Understanding Filing Deadlines in Insurance Policies

Filing deadlines in insurance policies are critical and missing them can jeopardize your claim. These deadlines fall into three main categories:

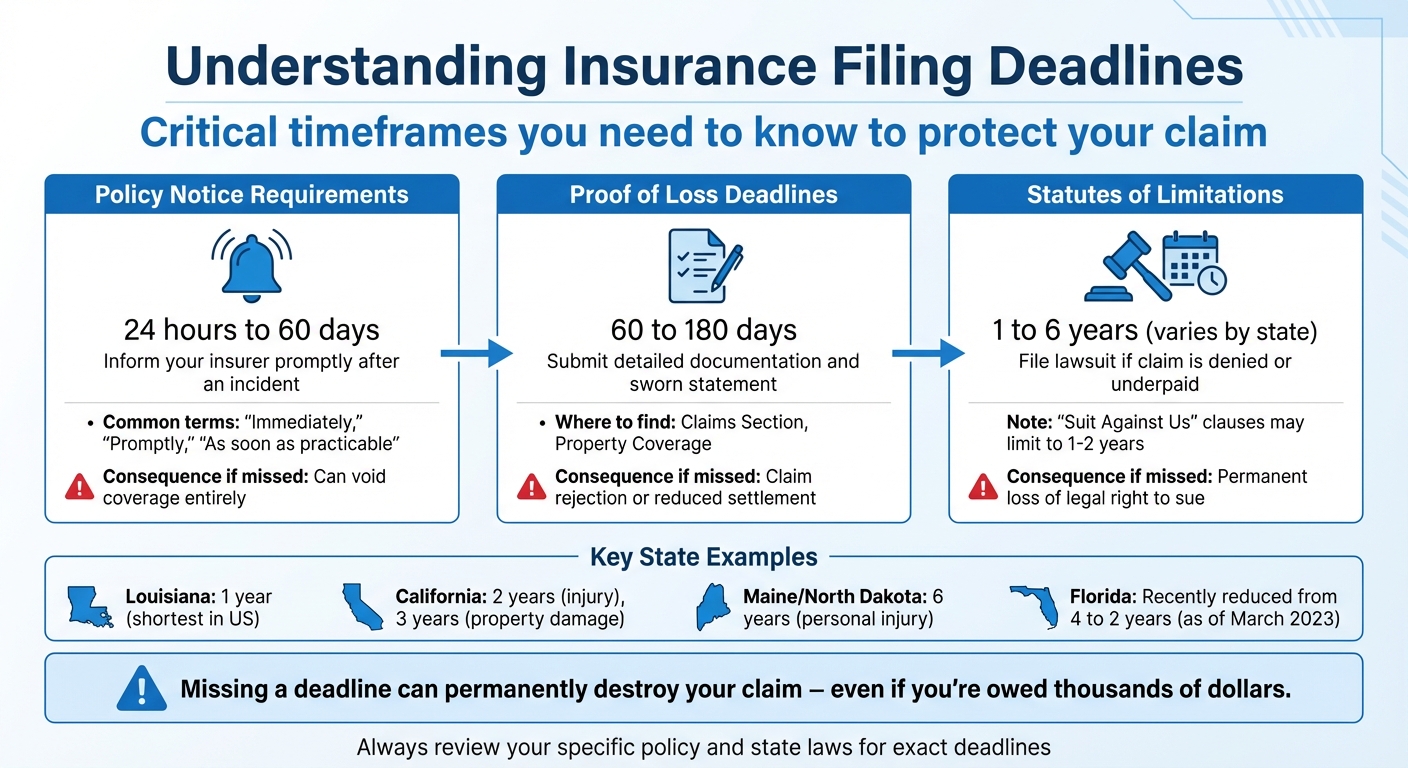

- Policy Notice Requirements: Inform your insurer promptly, typically within 24 hours to a few days.

- Proof of Loss Deadlines: Submit detailed documentation within 60-180 days.

- Statutes of Limitations: File lawsuits within 1-6 years, depending on state laws and policy terms.

Delays can lead to claim denial or reduced payouts. Deadlines vary by state and policy type, so always review your policy and confirm specifics with your insurer. If you're unsure, seek professional help to protect your rights.

Insurance Filing Deadlines by Type: Notice, Proof of Loss, and Lawsuit Timeframes

How to Find Filing Deadlines in Your Insurance Policy

Reading Policy Language

Insurance policies often rely on vague terms to outline reporting deadlines. Phrases like "immediately," "promptly," "as soon as practicable," or "within a reasonable period of time" are common, but they rarely spell out exact timeframes. For example, auto insurance policies might specify a 24 to 72-hour window for reporting an incident. On the other hand, homeowners' policies typically use less precise language, such as "as soon as practicable".

"The insurance policy is probably the most purchased yet least read contract in existence."

These phrases can mean different things depending on the policy. In one case, "promptly" might imply 24 hours, while in another, it could allow for several days. If you're unsure, it's always best to reach out to your insurer for clarification.

To track down specific deadlines, focus on certain sections of your policy.

Where to Look in Your Policy

Deadlines for filing claims are usually detailed in sections labeled "Notice of Loss," "Reporting Requirements," "Duties After Loss," or "Claims Process". For example, a "Proof of Loss" clause might require you to submit a sworn statement within 60 to 180 days.

Another important section is the "Suit Against Us" or "Legal Action" clause. This outlines how long you have to file a lawsuit if your claim is denied - typically between 1 and 2 years, even if state laws allow more time. Keep in mind that umbrella or excess insurance policies may have different requirements than your primary coverage.

| Deadline Type | Where to Find It | Typical Timeframe |

|---|---|---|

| Notice of Loss | Reporting Requirements / Duties After Loss | 24 hours – 60 days |

| Proof of Loss | Property Coverage / Claims Section | 60 – 180 days |

| Lawsuit Deadline | "Suit Against Us" / Legal Action Clause | 1 – 2 years |

If you're still unsure after reviewing the policy, it's time to contact your insurer.

Asking Your Insurance Provider for Help

Once you've identified ambiguous terms or sections in your policy, reach out to your insurer directly for clarification. Use the claims number on the back of your insurance card. Be specific with your questions, like: "What is the exact deadline for reporting this accident?" or "When is my proof of loss due?". After each conversation, email a summary of what was discussed, including any deadlines mentioned.

For terms like "promptly", request written clarification to avoid disputes later. In Texas, for example, insurers must acknowledge your claim within 15 business days. If you need more time, request an extension in writing before the original deadline passes and confirm the new date in writing.

If you're still stuck, consider contacting your state’s insurance department. In Texas, the Texas Department of Insurance helpline is available at 800-252-3439. For larger or more complicated claims, consulting an insurance attorney can help you navigate tricky clauses like "Suit Against Us" and ensure you meet all deadlines.

sbb-itb-6a9d141

What Happens If You Miss Filing Deadlines

Denied Claims and Lower Payments

Filing your insurance claim on time is more than just a formality - it’s a critical step in protecting your rights. Missing deadlines can result in your claim being denied outright, even if it’s valid and worth a significant amount of money. Most policies require you to report an incident “promptly” or “immediately,” such as by following the essential steps after an accident, which typically translates to a timeframe of 24 hours to 60 days. For example, if you wait a week to report an accident because you wanted to “assess the damage,” your insurer might argue that the delay invalidates your coverage.

Even if your claim isn’t denied, you could face reduced payments. Insurers often require a formal “proof of loss” document, which usually needs to be submitted within 60 to 180 days. Missing this deadline can lead to lower payouts or delays in processing your claim. Insurance companies may argue that your delay hindered their ability to investigate the scene, interview witnesses, or collect evidence while it was still fresh.

"Missing a deadline can permanently destroy your claim - even if you're owed thousands of dollars."

- Terms.Law

| Deadline Type | Typical Timeframe | Consequence of Missing |

|---|---|---|

| Policy Notice | 24 hours to 60 days | Can void coverage entirely |

| Proof of Loss | 60 to 180 days | Claim rejection or reduced settlement |

| Statute of Limitations | 1 to 6 years (varies by state) | Permanent loss of legal right to sue |

| Suit Limitation Clause | 1 to 2 years (contractual) | Overrides longer state legal deadlines |

Delays don’t just affect your payout - they can also violate the terms of your contract.

Legal and Contract Consequences

Failing to meet deadlines can have serious legal repercussions. Most insurance policies include provisions, such as a "Suit Against Us" clause, which limit the amount of time you have to file a lawsuit to as little as 1 or 2 years - even if your state’s statute of limitations allows for a longer period. Missing this contractual deadline weakens your ability to challenge a denied claim. Once that window closes, you lose any legal leverage to compel the insurer to pay.

"Once the threat of a lawsuit is gone - that is, once the statute of limitations expires - you have no way to force an insurance company to pay you."

- Dan Ray, Attorney

This issue is even more pressing when dealing with federal programs like National Flood Insurance or National Crop Insurance. These programs enforce strict compliance with filing deadlines, leaving little to no room for extensions unless granted by a federal official. For instance, missing a 60-day proof of loss deadline in these programs almost always results in losing your benefits entirely.

Typical Filing Deadlines and State Differences

Standard Vehicle Insurance Filing Deadlines

When filing a vehicle insurance claim, there are three key timelines to keep in mind. First is the policy notice deadline, which requires you to inform your insurer "promptly" or "immediately." This typically means notifying them within 24 hours to 7 days after an accident, depending on your policy. This step is simply about informing your insurer of the incident.

Next comes the proof of loss deadline. This is when you must submit a sworn statement that details the damages you’ve incurred. Insurers usually require this documentation within 60 to 180 days. Lastly, there’s the statute of limitations, which is the legal timeframe for filing a lawsuit if your claim is denied or underpaid. This period varies widely, typically ranging from 1 to 6 years, depending on your state and the type of damage involved.

If you live in a no-fault state, additional rules may apply. For instance, New York requires No-Fault (PIP) claims to be filed within 30 days, while Florida mandates that medical treatment for Personal Injury Protection must occur within 14 days. Missing these state-specific deadlines can seriously affect your ability to pursue a claim, even if you meet the general insurance policy requirements.

These timelines offer a general framework, but state laws often add further complexities. For more detailed information on navigating the aftermath of an accident, see our car accident guides.

How Deadlines Vary by State

Each state has its own rules that can significantly impact filing deadlines. For example, Louisiana has the shortest statute of limitations in the country, giving just 1 year for both personal injury and property damage claims. On the other hand, states like Maine and North Dakota allow up to 6 years for personal injury claims. Some states also differentiate between bodily injury and property damage deadlines. In Louisiana, both types of claims must be filed within 1 year, while California allows 2 years for injury claims and 3 years for property damage.

Recent legislative changes can also alter deadlines. In Florida, the statute of limitations for negligence-based personal injury claims was reduced from 4 years to 2 years for accidents occurring on or after March 24, 2023. These changes highlight the importance of staying up-to-date on your state’s laws, as they can shift over time.

Additionally, many states require that accidents be reported to the DMV or local authorities within a specific timeframe. For example, accidents involving property damage exceeding $1,000 often need to be reported within 10 days. Missing these reporting deadlines can further complicate your claim process.

How to Meet Your Filing Deadlines

Keeping Records of Accidents and Claims

Staying ahead of filing deadlines starts with thorough documentation of your accident and claims. Right after an accident, gather essential details like the names, contact information, and insurance policy numbers of everyone involved. Don’t forget to jot down license plate numbers and the 17-digit Vehicle Identification Number (VIN), which you can find on the dashboard or inside the door frame of each vehicle. Take photos of all damages and note key factors like weather conditions, road quality, and the direction the vehicles were traveling.

Organize everything into a "Master File." This should include copies of every document you send to your insurance company, such as receipts, medical records, repair estimates, and a list of any personal property damaged inside your vehicle. After every phone call with your insurer, follow up with a written record - whether it's an email or a letter - to create a solid paper trail. Also, keep a detailed log of your interactions with claims adjusters, noting names, dates, inspections, and any repair approvals.

Using Reminders and Staying Organized

A digital calendar can be a lifesaver when it comes to tracking deadlines. Set automated reminders for all critical dates, and make sure these align with the records in your Master File. Many insurance companies now offer mobile apps that let you report claims, upload photos, check deductibles, and track your claim’s status in real time. If your insurer grants an extension for filing paperwork, always get written confirmation.

It’s also wise to ask your claims adjuster directly about deadlines for filing claims, submitting bills, resolving disputes, and providing additional information. Keep all documentation for as long as your state’s statute of limitations allows, since legal action could arise long after the incident. If managing all these details feels overwhelming, seeking professional help can make the process more manageable.

Getting Professional Help

If you’re unsure about your deadlines or cutting it close to a critical one, professional help can make all the difference. Experts can clarify confusing policy terms and guide you through important deadlines. Legal counsel, in particular, can interpret complex policies and state laws, ensuring you don’t miss any key dates. They can also challenge an insurer’s claim that a delay harmed their investigation.

Services like Collision Help | Nationwide Accident Help streamline the process. By uploading photos of your vehicle damage through their secure platform, you can receive a tailored claim and repair plan - often within 24 hours and with no upfront cost.

Some insurance attorneys work on a contingency fee basis, meaning they only get paid if they recover money for you. If an insurer claims your delay affected their investigation, ask for a written explanation. If they can’t prove the delay caused harm, you may still be entitled to payment.

Conclusion: What You Need to Know About Filing Deadlines

Filing Deadline Basics

Filing deadlines usually fall into three main categories: immediate notice of loss (usually within 24 to 72 hours), formal proof of loss (requiring detailed documentation within 60 to 180 days), and the statute of limitations (ranging from one to six years to file a lawsuit if your claim is denied or underpaid).

These deadlines aren't optional - they're binding terms of your insurance policy. Many policies also include "Suit Against Us" clauses, which may shorten the filing period even further, sometimes limiting your timeframe to just one or two years. Keeping track of these deadlines is crucial to protect your rights and ensure you receive the compensation you're entitled to.

Final Tips for Policyholders

Here’s a quick recap to help you stay on track: Report any accidents immediately. Delaying could violate the notice requirements in your policy, putting your entire claim at risk. Use a calendar to set reminders for all key deadlines, and leave yourself at least a week of extra time to handle any unexpected issues.

Maintain a written record of all communications, and if you receive any deadline extensions, make sure they’re confirmed in writing. If you're unsure about how to proceed, consider seeking professional help. Services like Collision Help | Nationwide Accident Help can guide you through the process. They even allow you to upload photos of your vehicle damage securely and get expert support within 24 hours.

Missing This Deadline Will DESTROY Your Car Accident Claim (2026 Update)

FAQs

Does a late claim report always mean denial?

When a claim is reported late, it doesn't automatically mean it will be denied. Courts often examine whether the delay actually caused any harm to the insurer. Additionally, some states have rules requiring insurers to meet certain conditions before they can deny coverage based on late notice. It's always a good idea to carefully review the terms of your policy and consult a professional if you're unsure.

Can my insurer extend a proof-of-loss deadline?

Yes, insurers have the ability to extend proof-of-loss deadlines. These deadlines are typically detailed in your insurance policy and can also be impacted by state laws. For example, after Hurricane Ida, FEMA extended the standard 60-day deadline to 180 days for flood claims. To find out if an extension applies to your situation, review your policy or reach out to your insurer directly.

Which deadline controls: my policy or state law?

The time you have to file your claim depends on state law, specifically the statute of limitations, which can vary based on where you live and the type of claim you're making. While your insurance policy might outline certain timelines, state law will override those terms if there’s a conflict.