How to Document Damage for Supplemental Claims

When dealing with supplemental insurance claims for car damage, documenting everything thoroughly and acting promptly is key. Supplemental claims cover hidden or newly discovered damage missed during the initial inspection. Here's how to handle it effectively:

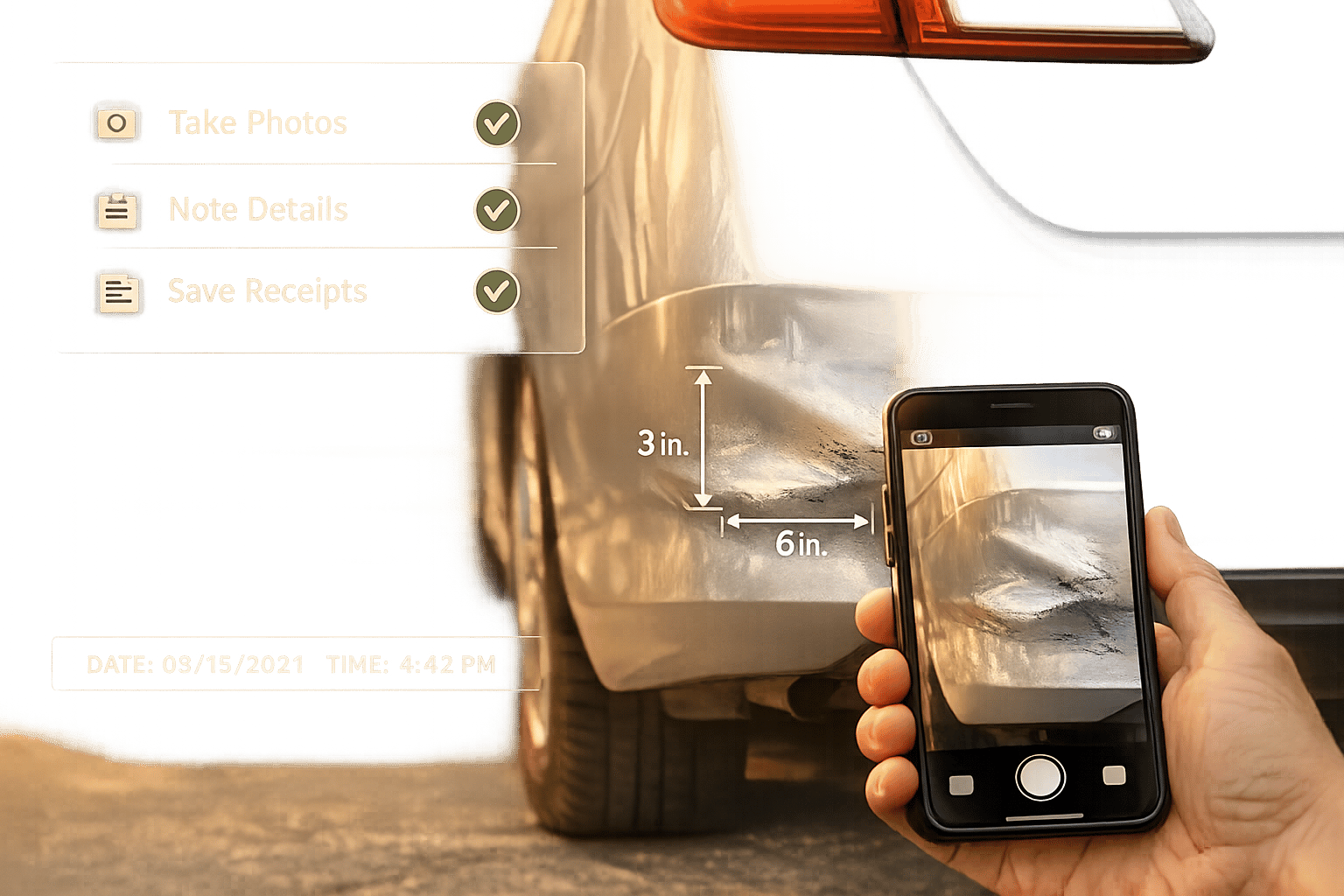

- Take detailed photos: Capture the damage from multiple angles (use the 8-point clock method) and include the license plate, VIN, and any debris or skid marks.

- Record details: Note weather, road conditions, and any other context. Use voice memos if needed.

- Collect evidence: Gather repair estimates, receipts, accident reports, and witness statements. Keep a log of all interactions related to the claim.

- Communicate with your insurer: Report new damage as soon as you notice it. Use email or your insurer’s app to keep a record of all communication.

- Submit your claim properly: Include a clear claim letter with all supporting documents. Use your insurer’s portal or Certified Mail for submission.

Timely action and organized records can help avoid delays or disputes. Always back up your evidence and follow up regularly with your insurer to ensure your claim progresses smoothly.

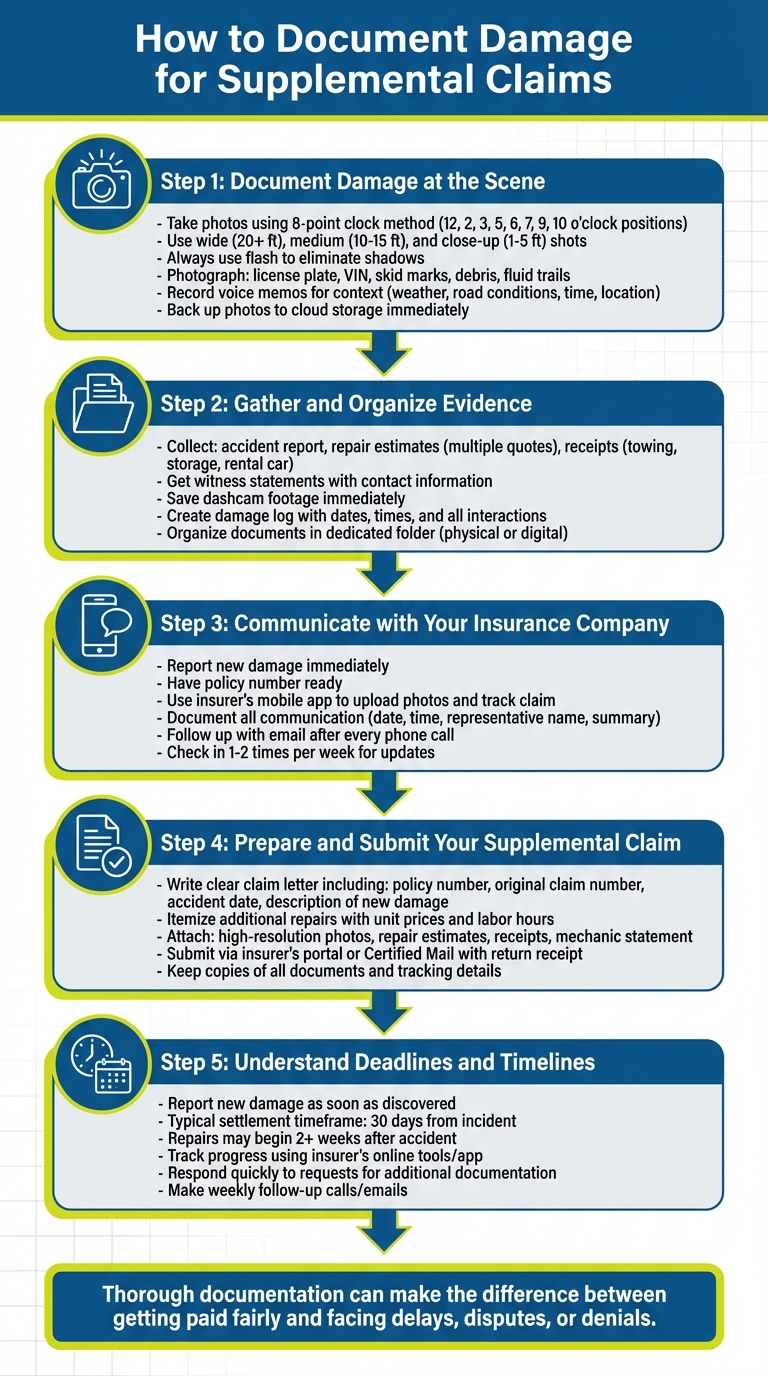

5-Step Process for Documenting Damage in Supplemental Insurance Claims

Get the Most from Your Property Damage Claim After a Car Accident!

Step 1: Document Damage at the Scene

When you're dealing with a car accident, documenting the damage right away is crucial for building a strong supplemental claim. Make sure to gather evidence before vehicles are moved or debris is cleared - this can be a game-changer for uncovering hidden damage later on. A well-documented scene lays the groundwork for a solid claim.

Take Complete Photos

Start by taking a variety of photos to capture the scene and the damage in detail. Use wide shots (20+ feet away), medium shots (10–15 feet), and close-ups (1–5 feet) to ensure you’ve got every angle covered.

Follow the 8-point clock method for photographing your vehicle:

- Front (12 o'clock)

- Both front corners (2 and 10 o'clock)

- Both sides (3 and 9 o'clock)

- Both rear corners (5 and 7 o'clock)

- Back (6 o'clock)

Always use your camera’s flash, even in bright sunlight, to eliminate shadows that might obscure damage. Avoid editing or applying filters to your photos to keep the timestamps and metadata intact.

"Photos can be the best evidence for showing how an accident happened. They also help you remember specifics about how the accident occurred." – Leah Hancock, Material Damage Reinspector, Erie Insurance

Don’t forget to photograph your license plate and VIN (found at the base of the driver’s side windshield) to confirm your vehicle’s identity. Additionally, document skid marks, fluid trails, shattered glass, and any debris or vehicle parts on the road. These details might prove essential if you need to file a supplemental claim down the line.

Record Context and Details

Capturing the broader context of the accident can further strengthen your claim. Take photos of weather conditions, road surfaces, traffic signs, street signals, and nearby landmarks to provide a sense of scale and distance. For example, if the sun was glaring or the road was slippery, these images can help address any disputes about visibility or road conditions.

If you’re unable to jot things down immediately, record a quick voice memo. Mention details like the time, location, weather, and any sounds or sensations you noticed during the impact. Also, look for nearby security or traffic cameras that might have recorded the incident - you might need this footage later on.

Finally, back up all your photos and videos as soon as possible. Upload them to cloud storage or email them to yourself to ensure the originals are safe and accessible.

Step 2: Gather and Organize Evidence

Once you've taken photos, the next step is to collect all the documents that back up your supplemental claim. This includes official reports, repair estimates, receipts, and witness statements. One of the most important items to request right away is the accident report. Use the incident number and the officer's name you noted at the scene to obtain it. Why is this report so crucial? As attorney David Goguen explains:

"Insurance adjusters, judges, and jurors value law enforcement officers' training and experience and may decide in your favor based on the officer's findings alone".

With this report in hand, focus on gathering everything else needed to build a strong case.

Collect Supporting Documents

Start by securing all official records and estimates to complement the photos you took at the scene. Make sure to have your vehicle’s 17-digit VIN and license plate details handy. Get written repair estimates from several body shops - having multiple quotes can help if the insurer questions costs. Keep receipts for any towing, storage fees, rental cars, taxis, or public transit you used while your car was out of service. If you have dashcam footage, save it immediately to prevent it from being overwritten. Additionally, collect the names, phone numbers, and statements of any witnesses who saw the accident.

Maintain a Damage Log

Keeping a chronological damage log can make a big difference in how smoothly your claim process goes. Use this journal to document how the accident has impacted your daily life. Record dates, times, and summaries of every interaction with insurance adjusters, body shops, and towing companies. Note any missed workdays, canceled appointments, or activities you couldn’t participate in because of the damage. These specific details are invaluable if the insurer questions your claim. Writing short, daily entries ensures accuracy and saves you from trying to recall events weeks later.

Organize Photos and Documents

Create a dedicated folder - physical or digital - for everything related to the accident and repairs. Upload your original photos to cloud storage or email them to yourself to preserve timestamps and metadata. Sort receipts into categories like towing and storage fees, rental car invoices, initial repair estimates, and final bills. Keep a detailed log of all communications, including claim numbers and summaries of conversations. To ensure nothing gets lost, back up all files in a secure digital folder. For professional advice, you can even upload your damage photos to Collision Help (https://collisionhelp.org) for a free evaluation.

Step 3: Communicate with Your Insurance Company

Once you've gathered your evidence, it's time to get in touch with your insurance company. Don’t delay - reach out as soon as you notice any additional damage, no matter who was responsible for it. When you contact them, have your policy number handy and be prepared to give a clear, factual description of the newly discovered damage. As Nationwide points out:

"The more information you have regarding your vehicle's damage, the more prepared you'll be when you contact your insurer".

Many insurance companies now offer mobile apps that make the process more convenient. You can use these apps to upload photos of the damage, check your deductible, and track the status of your supplemental claim in real time. By taking advantage of these tools, you can ensure that all new details are documented and addressed promptly.

Report Newly Found Damage

The moment you spot damage that wasn’t included in the initial estimate, call or email your insurer. Provide your vehicle's identification details and explain exactly what you’ve discovered - stick to the facts. If an adjuster is sent out to inspect the new damage, confirm their identity and keep a record of their observations. If they give you the green light to start repairs, make sure you get that approval in writing, along with any specific instructions or restrictions.

Document All Communication

Start a communication log from the very first interaction. Note the date, time, the name of the representative you spoke with, and a summary of the conversation. This log will help you stay organized and avoid disputes later. As Nolo cautions:

"Memories fade and insurance claims and lawsuits can drag on".

After every phone call, follow up with an email summarizing the discussion. This creates a permanent, timestamped record of what was said. Be sure to save all claim numbers, emails, and other correspondence. Back up these files in at least two places, like a cloud service and an external drive, to keep them safe.

Follow Up Regularly

Don’t let your claim fall through the cracks - stay on top of it by following up consistently. Check in with your insurer once or twice a week for updates. If part of your supplemental claim gets denied or the estimate feels off, ask for a written explanation. This should include how they calculated the amount and what policy limits were applied. If you’re not satisfied with their answers or can’t reach an agreement, don’t hesitate to request a conversation with a claims manager. Persistence is key to ensuring that all supplemental damage is addressed and your claim progresses smoothly.

sbb-itb-6a9d141

Step 4: Prepare and Submit Your Supplemental Claim

Now that you've gathered and organized your evidence, it’s time to put together your supplemental claim. A well-prepared submission can make the approval process much smoother. Here’s how to ensure your claim is complete and ready to go.

Write a Clear Claim Letter

Start by drafting a straightforward claim letter. Be sure to include key details like your policy number, original claim number, the date of the accident, and a concise explanation of the situation. Cover the basics - who, what, when, where, why, and how. Specifically, describe the newly discovered damage and explain why it wasn’t visible during the initial inspection. For instance, if a body shop uncovered frame damage after removing a bumper, include that detail in your letter.

Break down the additional repairs needed into clear, itemized sections. Include unit prices, quantities, and labor hours for each repair. Specify the total dollar amount you’re requesting to cover the supplemental damage, and set a reasonable response deadline for the insurer - usually 15 to 30 days.

"The demand letter represents the first step in the vehicle damage settlement negotiation process. In the letter, you will spell out your vehicle damage claim, including the details of the underlying accident, how you dealt with the damage to your vehicle, and the costs you faced as a result of the accident."

Once your letter is ready, gather all supporting documents to back your claim.

Attach All Supporting Documents

The evidence you’ve collected plays a crucial role in strengthening your claim. Include high-resolution, date-stamped photos of the damage, a detailed repair estimate for the additional work, the final invoice (if available), the original incident report, and receipts for any extra expenses you’ve incurred. A written statement from a mechanic or specialist explaining why the damage wasn’t apparent during the initial inspection can add credibility to your case.

"Strong evidence can help support a successful car insurance claim and reduce the odds of a claim denial that leaves you paying out of pocket."

Submit Through Approved Channels

How you submit your claim is just as important as what you submit. Many insurance companies provide online portals or mobile apps for supplemental claims, allowing you to track your submission and receive confirmation numbers instantly.

For added security, consider sending your claim via Certified Mail with a return receipt. This ensures you have proof of submission and can help prevent disputes or delays. In some cases, your body shop may handle the submission directly with the insurer. Always keep copies of all documents and tracking details. For example, in Texas, insurers are required to acknowledge receipt of your supplemental claim within 15 days and must decide to accept or reject it within 15 business days after receiving all necessary documentation.

If you’re unsure at any point during the process, services like Collision Help | Nationwide Accident Help can provide expert guidance. Their secure online platform allows you to upload photos of your vehicle damage and receive professional advice within 24 hours.

Step 5: Understand Deadlines and Timelines

Know Filing Deadlines

When it comes to filing supplemental claims, sticking to deadlines is non-negotiable. Most insurance policies require you to report any newly discovered damage as soon as possible, but the exact timeframe can vary depending on your policy. For auto insurance claims, settlements typically occur within 30 days of the incident. However, this can take longer if additional damage is found later or if you're in the middle of medical treatment.

Take a close look at your policy to find specific deadlines for filing claims and submitting documents. These details are often buried in sections like "Conditions" or "Exclusions", so you'll need to read carefully. Meeting these deadlines is crucial to avoid unnecessary delays in processing your claim.

In some cases, vehicle repairs might not begin until at least two weeks after an accident, as adjusters work on comparing estimates. During this time, hidden damage might come to light. That’s why it’s important to stay in touch with both your repair shop and your insurer. Once you’ve met all deadlines, keep an eye on your claim to ensure it moves forward smoothly.

Track Progress After Submission

After you’ve filed your supplemental claim on time, keeping track of its progress is just as important. Many insurers now offer online tools or apps that let you check updates, upload additional documents, and manage your claim in real-time. If your insurer doesn’t provide digital tracking, you’ll need to stay proactive by reaching out to your adjuster regularly. A weekly phone call or email - including your claim number and a summary of the conversation - can go a long way.

If your insurer asks for more documentation, don’t delay. Quickly submitting items like repair estimates or police reports can help keep the process on track. Prompt responses show you’re actively engaged and can help avoid unnecessary hold-ups.

Conclusion

Achieving success with a supplemental claim boils down to three key practices: thorough documentation, clear communication, and timely action. As James Shaffer, a seasoned writer and auto insurance expert at InsurancePanda.com, explains:

"Thorough documentation can make the difference between getting paid fairly and facing delays, disputes, or denials".

Insurance companies meticulously review every claim, so your evidence must leave no room for doubt. This means gathering detailed records from the accident scene, keeping your financial documentation well-organized, and maintaining a comprehensive log of all communications - steps we've discussed earlier.

Beyond collecting solid evidence, prompt and precise communication with your insurer is just as important. Notify your insurer of any new damage as soon as possible, and be quick to provide any additional information they request. While most auto insurance claims are resolved within 30 days, delays in submitting documentation can drag out this process. To protect yourself, use email for all correspondence, ensuring you have a permanent record of every interaction.

Attorney Charles R. Gueli emphasizes the importance of visual evidence:

"Photographs taken at the car accident scene are powerful evidence that will help you get maximum compensation".

FAQs

What details should I include when documenting vehicle damage for a supplemental claim?

When documenting vehicle damage for a supplemental claim, make sure to take clear, well-lit photos from different angles, along with close-up shots of the damaged areas. It's also important to photograph any existing damage to provide a full picture. Include photos that align with repair estimates to strengthen your case. Don’t forget to provide the vehicle's VIN (Vehicle Identification Number), relevant repair or towing invoices, and a detailed description of the damage. These steps help ensure your claim is handled efficiently and without unnecessary delays.

What steps can I take to speed up the processing of my supplemental claim?

To speed up your supplemental claim process, it's crucial to document any additional damage thoroughly. Start by taking clear, well-lit photos of your vehicle. Capture multiple angles, focusing on the damaged areas while also showing the car's overall condition. Good lighting and varied perspectives can provide a clearer picture of the situation.

Submit detailed reports or repair estimates that align with the guidance from your insurance adjuster. Make sure to send in all required documentation promptly, as delays can stall the process. If you're uncertain about any part of the claim, it might be helpful to consult a professional to ensure everything is accurate and complete.

What can I do if my supplemental insurance claim is denied?

If your supplemental claim gets denied, the first step is to carefully go through the denial letter. This will help you understand why the decision was made. Next, gather more supporting evidence to reinforce your case. This could include detailed photos of the damage, updated repair estimates, or written statements from mechanics.

With this additional documentation in hand, you can try appealing directly to your insurance company. Another option is to submit a formal demand letter, asking them to reconsider their decision. If the matter still isn’t resolved, it might be time to consult with a legal professional or an expert in insurance claims for more help.