5 Tips for Picking a Rental Car After an Accident

When dealing with a car accident, choosing the right rental car can save you money and reduce stress. Here’s what you need to know:

- Match the car to your needs: Pick a vehicle similar to your own to maintain your routine. Check your insurance policy to ensure it covers the cost. This is especially important if your vehicle is declared a total loss.

- Understand insurance coverage: Review your policy and credit card benefits to avoid unnecessary add-ons. Watch out for "loss of use" fees.

- Set a budget: Daily rental rates average $57, but insurance often covers only $30–$50. Compare prices, avoid hidden fees, and look for discounts.

- Check rental terms: Be aware of duration limits, mileage restrictions, and repair delays that might affect coverage.

- Choose a reliable provider: Opt for rental companies with strong insurance partnerships and direct billing options to simplify the process.

Rental Car Insurance Coverage Costs and Options After an Accident

1. Match the Car Size and Features to Your Needs

Suitability for Post-Accident Needs (Size, Features, Comfort)

When choosing a rental car after an accident, aim for a vehicle that matches the size and class of your damaged car. Most insurance policies allow for a similar replacement, so you shouldn't have to settle for a downgrade. For instance, if you rely on a pickup truck for work or an SUV for your family, switching to a compact sedan could disrupt your routine. Sticking with a comparable vehicle helps maintain your daily life with minimal stress.

"If you drive a pickup and require a similar truck for work, don't be afraid to insist on what you need." - Car and Driver

Think about your specific needs before making a choice. A family of five, for example, will struggle to fit into an economy car, especially if car seats are involved. Insurance companies generally cover vehicles that match what you normally drive, so don't hesitate to request one that fits your lifestyle.

Also, check your insurance policy's daily reimbursement limit. This ensures you don’t end up paying out of pocket for a rental that's more expensive than your coverage allows.

Finally, practicality matters, especially if you're recovering from an injury. Consider how easy the car is to use. For example, while electric vehicles might seem appealing due to lower rates, their charging times can be a hassle. Charging for 150 miles can take 30 minutes, compared to just five minutes to refuel a gas-powered car - something to keep in mind during an already stressful time.

sbb-itb-6a9d141

How to get a rental car after an auto accident without paying out of pocket.

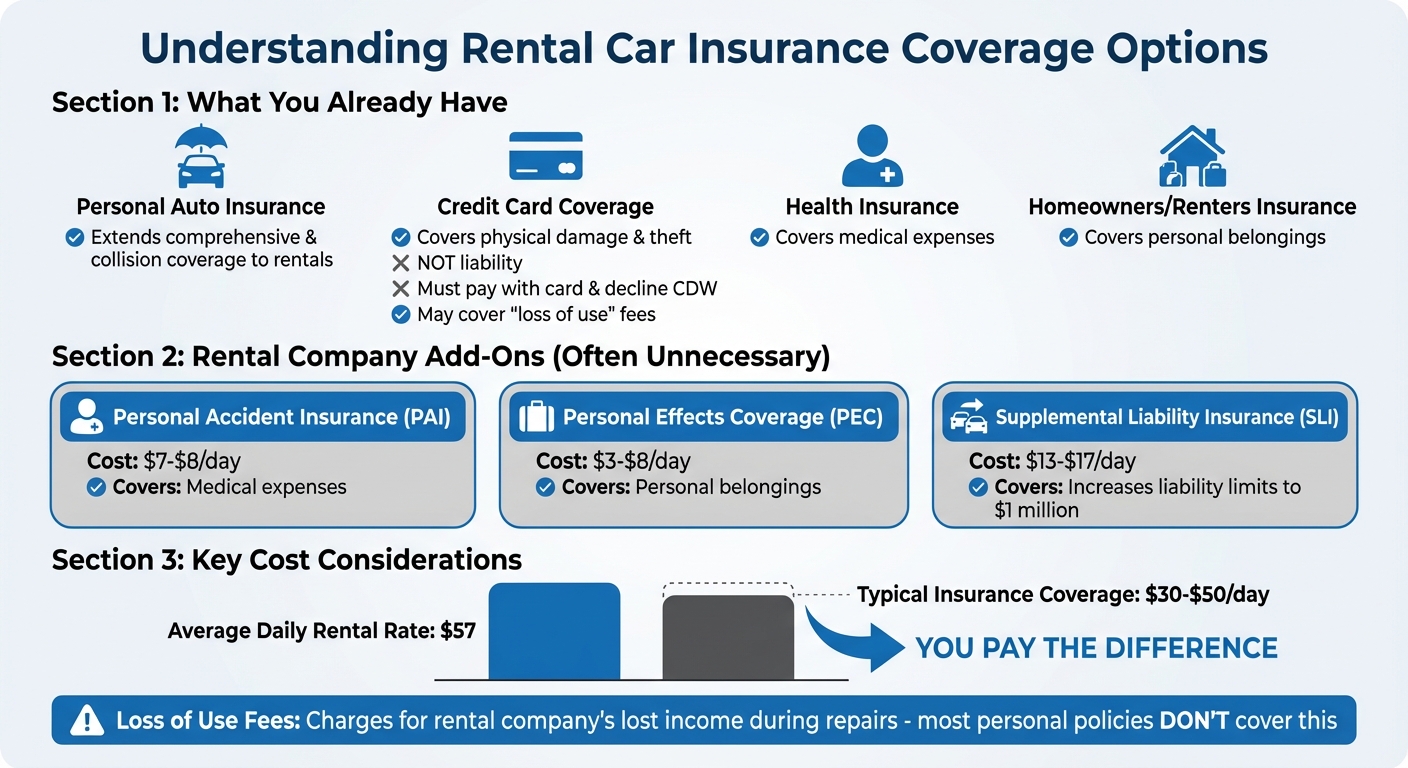

2. Know What Insurance Coverage You Need

Before renting a car, take a moment to review your current insurance coverage. If you already have comprehensive and collision coverage on your personal auto insurance policy, it likely extends to rental cars as well. To confirm, reach out to your insurance agent or check your policy's declarations page. Having clarity here can help you decide if you need any additional coverage.

Many credit cards offer coverage for physical damage and theft on rental cars, but they usually exclude liability protection. To activate this coverage, you must pay for the rental entirely with your credit card and decline the rental company’s Collision Damage Waiver (CDW).

It’s also important to understand "loss of use" fees. These are charges the rental company might impose for income lost while the car is being repaired. While most personal auto policies don’t cover these fees, certain credit cards might. Double-check your policy or card benefits to avoid unexpected costs.

Rental companies often offer extra coverage options, including:

- Personal Accident Insurance (PAI): Costs $7–$8 per day and covers medical expenses.

- Personal Effects Coverage (PEC): Costs $3–$8 per day and protects personal belongings.

- Supplemental Liability Insurance (SLI): Costs around $13–$17 per day and can raise your liability limits to $1 million, which is useful if your current policy has low limits or no liability coverage.

However, these add-ons are often unnecessary if you already have health insurance, homeowners insurance, or renters insurance that covers medical expenses and personal belongings.

"If you already have comprehensive and collision coverage, buying extra coverage for a rental car is generally unnecessary."

– Maya Afilalo, Managing Editor & Industry Analyst, AutoInsurance.com

Still unsure? You can always consult Collision Help | Nationwide Accident Help (https://collisionhelp.org) for advice on your coverage and claims process. Knowing exactly what your insurance covers can save you money and make your rental experience smoother.

3. Compare Prices and Set a Budget

Managing costs is just as important as finding a rental that fits your needs after an accident. The advertised daily rental rate often doesn’t tell the whole story, thanks to taxes, surcharges, and add-ons. For instance, while the average rental car in the U.S. costs around $57 per day, picking up at an airport can add an extra 10% to 30% due to additional fees. To sidestep these charges, consider using non-airport pickup locations or rideshare services to get to your rental. These unexpected expenses make it critical to set a clear budget upfront.

If your rental costs exceed your insurance policy’s daily limit - usually between $30 and $50 - you’ll be responsible for covering the difference. To save, ask about "accident rates" or special discounts for rentals tied to vehicle repairs. Companies like Enterprise and Hertz often provide these options.

It’s important to account for more than just the base rate. Extra charges like mileage overages and refueling fees can sneak up on you. For example, mileage overages can range from $0.10 to $0.50 per extra mile, refueling surcharges can hit up to $10 per gallon, and security deposits vary between $50 and $300, depending on the rental company’s policies. These hidden fees are a common pitfall - nearly 30% of travelers report paying more than they expected due to such charges.

"If the rental location is at the airport, the rental agency is contractually required to pay the concession fee to the airport."

– Neil Abrams, Founder, Abrams Consulting Group

To keep costs down, explore membership discounts and special partner rates. Memberships like AAA, Costco, or AARP can help lower daily rates and cut down on insurance add-on fees. Additionally, if your insurance provider has a preferred rental partner - such as GEICO with Enterprise or Allstate with Hertz - you might gain access to discounted rates and direct billing options.

4. Review Rental Duration and Mileage Limits

Understanding your rental terms can help you sidestep unnecessary costs. Most rental reimbursement policies cover up to 30 days. That’s usually enough, considering the average repair takes about two weeks. But delays - like waiting on parts or a busy repair shop - can eat into that time quicker than you'd expect.

If your car is declared a total loss, the rules shift. Rental coverage often ends just 2 to 5 days after the settlement is issued, even if you haven’t found a replacement car yet. So, once you receive the settlement, it’s crucial to act fast.

"Rental reimbursement coverage ends when your vehicle is repaired. If your car is repaired on Friday but you don't pick it up until Monday... you'll be responsible for Saturday's and Sunday's rental costs." – Karen Axelton, Senior Personal Finance Writer, Experian

When dealing with repairs, staying on top of the timeline is key. Keep tabs on the body shop’s progress and notify your adjuster immediately if delays might push you past your coverage limits.

Mileage limits are another thing to check. While your insurance might cover the daily rental rate, rental agreements often cap mileage - usually between 100 and 200 miles per day for local rates. If you’re driving long distances or crossing state lines, make sure you’re covered by an “unlimited” mileage plan. Be aware that some plans come with geographic restrictions.

5. Choose a Trusted Rental Provider

Once you've evaluated rental costs and coverage, the next step is selecting a reliable provider.

Different rental agencies handle accident-related rentals in their own way. Opt for providers with strong insurance partnerships. Well-known companies like Enterprise or Hertz often collaborate directly with major insurers, streamlining billing and rental extensions. This means you won't need to pay hundreds of dollars upfront and then wait weeks for reimbursement.

Some specialized rental services take it a step further by offering direct billing options. These services can reduce security deposits to around $50, compared to the usual $200–$300, and may even provide discounted insurance rates.

"Backed by more than 65 years of exceptional customer service, you can feel confident we'll take care of you during this experience." – Enterprise

It's also crucial to confirm that roadside assistance is included. Quick help is a lifesaver if you encounter issues during your rental period. Before finalizing your booking, double-check the details of roadside support, including any geographic limitations. Additionally, ask if the company offers pick-up services. Having someone pick you up from the repair shop or your home can be incredibly convenient when you’re temporarily without a vehicle.

Lastly, find out if the rental agency communicates directly with collision repair shops. Top providers will automatically extend your rental if repairs take longer than expected, saving you from the hassle of rebooking or unexpected out-of-pocket costs. Picking the right provider not only helps control expenses but also simplifies the claims process.

For more advice on managing rental options, handling insurance claims, and working with preferred providers after an accident, visit Collision Help | Nationwide Accident Help at https://collisionhelp.org.

Conclusion

The tips outlined above provide a practical guide to simplify the rental process after an accident. Picking the right rental car doesn’t have to add to your stress. Focus on matching the vehicle to your needs, reviewing your insurance limits, budgeting wisely, understanding the rental terms, and choosing a trusted provider. These steps aim to help you stay on track during repairs while managing costs effectively.

Planning ahead is crucial. Check your policy’s daily rental limits - typically between $30 and $50 per day - before securing a rental. Keep all receipts, agreements, and correspondence with your insurer to ensure a smooth claims process.

"Knowing how to get a rental car from an insurance claim can help alleviate some of the stress resulting from an accident." – Idalia Garcia, Insurance Editor

Most insurance policies cover rentals for up to 30 days, while the average repair takes about two weeks. Staying in touch with your collision repair shop can help you manage rental extensions if repairs take longer than anticipated.

For assistance with insurance claims, repair coordination, or understanding your coverage, Collision Help | Nationwide Accident Help offers expert support within 24 hours. You can upload photos of your vehicle damage at https://collisionhelp.org to receive a tailored plan for your claim and rental needs. This service helps reduce hassle and ensures a smoother experience until your car is back on the road.

FAQs

What should I do if my insurer only covers a cheaper rental than I need?

Adding rental reimbursement coverage to your auto insurance policy can help you avoid similar problems down the road. This coverage ensures you have access to a rental car if your vehicle is out of commission due to an accident. Additionally, you might want to see if the at-fault driver's insurance can cover a rental that's a better fit for your needs. Keep in mind, standard policies often come with limits, so it's worth reviewing your coverage details and these alternatives to make sure you're prepared.

Do I need the rental company’s insurance if I already have auto insurance or a credit card?

If you already have personal auto insurance or use a credit card that offers rental car coverage, you might not need the insurance offered by the rental company. That said, it’s important to take a closer look at your existing policies to see what they actually cover - like liability or collision protection - before deciding to skip the rental company’s options. Make sure you’re aware of any gaps in coverage to avoid surprise expenses later.

How can I avoid extra rental charges like loss-of-use, mileage, and airport fees?

To steer clear of extra rental charges, there are a few smart strategies to keep in mind. First, consider using your own insurance coverage instead of purchasing the rental company's options. Second, avoid picking up the car at the airport, as this often comes with added surcharges. Third, decline any add-ons you don’t need, like GPS or roadside assistance. Fourth, take the time to compare prices across different rental companies to find the best deal. Lastly, thoroughly inspect the car for any pre-existing damage before driving off to avoid being held responsible later. These simple steps can help you sidestep fees like loss-of-use charges, mileage overages, and airport-related costs.