. If your car is declared a total loss, they’ll determine its actual cash value and subtract your deductible from the payout.

Be cautious with recorded statements. Avoid giving a recorded statement to the other driver’s insurer. If your own insurer requests one, consult legal counsel before proceeding. Keep your responses brief and factual, steer clear of admitting fault, downplaying injuries, or speculating about uncertain details. Whenever possible, communicate in writing to maintain a clear record.

Arranging Repairs and Rental Cars

You can choose your repair shop, but check with your insurer about rental reimbursement before securing a rental car. Many insurers have preferred repair networks that offer guarantees on workmanship for as long as you own or lease your vehicle.

If your policy includes rental reimbursement, it typically covers a daily amount (e.g., $30) for a limited time while your car is being repaired. Confirm your coverage details and limits with your insurer to avoid unexpected out-of-pocket costs.

Once your repair and rental arrangements are sorted, shift your focus to ensuring your settlement accurately reflects your losses.

How to Review and Negotiate Your Settlement

Don’t settle for the first offer. Insurance companies often make low initial offers to start the negotiation process.

"The first settlement offer is typically far lower than what a fair payout should be. The adjuster provides this as a starting point, anticipating negotiations".

Carefully compare the settlement offer with your documented damages. If it doesn’t match up, prepare a counteroffer. Account for both economic damages (like medical bills, lost wages, property damage, and future treatment costs) and non-economic damages (such as pain, suffering, and emotional distress). If the offer seems unreasonably low, ask the adjuster for specific reasons and respond with supporting evidence.

Your counteroffer should include detailed documentation, such as police reports, repair estimates, receipts, photos, and medical records. Stay professional during negotiations and stick to written communication to keep everything clear. Avoid finalizing the settlement until you’ve fully recovered or reached maximum medical improvement, and you’re confident about potential future expenses. If your injuries are severe or negotiations stall, it may be wise to consult an attorney to advocate for fair compensation.

Conclusion

Filing an insurance claim after an accident doesn’t have to be overwhelming if you follow a clear plan. Start at the scene by prioritizing safety, calling 911 if necessary, exchanging information with everyone involved, and documenting the incident with photos and videos from different angles. Once you’ve taken these steps, notify your insurer promptly and gather key documents like police reports, medical records, repair estimates, and receipts. Keeping everything organized and communicating in writing will make the process smoother.

When dealing with adjusters, stick to the facts and ensure your statements are documented. As attorney Adam Loewy from Loewy Law Firm advises:

"You're not required to give a recorded statement to the other driver's insurer. You can say no - and you should."

Preparation is critical to a successful claim. Carefully review any settlement offers, compare them to your documented losses, and don’t hesitate to negotiate using solid evidence.

For complex cases, such as those involving serious injuries or disputes, professional assistance can make a big difference. Collision Help | Nationwide Accident Help provides expert support within 24 hours - just upload your photos and receive a personalized plan at no upfront cost.

Whether you manage the claim on your own or enlist professional help, thorough documentation and effective communication are your best allies in securing fair compensation for your losses.

FAQs

What should I do if the other driver doesn’t have insurance?

If the other driver doesn’t have insurance, you can still file a claim through your own policy - assuming you have uninsured motorist coverage or the appropriate collision coverage. In this case, your insurance company will cover the costs and might pursue reimbursement from the at-fault driver through a process known as subrogation.

Make sure you gather solid documentation of the accident. This includes taking photos, collecting witness details, and obtaining a police report. These pieces of evidence will strengthen your claim. Reach out to your insurance provider as soon as possible to begin the claims process and clarify what your policy covers.

What should I do if my insurance company offers a low settlement after an accident?

If you’re hit with a low settlement offer, don’t accept it without digging deeper. Start by requesting a detailed breakdown from your insurance company explaining how they arrived at that number. Then, gather solid evidence to back up your case - things like repair estimates, recent vehicle appraisals, or comparable market values.

Next, draft a formal demand letter. In it, clearly explain why you believe the offer is too low, and include all your supporting documentation. Keep it professional and to the point.

Negotiation is often part of the process, so be firm but courteous in your discussions. If you still can’t reach an agreement, you might need to take further steps. This could mean consulting a lawyer or filing a complaint with your state’s insurance department. In some situations, legal action might be the only way to secure fair compensation. Staying organized and persistent throughout the process can make all the difference.

When should I consider hiring a lawyer for my insurance claim?

If your insurance claim is being challenged, involves substantial losses, or has been unjustly denied, it might be time to consider hiring a lawyer. An attorney can step in to safeguard your rights, particularly if the insurance company is acting unfairly or offering a settlement that falls short of covering your losses.

Legal help is especially valuable for more complicated claims, such as those involving severe injuries, significant property damage, or disagreements over liability. A lawyer can navigate the process for you, handle negotiations, and work to ensure you get the compensation you deserve.