5 Consequences of Filing Claims Late

Filing an insurance claim late can lead to serious financial and legal problems. Here’s what you need to know:

- Your claim might be denied: Most insurance policies require you to report accidents within 24–72 hours. Missing this window gives insurers the right to reject your claim.

- You pay out of pocket: Without a timely claim, you’ll cover repair costs, medical bills, and other expenses yourself.

- Policy cancellation: Filing late can violate your insurance contract, leading to policy termination or higher future premiums.

- Reduced payouts: Delays weaken evidence, making it easier for insurers to reduce your settlement.

- Loss of legal rights: Missing deadlines, like the statute of limitations, can permanently block you from suing for compensation.

Act quickly after an accident - report incidents immediately, document everything, and stay informed about deadlines in your state. Even minor delays can cost you thousands of dollars.

State-by-State Insurance Claim Filing Deadlines and Statute of Limitations

The Hidden Reasons Your Car Accident Claim Is Delayed

sbb-itb-6a9d141

1. Your Claim Gets Denied

Missing your policy's deadline is one of the fastest ways to have your claim rejected. Insurance policies are legally binding contracts, and failing to report an incident within the required timeframe gives your insurer the legal right to deny your claim outright.

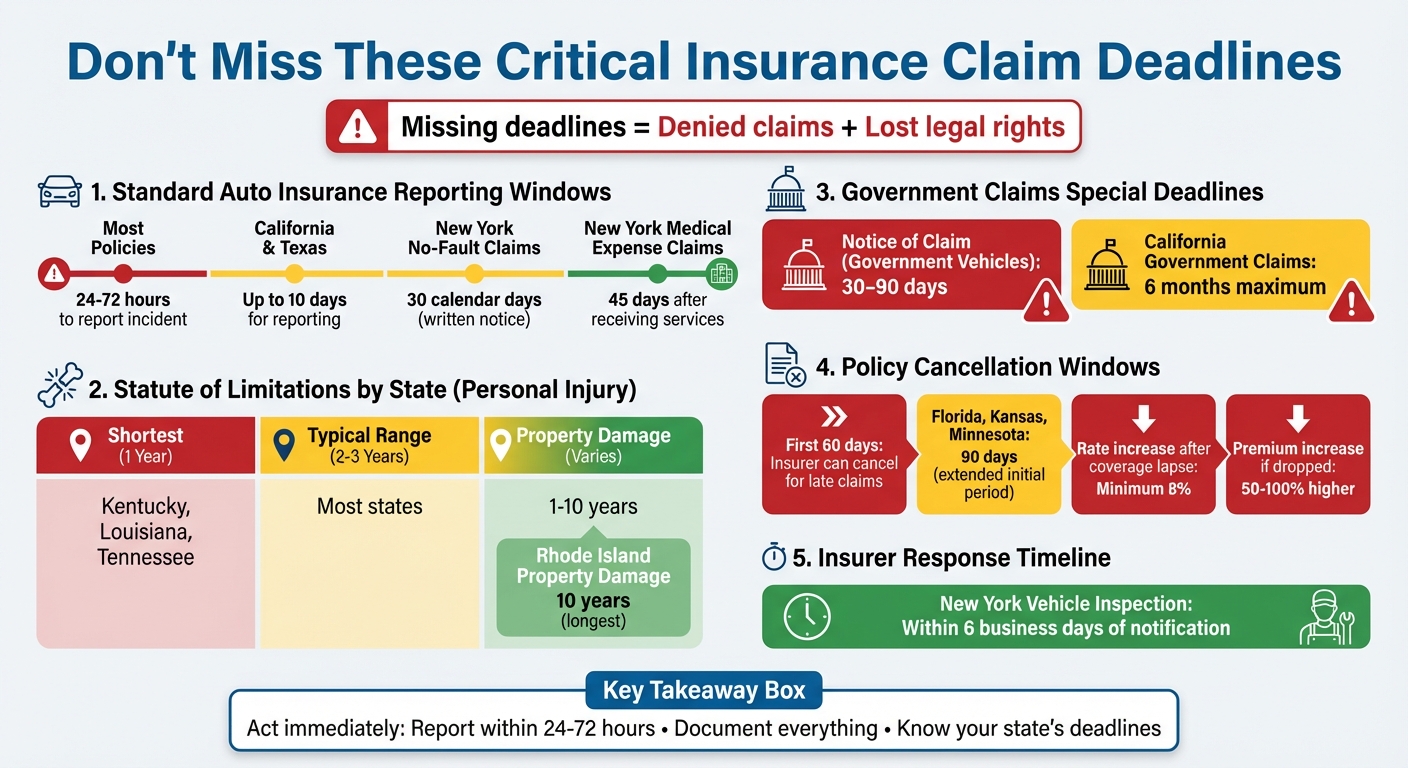

Most auto insurance policies require you to report an incident within 24 to 72 hours. However, some states, like California and Texas, provide a bit more leeway, allowing up to 10 days for reporting.

As Karl Susman, President of Susman Insurance Agency, explains:

"The policy language telling you to report claims promptly isn't a friendly suggestion - it is a requirement."

These deadlines aren't arbitrary. They're in place to ensure that investigations remain effective. Delays can compromise evidence - physical proof can deteriorate, and witness memories can fade. When this happens, insurers may argue that the delay has hindered their investigation and deny your claim.

The pressure is even greater in states with stricter timelines. For example, in New York, you must submit written notice for a No-Fault claim within 30 calendar days of the accident. For medical expense claims, notice must be provided within 45 days of receiving services. Missing these deadlines could leave you paying hefty expenses out of pocket.

To avoid these risks, report the incident as soon as possible. Many insurers allow you to open an "incident file" without it counting as a formal claim, which helps preserve your rights while giving you some flexibility.

If you’re feeling overwhelmed by these tight deadlines, organizations like Collision Help | Nationwide Accident Help (https://collisionhelp.org) can provide expert advice to guide you through the insurance claim filing process.

2. You Pay All Expenses Yourself

Filing late means you're on the hook for every expense after an accident. Even what seems like a minor fender bender can hide serious issues, like a damaged axle or weakened bumper components. Licensed Insurance Agent Brandon Frady puts it plainly:

"If you don't notify your insurance provider, you might have to pay for those unexpected expenses with your own cash".

This goes beyond just repair costs. You'll also be footing the bill for towing, storage, rental cars, and even medical expenses. And if you miss the deadline for Personal Injury Protection (PIP) claims, you’re left covering hospital stays, doctor visits, and physical therapy entirely out of pocket. Each state has strict deadlines for filing claims, and missing them means you're financially responsible for everything.

Delays can also let small problems snowball into bigger, costlier ones. For example, a tiny dent that could have been fixed cheaply might lead to rust, and if your insurer sees the damage as preventable, they might refuse to cover it. In cases of stolen or totaled vehicles, filing late could mean losing out on recovering the vehicle's actual cash value, including sales tax.

For more tips on navigating these tricky situations, check out Collision Help | Nationwide Accident Help (https://collisionhelp.org).

3. Your Policy Gets Canceled

Filing a claim late doesn't just risk rejection - it could lead to your entire policy being canceled. Most insurance policies include a "Notice of Loss" clause, which requires you to report accidents "promptly", often within 24 to 72 hours for auto insurance. Missing these deadlines violates the terms of your contract, giving insurers the right to cancel your coverage.

During the first 60 days of your policy (or 90 days in states like Florida, Kansas, and Minnesota), insurers can cancel for late claims or unreported accidents. Even after this initial period, late filings can still lead to mid-term cancellations if they’re deemed a material misrepresentation - essentially, a breach of trust. Christopher Boggs, Vice President of Education at Insurance Journal's Academy of Insurance, clarifies:

"A 'material misrepresentation' is a dressed-up term for a lie. This means the insured lied about a material fact".

When a policy is canceled, it doesn’t just end your current coverage - it creates a domino effect of legal and financial headaches.

Late filings can also hurt you long-term. A pattern of delayed claims may result in non-renewal at the end of your policy term, making it harder and more expensive to secure future coverage. Insurers use databases like the Comprehensive Loss Underwriting Exchange (CLUE) to track your claims history, and repeated violations flag you as a high-risk customer. If you’ve been dropped, expect to pay 50% to 100% more for a new policy compared to someone with a clean record.

If your policy is canceled, you’ll receive a written notice explaining the reason and effective date. Each state has specific rules about how much notice you’ll get. But even a brief lapse in coverage can increase your future rates by at least 8%. In some cases, you might be forced into a state "assigned risk" plan, which guarantees coverage but at much higher premiums.

The best way to avoid all this? Report accidents immediately, even if they seem minor. Waiting to "see how bad it is" could lead to policy violations, leaving you with expensive premiums - or worse, no coverage at all.

4. Your Claim Gets Questioned and Reduced

Filing a claim late doesn't just risk outright denial - it often leads to heightened scrutiny and lower settlement offers. Insurers tend to see delays as warning signs, and as time passes, it becomes increasingly difficult to verify the details of your claim.

A major factor here is the deterioration of evidence. When an adjuster reviews your case weeks or months after the incident, they’re often working with incomplete information. Physical evidence may have disappeared, and witnesses may struggle to recall key details. As Karl Susman, President of Susman Insurance Agency, explains:

"Insurance claims are part storytelling, part proof. The longer you wait, the more the story gets fuzzy and the more likely the proof gets harder to come by".

This lack of clarity generally benefits the insurer. Without strong evidence, adjusters base settlements only on what they can confirm. They may also argue that you failed to take timely action to prevent further damage. For example, if a small leak turns into major water damage because of delays, the insurer might reduce your payout. In New York, insurers are required to inspect damaged vehicles and make a good faith settlement offer within 6 business days of being notified. Delaying your report can disrupt this timeline and make them less willing to settle.

Delays can also raise suspicions of fraud, leading to more thorough investigations and smaller settlement offers. In short, waiting to file doesn’t just complicate the process - it can significantly reduce the amount you recover.

Even if you have receipts and photos, late claims often result in lower payouts. Insurers may only cover damages they can independently verify, leaving you to cover the rest. To avoid this, document everything immediately - take photos from every angle right after the incident and report the loss to your insurer as soon as possible.

5. You Lose Your Right to Sue

Missing the filing deadline for your claim can mean permanently losing your right to sue. Once the statute of limitations runs out, courts will dismiss your case. Attorney Stacy Barrett explains it plainly:

"If you miss the filing deadline, a judge will likely have no choice but to dismiss your lawsuit and you'll lose your chance to get compensation for your injuries and losses."

The time limits for filing - known as statutes of limitations - differ by state. For personal injury claims, they typically range from 2 to 3 years, though some states, like Kentucky, Louisiana, and Tennessee, only allow 1 year. Property damage claims can have statutes ranging from 1 to 10 years, with Rhode Island permitting the longest window at 10 years. Missing these deadlines is just as damaging as weakened evidence; it effectively eliminates your ability to sue.

Late filing doesn’t just hurt your case - it completely undermines your legal options. Negotiating with the insurance company doesn’t stop the clock, and adjusters aren’t obligated to warn you about deadlines. If negotiations drag on and the deadline passes, you lose the leverage needed to compel the insurer to pay. Attorney Dan Ray sums it up:

"The statute of limitations, in other words, is a claim killer."

The situation is even more urgent with government-related claims. For instance, if your accident involves a public vehicle, like a city bus or mail truck, you may have as little as 30 to 90 days to file a formal notice of claim. In California, government claims must be submitted within 6 months. Missing these strict deadlines usually means you can’t file a lawsuit at all.

To protect your rights, find out your state’s filing deadline immediately after an accident. Don’t rely on the insurance company to settle in time - if negotiations stall, you may need to file a lawsuit to keep your claim alive. Missing the deadline, even by a single day, means forfeiting your right to compensation.

Conclusion

Missing an insurance claim deadline isn't just inconvenient - it can lead to serious financial and legal consequences. As we've discussed, late filing can result in denied claims, higher out-of-pocket expenses, policy cancellations, reduced settlements, and even the loss of legal options.

When it comes to insurance claims, time is critical. Most auto insurance policies require you to notify your insurer within 24 to 72 hours of an accident. These deadlines are not optional - they're part of your contract. As Karl Susman, President of Susman Insurance Agency, puts it:

"The fastest way to turn a covered loss into an uncovered one is to treat the notice requirement like it's a suggestion".

Delays can severely weaken your claim. Evidence can vanish, memories fade, and additional damage may occur - all while the statute of limitations ticks away. For example, in states like Kentucky and Louisiana, you only have one year to file a lawsuit for personal injury. Missing that deadline, even by a single day, could mean losing your legal rights, no matter how strong your case might be.

Acting quickly is your best defense. Report the accident as soon as you're safe, document everything with photos and videos, and follow up phone notifications with written confirmation to create a strong paper trail. If you're unsure whether to file a claim, report the incident anyway - many insurers allow you to open an incident file to protect your rights without committing to a formal claim.

When time is tight and the process feels overwhelming, professional help can make all the difference. Collision Help provides nationwide support for insurance claims, vehicle repairs, and total loss disputes after an accident. By uploading photos of your vehicle damage, you can receive expert guidance within 24 hours through a secure and simple process. With deadlines looming and so much at stake, having expert assistance ensures you meet every requirement and protect every dollar you're entitled to.

FAQs

What counts as “prompt notice” for my insurance claim?

“Prompt notice” refers to reporting your insurance claim as quickly as you reasonably can. This usually means within a few days, but it’s often required no later than 30 days, depending on your insurance policy and state regulations. Delaying this step can cause problems, so it’s crucial to review your policy for exact deadlines and take action promptly after an incident.

Can I report an accident without filing a formal claim yet?

Yes, you can notify your insurer about an accident without immediately filing a formal claim. However, waiting too long to report it might create issues if you decide to file a claim later. Delays could lead to penalties or even a denial of coverage. To avoid potential problems, it’s a good idea to let your insurance company know about the accident as soon as you can.

Do insurance negotiations pause the statute of limitations?

No, negotiating with your insurance company does not stop the statute of limitations clock. The time limit for filing your claim keeps running, even if you're in active discussions with the insurer. To protect your right to seek compensation, ensure you file your claim within the legally allowed timeframe.