How Secondary Insurance Works After PIP Coverage Runs Out

When your Personal Injury Protection (PIP) insurance reaches its limit, your health insurance becomes the next layer of coverage to manage accident-related medical costs. Here's how the process works:

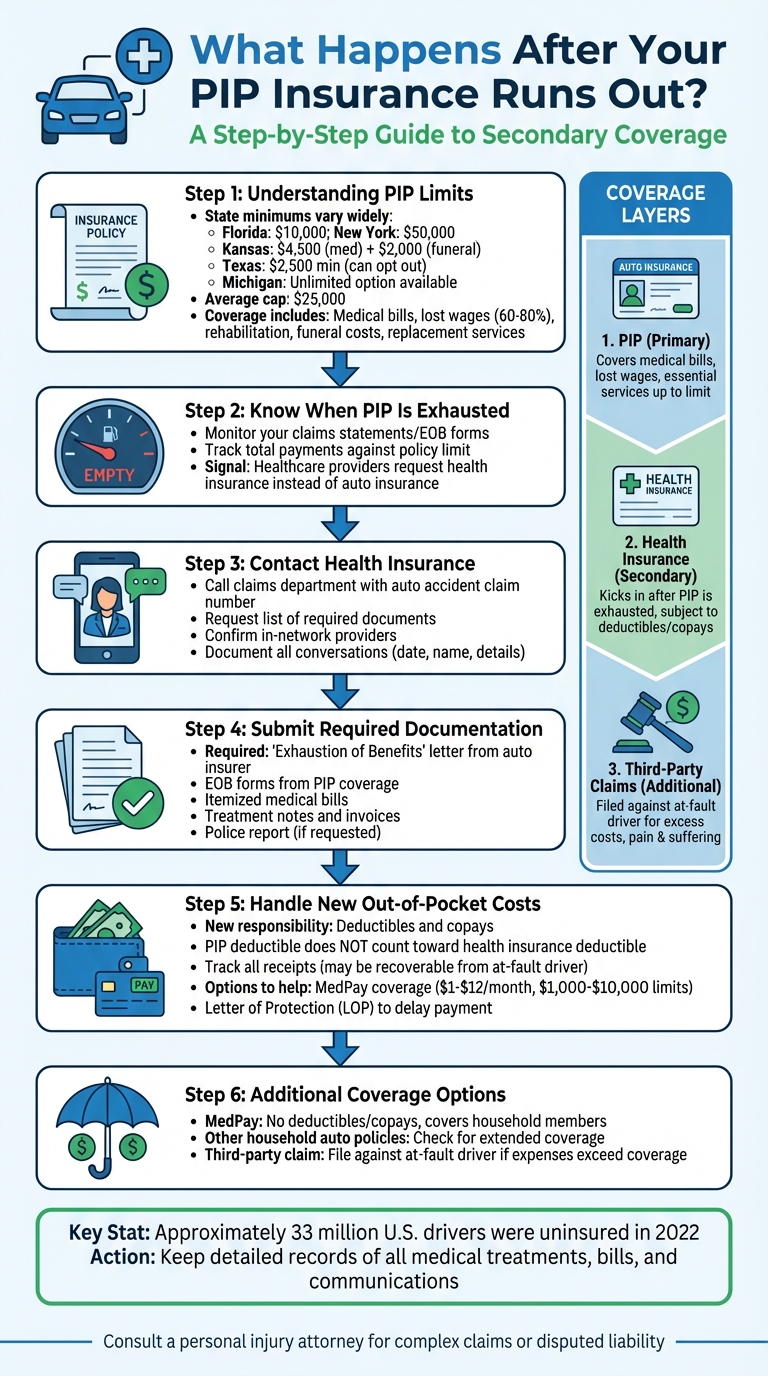

- PIP Basics: PIP pays for medical expenses, lost wages, and other costs after a car accident, regardless of fault. Coverage limits vary by state, typically ranging from $2,500 to $50,000. For example, Florida mandates $10,000, while New York requires $50,000.

- Transition to Health Insurance: Once PIP is maxed out, health insurance takes over. You'll need to provide proof of exhausted PIP benefits, such as an "Exhaustion of Benefits" letter, to your health insurer.

- Out-of-Pocket Costs: Health insurance introduces deductibles and copays, unlike PIP, which often has minimal upfront costs. MedPay, an optional auto insurance add-on, can help cover these gaps.

- Filing Third-Party Claims: In cases where PIP and health insurance don't fully cover expenses, you may file a claim against the at-fault driver’s insurance for additional compensation.

Staying organized with documentation, like medical bills and insurance statements, ensures a smoother transition between coverage types. If needed, explore supplemental options like MedPay or consult a personal injury attorney for guidance.

How to Transition from PIP to Secondary Insurance After Coverage Runs Out

How PIP Works and When Benefits Run Out

PIP Coverage Limits by State and Policy

The limits of Personal Injury Protection (PIP) coverage depend on both your state and the options you chose when setting up your policy. Fifteen states and Puerto Rico require PIP insurance, but the minimum coverage amounts differ significantly. For example, New York mandates at least $50,000 in coverage, while Florida only requires $10,000. In Kansas, the minimum is $4,500 for medical expenses and $2,000 for funeral costs. Texas handles it differently; insurers must offer at least $2,500 in PIP, but you can opt out of it in writing.

While state minimums set a baseline, many policies go beyond these requirements, with insurers often capping coverage at around $25,000. To find out your specific limits for medical expenses, lost wages, and other benefits, check the Declarations Page of your policy. Michigan stands apart by offering unlimited PIP medical benefits, though policyholders now have the option to select lower limits to save on premiums.

PIP coverage extends beyond just medical bills. It typically includes lost wages, rehabilitation costs, funeral expenses, and even replacement services like childcare or housekeeping if you're unable to manage them during recovery. In Florida, PIP usually covers 80% of medical expenses and 60% of lost wages. Meanwhile, New York's PIP pays 80% of lost earnings, capped at $2,000 per month. However, PIP does not cover property damage, injuries to passengers in other vehicles, or compensation for pain and suffering.

How to Tell When Your PIP Benefits Are Exhausted

Knowing your policy limits is key to understanding when your PIP benefits are close to running out. These benefits are considered exhausted once the total payments for all covered expenses - like medical bills, lost wages, and replacement services - reach your policy's maximum limit. For instance, if your policy has a $10,000 limit, benefits end once that amount has been paid out.

To stay on top of your remaining benefits, regularly review your claims statements or Explanation of Benefits (EOB) forms, which your insurer provides after each medical visit. You can also contact your insurance adjuster or access your insurer's website or app to request a summary showing how much has been paid and what remains. Keeping a personal log of medical bills, receipts, and wage documentation can also help you track your usage.

When your PIP funds are depleted, healthcare providers will start asking for your health insurance details instead of your auto insurance information. This shift indicates that your primary PIP coverage is exhausted, and they will bill your health insurance for any remaining costs. Being aware of this transition ensures a smooth handoff to your secondary coverage without interruptions.

How Secondary Insurance Works After PIP Coverage Runs Out

When your Personal Injury Protection (PIP) benefits are maxed out, it’s time to turn to your secondary insurance. Making this transition smooth requires a bit of preparation and communication. Here’s how to navigate the process.

Contact Your Health Insurance Provider

Start by reaching out to your health insurance provider’s claims department. Share the claim number from your auto accident to help them track your case effectively. Most health insurers will need formal proof that your PIP benefits are fully used up before they’ll process any accident-related claims. Ask them what specific documents they require and confirm that your healthcare providers are in-network, as health plans tend to have stricter rules about which providers you can use.

Keep a record of every interaction - note the date, the name of the representative, and the details of your conversation. This documentation can be incredibly helpful if any issues arise.

File Claims with Required Documentation

To move forward, you’ll need to provide an "Exhaustion of Benefits" letter or a similar statement from your auto insurance company confirming your PIP limits have been reached. Without this, your health insurer is likely to deny any accident-related claims.

"Some health insurance providers will not pay claims related to a car accident until you provide proof that: PIP benefits have been used in full [and] you have no other primary coverage." – AccidentDoctor.org

In addition to the exhaustion letter, submit Explanation of Benefits (EOB) forms from your auto insurance provider for each medical bill. These forms detail what your PIP coverage paid and what remains unpaid. You’ll also need itemized medical bills, treatment notes, and invoices from your healthcare providers. If requested, include a copy of the police report. Let your doctor’s billing department know that your PIP benefits are exhausted so they can start billing your health insurance directly.

Handling Deductibles and Copays

Once your health insurance takes over, you’ll be responsible for covering deductibles and copayments as outlined in your policy. Unlike PIP - which in some states, like Florida, might cover up to 80% of your medical costs - your health insurance will follow its own cost-sharing rules. Keep in mind that any deductible you paid under PIP won’t count toward your health insurance deductible, so you’ll need to meet a new one.

Track all out-of-pocket expenses, including receipts for deductibles and copays. These costs might be recoverable if you file a liability claim against the at-fault driver. If covering these expenses becomes challenging, check whether your auto policy includes Medical Payments (MedPay) coverage, which can help with health insurance copays and deductibles. Another option is asking your medical provider if they accept a Letter of Protection (LOP), which allows you to delay payment until you receive a legal settlement.

Other Coverage Options After PIP Runs Out

When Personal Injury Protection (PIP) benefits are used up, it's time to look into other coverage options to help manage any remaining medical costs.

Using MedPay for Additional Medical Expenses

Medical Payments Coverage (MedPay) is an optional add-on to your auto insurance that can be a big help when PIP benefits are exhausted. Unlike other coverage, MedPay kicks in right away - there are no deductibles or copays - and it typically costs between $1 and $12 per month, depending on the limit you select. This makes it a practical way to handle medical expenses that your primary insurance might not fully cover.

MedPay limits usually range from $1,000 to $10,000, with $5,000 being the most common choice for policyholders. Another advantage? MedPay is portable, meaning it can cover you and family members who live with you, even in situations outside of your own vehicle.

Keep in mind that how MedPay works can vary between insurers. Some treat it as the primary coverage, while others use it to handle out-of-pocket costs after your health insurance has paid its share. It's a good idea to check with your insurer to understand how they prioritize payments.

Adding MedPay to your coverage can provide an extra layer of financial protection once your PIP benefits are gone.

Checking for Coverage from Other Auto Policies

In addition to MedPay, it’s worth reviewing other auto insurance policies in your household for potential secondary benefits. Many policies extend coverage to family members living in the same home, even if they aren’t driving the insured vehicle. For example, if you’re injured as a passenger in someone else’s car, your own auto policy is typically considered primary. Once those benefits are exhausted, the vehicle owner’s policy may step in as secondary coverage.

To figure out if you’re eligible, take a close look at the "Definitions" section in your household’s auto insurance policies. Terms like "insured" and "resident relative" can clarify who is covered. If you have a high-deductible health plan, you might also be able to stack MedPay benefits from multiple household policies to help cover out-of-pocket costs without tapping into your savings.

It’s a smart move to contact each insurer to confirm how coverage is prioritized and what their filing procedures are. Proper coordination can help you avoid claim denials and make sure you’re making the most of your available resources.

sbb-itb-6a9d141

Understanding Subrogation and Medical Liens

Once your primary Personal Injury Protection (PIP) benefits are used up, navigating subrogation and medical liens becomes a critical part of managing your recovery. These processes can directly impact the final amount you receive from a settlement with the at-fault driver. Understanding how they work can help you protect more of your compensation.

What Subrogation Means for Your Settlement

Subrogation gives your health insurer the right to recover costs they covered for your accident-related medical expenses from the at-fault party's insurance. As attorney Dan Ray explains: "If your health insurer pays for accident-related medical expenses, it will reclaim part of those costs from your settlement."

Here’s an example: If you receive a $1.5 million settlement and your health insurer paid $400,000 in medical bills after your PIP coverage ran out, they may claim that $400,000 from your payout. Unlike subrogation, reimbursement means your insurer waits for you to collect your settlement before requesting repayment, rather than pursuing the at-fault party directly.

Before agreeing to any subrogation claim, ask your insurer for an itemized breakdown of the charges they want to recover. Also, review your policy’s Summary Plan Description (SPD). If the SPD doesn’t clearly outline subrogation or reimbursement rights, your insurer may not have legal grounds to claim a portion of your settlement. Understanding this can help you explore alternative payment options, like Letters of Protection.

How Letters of Protection (LOPs) Work

If your secondary insurance doesn’t cover all your medical costs, a Letter of Protection (LOP) can ensure you continue receiving care while deferring payment until your settlement is finalized. An LOP is essentially a lien - a written agreement where a healthcare provider agrees to treat you now in exchange for payment from your future settlement. However, if your settlement doesn’t fully cover the lien, you’ll be responsible for any remaining balance.

How to Negotiate Medical Liens

Negotiating medical liens is another key step in maximizing your settlement. Medical liens are often negotiable, so don’t accept the first amount you’re presented with. Start by requesting an itemized statement of charges and carefully review it for errors or unrelated treatments. You can also use the "Common Fund Doctrine" to argue that since your attorney’s efforts secured the settlement, the lien should be reduced proportionally to account for attorney fees and case expenses. For example, if attorney fees make up 33% of your settlement, the lienholder may agree to reduce their claim by the same percentage.

In some states, like Illinois, laws cap provider liens at around 40% of your total compensation. This means any amount above that cap could be reduced. Reach out to lien claimants early in the settlement process and emphasize that accepting a guaranteed, reduced payment now is more advantageous than waiting for months for a potentially smaller payout. Always get any agreement to reduce a lien in writing before finalizing your settlement.

Here’s a quick guide to the negotiability of different lien types:

| Provider/Bill Type | Negotiability | Key Notes |

|---|---|---|

| Ambulance Services | Very Difficult | Rarely agree to negotiate |

| Medical Doctors/Physician Groups | Difficult | Often requires persistence |

| Hospitals/County Facilities | Moderate | May be subject to legal caps |

| Health/Med Pay Insurers | Negotiable | Often open to reductions for common fund defenses |

| Medicare/Medicaid | Statutory | Governed by strict formulas but may reduce for attorney fees |

Effectively negotiating liens can help ensure you retain a larger portion of your settlement, making it essential to approach claims management with a clear strategy and attention to detail.

Filing Claims Against the At-Fault Driver's Insurance

Once you've used up your Personal Injury Protection (PIP) benefits, you might still face expenses like pain and suffering that aren't covered. In such cases, filing a third-party claim against the at-fault driver's liability insurance can help you seek compensation for these additional damages. This process, however, involves meeting specific legal requirements and gathering strong evidence to build a compelling case.

When You Can File a Third-Party Claim

In no-fault states, you can only file a third-party claim after meeting certain financial or injury thresholds set by state law. These thresholds vary by state. For instance, Massachusetts requires expenses exceeding $2,000, New York sets the limit at over $50,000, and Utah requires you to first exhaust $3,000 in PIP coverage.

It's also important to understand how comparative negligence laws might affect your claim. If you're partially at fault for the accident, your settlement could be reduced. In many states, being 50% or more at fault bars you from recovering any damages. Additionally, insurers often require signing a "release for damages" before settling, which prevents you from seeking further compensation later. Be aware of your state's statute of limitations for personal injury claims - these typically range from one to six years. Missing this deadline could mean losing your right to file a claim entirely.

Gathering Evidence to Support Your Claim

To strengthen your claim, you need solid documentation. Start by collecting the at-fault driver's name, insurance details, and contact information at the scene. Also, gather witness names and phone numbers. Request a copy of the police report, as it serves as an official record to establish liability. As attorney Ben Michael advises:

"Document everything. Take pictures and videos of every single bit of damage to your car or property from every angle. There is no such thing as too much documentation."

Keep all medical records, bills, and receipts related to your injuries. If you've lost income due to the accident, collect pay stubs or letters from your employer to prove it. For property damage, get multiple repair estimates and document any specialty equipment or damaged child safety seats. To support claims for pain and suffering, maintain a daily journal detailing your pain levels, treatments, and how the accident has impacted your life. Paul Koenigsberg, Managing Partner at Koenigsberg & Associates, emphasizes:

"A detailed record of symptoms can be crucial if you need to file a personal injury claim or seek compensation for medical costs."

Getting Help with Complex Insurance Claims

Having thorough documentation makes it easier to handle disputes over liability. However, third-party claims can get complicated, especially when dealing with uninsured drivers or contested liability. In 2022, approximately 33 million licensed drivers in the U.S. were uninsured. If the at-fault driver's insurer denies responsibility despite clear evidence, consulting a personal injury lawyer can help you navigate the complexities of state laws.

For property damage claims, such as vehicle repairs or disputes over a total loss, you can turn to resources like Collision Help | Nationwide Accident Help. By uploading photos of your vehicle damage, you can receive personalized guidance within 24 hours. Their experts help you understand your repair options and work through insurance disputes through a secure, easy-to-use process.

Conclusion

Shifting from PIP (Personal Injury Protection) to secondary insurance can be a smooth process with the right preparation. Start by informing your medical providers to bill PIP first. Once your PIP coverage is used up, have them bill your health insurer. At the same time, reach out to your health insurer to activate secondary coverage, keeping in mind that deductibles and copays will come into play. If needed, consider supplemental options like MedPay for additional support.

Handling property damage is another key part of the process. For property damage claims - such as vehicle repairs or disputes over a total loss - resources like Collision Help | Nationwide Accident Help can be invaluable. By uploading photos of your vehicle damage, you can receive tailored advice within 24 hours. This service offers a secure and simple way to explore repair options and resolve insurance disputes.

When faced with denied claims, complex coverage questions, or issues like statutes of limitations, seeking professional help is essential. Attorney Don Corson emphasizes the importance of expert assistance in uncovering hidden coverage, negotiating medical liens, and ensuring critical deadlines aren't overlooked.

FAQs

What should I do when my PIP coverage runs out?

When you've exhausted your Personal Injury Protection (PIP) benefits, you can rely on your health insurance or secondary auto insurance to cover additional costs. The first step? Reach out to your health or auto insurance provider to clarify what comes next. Usually, this means submitting necessary paperwork - like medical bills and claim forms - to ensure your expenses are handled.

It's important to stick closely to your insurer's instructions to avoid any hiccups or delays in processing your claim. If the process feels overwhelming or you're unsure about your options, seeking assistance from a professional service can make things much easier.

What is MedPay, and how can it help after PIP benefits are used up?

MedPay, or Medical Payments coverage, steps in to cover medical expenses once your Personal Injury Protection (PIP) benefits are used up. It’s designed to handle costs like doctor visits, hospital stays, and other medical treatments, no matter who caused the accident.

What sets MedPay apart from health insurance is that it usually serves as the primary coverage for accident-related medical bills. This means it kicks in first, offering financial relief before your health insurance takes over. It’s a practical way to help manage out-of-pocket expenses after an accident.

What documents do I need to file a health insurance claim after my PIP benefits are used up?

When your Personal Injury Protection (PIP) coverage runs out, turning to your health insurance for a claim involves a bit of preparation. Start by collecting essential documents like medical bills, treatment records, and any evidence that ties your injury or condition to the accident.

Your health insurance provider might also require you to fill out a claim form and submit proof of the accident, such as a police or accident report if it's relevant. Keeping everything well-organized and readily available can make the process smoother and help you steer clear of unnecessary delays.