Actual Cash Value vs Replacement Cost: Key Differences

When filing an auto insurance claim, the payout method - Actual Cash Value (ACV) or Replacement Cost Value (RCV) - determines how much money you’ll receive. Here’s the difference:

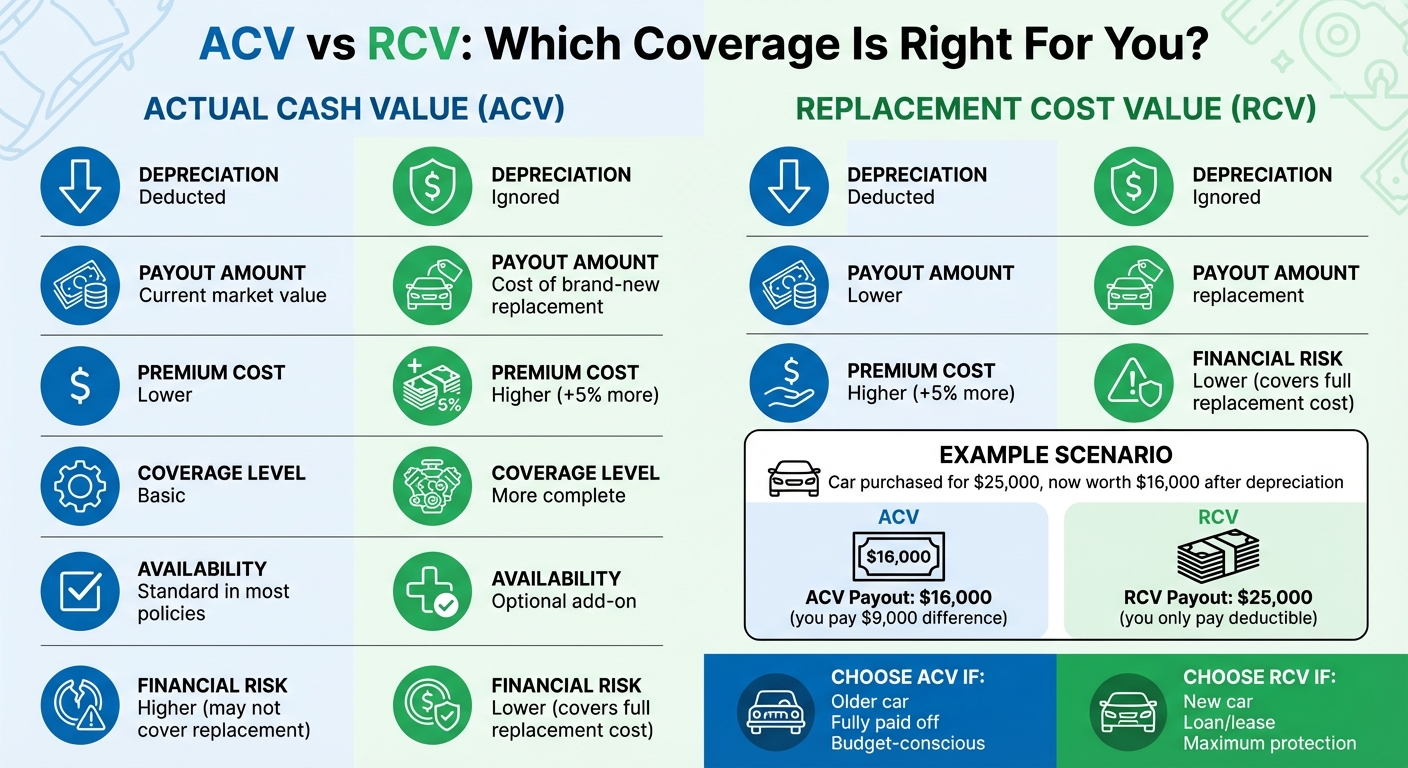

- ACV: Pays the depreciated value of your car (its current market value). It’s the default option in most policies and comes with lower premiums. However, the payout may not cover the cost of replacing the car, especially if insurance calculates a total loss, leaving you to make up the difference.

- RCV: Covers the cost of a brand-new replacement without factoring in depreciation. This optional add-on costs about 5% more in premiums and is usually available only for newer cars or original owners. It ensures you can replace your car without significant out-of-pocket expenses.

Quick Comparison

| Feature | ACV | RCV |

|---|---|---|

| Depreciation | Deducted | Ignored |

| Payout Amount | Current market value | Cost of a brand-new replacement |

| Premium Cost | Lower | Higher |

| Coverage Level | Basic | More complete |

| Availability | Standard in most policies | Optional add-on |

| Payout Process | Single payment | Often two payments |

| Financial Risk | Higher (may not cover replacement) | Lower (covers full replacement cost) |

If you own a newer car or have an auto loan, RCV might be worth considering to avoid financial shortfalls. In these cases, GAP insurance can also provide critical protection. For older cars or vehicles fully paid off, ACV is often sufficient. Always review your policy to ensure it suits your needs.

ACV vs RCV Insurance Coverage Comparison Chart

ACV vs. Replacement Cost and How insurance calculates the value of your car, house, atv, motorcycle

sbb-itb-6a9d141

What is Actual Cash Value (ACV)?

Actual Cash Value (ACV) represents the market value of your car in its current condition before a loss occurs. It’s the figure most auto insurance policies use to determine how much you’ll receive if your car is declared a total loss. Essentially, ACV helps establish the payout amount when repairs aren’t financially practical. Typically, a car is considered "totaled" when repair costs exceed 70% to 80% of its ACV, though this percentage can vary depending on your state and insurance provider.

"The actual cash value of your car is what it's worth in its current condition or the amount you could reasonably expect to get for it if you sold it today."

– Kelley Blue Book

The good news? ACV isn’t set in stone. If you think your insurer’s valuation is too low, you can dispute the total loss valuation. You’ll need to provide evidence, like recent sales data for similar cars in your area, or you can hire a private appraiser (which typically costs around $200 to $300) to back up your claim.

How Insurers Calculate ACV

Insurance companies use a simple formula to calculate ACV:

Actual Cash Value = Replacement Cost – Depreciation.

In this equation, "replacement cost" means the current price of a comparable used car. Depreciation, on the other hand, factors in several elements:

- Age and Mileage: Older cars with more miles lose value faster.

- Physical Condition: Adjusters assess vehicles as Excellent, Good, Fair, or Poor based on wear and tear.

- Market Conditions: Demand and location-specific factors influence value.

- Vehicle History: Accident records and maintenance history also play a role.

To determine ACV, insurers often use proprietary tools or third-party valuation services like CCC ONE or Mitchell. These tools analyze local market data and recent sales of similar cars to arrive at a value.

"Most carriers are connected to a third-party vendor that they're feeding the data into... Then the software aggregates the information to calculate the vehicle's actual cash value."

– Josh Damico, Vice President of Insurance Operations, Jerry

To ensure accuracy, request the full valuation report from your adjuster. Double-check that details like trim, optional features (e.g., heated seats, sunroof), and mileage are correctly noted. If you’ve recently made significant upgrades - like installing new tires or replacing the engine - submit receipts for these repairs, as they could bump up your payout.

Benefits and Drawbacks of ACV Coverage

One major advantage of ACV-based policies is that they typically come with lower premiums, as depreciation reduces the insurer’s potential payout. However, there’s a downside: the payout you receive may not be enough to replace your car. This gap can be even more problematic if you’re still paying off a loan, as the ACV might not cover the remaining balance. For this reason, many drivers opt for additional protection, which we’ll dive into when discussing Replacement Cost Value coverage next.

What is Replacement Cost Value (RCV)?

Replacement Cost Value (RCV) refers to the cost of replacing or repairing your vehicle at current market rates - without factoring in depreciation. Unlike Actual Cash Value (ACV), which deducts for age, mileage, and wear, RCV focuses on what it would cost today to restore or replace your vehicle. The idea? To put you back in the same financial position you were in before the loss.

In auto insurance, RCV typically isn't included by default. Instead, it's offered as an optional add-on, often called "New Car Replacement" coverage. Big-name insurers like Allstate, ERIE, Farmers, Liberty Mutual, Travelers, and USAA offer this option. However, there are eligibility requirements: you usually need to be the original owner, and your car must meet specific age and mileage criteria.

"Replacement cost value is the amount it would cost to replace or repair your home and belongings at current prices, without subtracting for age, condition, or depreciation."

– Terence Loose, Insurance Writer, Rocket Mortgage

The trade-off for this more comprehensive coverage is a higher premium. Adding a new car replacement endorsement can increase your insurance costs by about 5% compared to a standard ACV policy. Considering that new cars often lose up to 20% of their value in the first year alone, that 5% bump can be a worthwhile expense if you're driving a newer vehicle. Next, let’s break down how RCV works when you file a claim.

How RCV Works in Practice

When you file a claim under RCV coverage, your insurer bases the payout on current market prices for a comparable new car or the cost of repairs. If your vehicle is totaled, you’ll receive enough to buy a brand-new version of the same make and model, rather than a used car with similar mileage.

Insurers handle RCV payouts differently. Some pay the full replacement cost right after your claim is approved. Others use a two-step process: they issue an initial payment based on your car’s ACV, then reimburse the remaining amount (the "recoverable depreciation") once you provide proof that you replaced the vehicle. This ensures the funds are used as intended.

To qualify for RCV endorsements, you’ll usually need both comprehensive and collision coverage. Additionally, most insurers require you to be the original owner of the vehicle. Restrictions may apply; for instance, Travelers’ Premier New Car Replacement is only available during the first five years of ownership. Before purchasing this coverage, check your policy’s "similar kind and quality" clause to ensure the replacement vehicle will match your original’s specifications. In the next section, we’ll explore the pros and cons of RCV coverage.

Benefits and Drawbacks of RCV Coverage

One of the biggest perks of RCV is that it reduces your out-of-pocket costs in the event of a total loss. Instead of scrambling to cover the difference between your insurance payout and the cost of a new car, you’ll likely only need to pay your deductible. This can be especially helpful if you own a new car or live in an area prone to severe weather, where the risk of total loss is higher.

On the flip side, RCV coverage costs about 5% more in premiums than ACV. With auto insurance rates expected to rise by 8% industry-wide by 2025, that extra cost is something to think about. Additionally, some insurers require detailed documentation before they’ll reimburse the full amount, so staying organized during the claims process is crucial.

For those financing a newer car, RCV can be a smart investment. It helps protect you from being upside-down on your loan after a total loss, ensuring you can replace your vehicle without draining your savings or taking on more debt.

ACV vs RCV: Side-by-Side Comparison

When it comes to Actual Cash Value (ACV) and Replacement Cost Value (RCV), the main distinction lies in how depreciation is handled. ACV takes depreciation into account, which lowers the payout, while RCV covers the full cost of replacing the item without factoring in depreciation.

ACV policies are generally more budget-friendly since they limit payouts by accounting for depreciation. On the other hand, RCV policies, though more expensive, ensure you’re reimbursed enough to replace the item entirely. Most insurance plans default to ACV, with RCV offered as an optional upgrade.

The claims process also varies. With ACV, payouts are typically made in a single payment based on the item's depreciated value. RCV claims, however, often involve two steps: an initial ACV payout followed by an additional payment for recoverable depreciation once you provide proof of replacement.

Comparison Table: ACV vs RCV

| Feature | Actual Cash Value (ACV) | Replacement Cost Value (RCV) |

|---|---|---|

| Depreciation | Deducted based on factors like age and wear | Not deducted; depreciation is ignored |

| Payout Amount | Reflects the current market value of the used item | Covers the cost of a brand-new replacement |

| Premium Cost | Lower and more affordable | Higher due to greater coverage |

| Coverage Level | Basic, may leave financial shortfalls | Comprehensive, ensures full recovery |

| Auto Availability | Standard/default in most policies | Optional add-on, not always included |

| Payout Process | Typically a single payment | Often involves two payments (ACV first, then recoverable depreciation) |

| Out-of-Pocket Risk | Higher, as payouts may fall short of replacement costs | Lower, as full replacement is covered (minus deductible) |

Up next, we’ll dive into real-world examples to see how these differences impact claim payouts.

How ACV and RCV Affect Your Claim Payout

The type of coverage you have - ACV (Actual Cash Value) or RCV (Replacement Cost Value) - plays a big role in determining how much you'll receive after filing a claim. Let’s break it down with two scenarios.

Example: Total Loss Claim

Imagine you bought a car for $25,000 five years ago. After an accident, your insurer declares the car a total loss. Over time, the car's market value has dropped to $16,000 due to depreciation caused by age, mileage, and wear.

With an ACV policy, your insurer would pay you $16,000 (minus your deductible). If you want to replace the car with a new one that costs $25,000, you'd need to cover the $9,000 difference out of pocket, plus your deductible. That’s a hefty financial gap to fill.

On the other hand, if you have an RCV policy - often referred to as "New Car Replacement" coverage - your insurer would pay the full cost of a new, equivalent car, which is $25,000. You’d only be responsible for your deductible, saving you that $9,000 difference. This type of coverage can be especially helpful for newer vehicles, as new cars can lose up to 20% of their value within the first year, according to Experian.

"The actual cash value (ACV) of your car is how much money you could get for it if you sold it. The replacement cost value (RCV) is how much it would cost to buy a comparable new car of the same make and model." - Karen Axelton, Experian

But what about claims that don’t involve a total loss? Let’s look at how these coverages affect repair costs.

Example: Major Repair Claim

Now, imagine your car suffers $10,000 in damage after a collision. Here’s how the two policies would handle the situation:

- With an RCV policy, your insurer would cover the full $10,000 repair bill (minus your deductible), using brand-new OEM vs aftermarket parts at current market prices.

- With an ACV policy, depreciation comes into play. Your insurer would calculate the depreciated value of the damaged parts and only pay that amount. If your car is older, this could leave you covering the difference if you prefer brand-new parts instead of used or aftermarket replacements.

The National Association of Insurance Commissioners points out that ACV coverage often falls short of fully replacing or repairing your property. This could lead to unexpected out-of-pocket expenses, particularly if you’re keen on keeping your car in its original condition and value.

These examples highlight how the choice between ACV and RCV can make a big difference in your financial responsibility after an accident.

How to Choose Between ACV and RCV Coverage

Factors to Consider

Deciding between Actual Cash Value (ACV) and Replacement Cost Value (RCV) coverage depends on your car's age, financial situation, and how much risk you're comfortable taking.

Vehicle age and ownership status play a key role. If you're the original owner of a car that's less than five years old, RCV can be a smart choice to protect against the steep depreciation that newer vehicles experience. On the other hand, if your car is older and fully paid off, opting for RCV might not make sense since the vehicle has already lost much of its value.

Loan or lease status is another important factor. If you financed your car with a small down payment (less than 20%) or have a long-term loan, there's a chance you owe more than your car's current value. In this situation, ACV alone might not cover what you still owe. To avoid this gap, consider RCV or add GAP insurance - it costs about $7.50 per month or $90 annually - to cover the difference between your loan balance and the car's value.

Keep in mind that RCV typically increases your premiums by about 5%. If your budget is tight and you’re confident you can handle the difference between ACV and the replacement cost, sticking with ACV might be the better option.

"The difference comes down to whether your policy pays for brand-new or deducts for age and wear-and-tear." - Diane Delaney, Executive Director, Private Risk Management Association

When to Choose ACV or RCV

After weighing these factors, match your situation to the following guidelines to decide which coverage works best for you.

Choose ACV if your car is older, fully paid off, or if you're prepared to handle the gap between ACV and replacement cost out of pocket. ACV is the standard option in most auto insurance policies and is a practical choice when your car has already gone through most of its depreciation.

Go with RCV if you're the original owner of a new or nearly new car, you're still making loan or lease payments, or you want the assurance that you won't face significant out-of-pocket costs after a total loss. Keep in mind that insurers often have specific requirements for RCV, such as age and mileage limits for your vehicle.

If your loan balance is higher than your car's value, adding GAP insurance can be a cost-effective alternative. It covers the difference between the ACV payout and what you owe the lender, without the higher premiums associated with RCV.

As your car ages and your loan balance decreases, it’s a good idea to review your policy every year. Once your car’s value exceeds what you owe - or it no longer qualifies for RCV due to age or mileage limits - switching to ACV can help lower your premiums. This approach ensures your coverage stays aligned with your car's value and your financial situation.

Conclusion

Deciding between Actual Cash Value (ACV) and Replacement Cost Value (RCV) can have a big impact on your insurance payout. ACV reimburses you for your vehicle's depreciated market value, which often falls short of replacement costs. On the other hand, RCV covers the full cost of replacing your vehicle with a comparable new one, though it typically comes with premiums about 5% higher.

Your choice should align with your financial situation and the type of vehicle you own. For newer cars or those still under financing, RCV or GAP insurance can shield you from financial shortfalls. Meanwhile, for older vehicles that are fully paid off, ACV's lower premiums might be a more practical option. The key is ensuring your policy reflects your vehicle's current value and your financial priorities.

Review your policy declarations carefully. Many drivers are unaware they have ACV coverage until they file a claim and discover the payout doesn't fully cover the cost of replacing their car or paying off their remaining loan.

Take the time to understand your coverage now. Speak with your insurance agent to confirm your policy is appropriate for your vehicle's value, and reassess it annually as your car ages. This proactive step can help you avoid unexpected expenses and maintain financial stability when it matters most.

FAQs

How does depreciation impact the payout in an Actual Cash Value (ACV) policy?

When it comes to an ACV (Actual Cash Value) policy, depreciation plays a big role in determining your payout. Simply put, the ACV is calculated by taking the replacement cost of your vehicle and subtracting depreciation. Depreciation reflects factors like wear and tear, age, and the drop in market value over time.

Here’s an example: Let’s say your car’s replacement cost is $20,000, but depreciation is estimated at $5,000. In this case, your ACV payout would be $15,000. If you’re planning to replace or repair your car after an accident, you might need to cover the gap between the payout and the actual costs out of pocket.

What are the advantages of choosing Replacement Cost (RCV) over Actual Cash Value (ACV) for a new car?

Choosing Replacement Cost (RCV) for your new car means your insurance will pay for a brand-new vehicle of the same make and model if yours is totaled, instead of just covering its depreciated value. In other words, it ensures you’re not left paying out-of-pocket to replace your car after a total loss.

If you’re financing or leasing, RCV can be a game-changer. It helps cover the remaining balance on your loan or lease, sparing you from unexpected financial headaches. On top of that, RCV allows you to maintain your current level of mobility without having to settle for a less valuable replacement, easing the financial strain that often follows an accident.

To sum it up, RCV offers three major advantages: it fully reimburses you for a new car, protects you from loan or lease shortfalls, and reduces financial stress if your car is totaled.

When should I consider switching from replacement cost (RCV) to actual cash value (ACV) coverage?

Switching from replacement cost (RCV) to actual cash value (ACV) coverage can be a smart move if you're aiming to cut down on insurance premiums, especially when dealing with older vehicles or properties with lower value. Since ACV accounts for depreciation, the payout you receive might still be enough to handle repairs or match the resale value.

This type of coverage tends to work well for items or vehicles where the higher cost of RCV coverage isn't justified. Unlike RCV, which covers the expense of replacing an item with a new one, ACV reflects what it's currently worth in the market.