Auto Insurance Fraud vs. Honest Mistakes

Filing an auto insurance claim can sometimes lead to confusion between an honest mistake and fraud. The difference comes down to intent. Fraud involves deliberately deceiving your insurer for financial gain, like staging accidents or inflating repair costs. Honest mistakes, on the other hand, are unintentional errors, such as typos or misinterpreting policy terms.

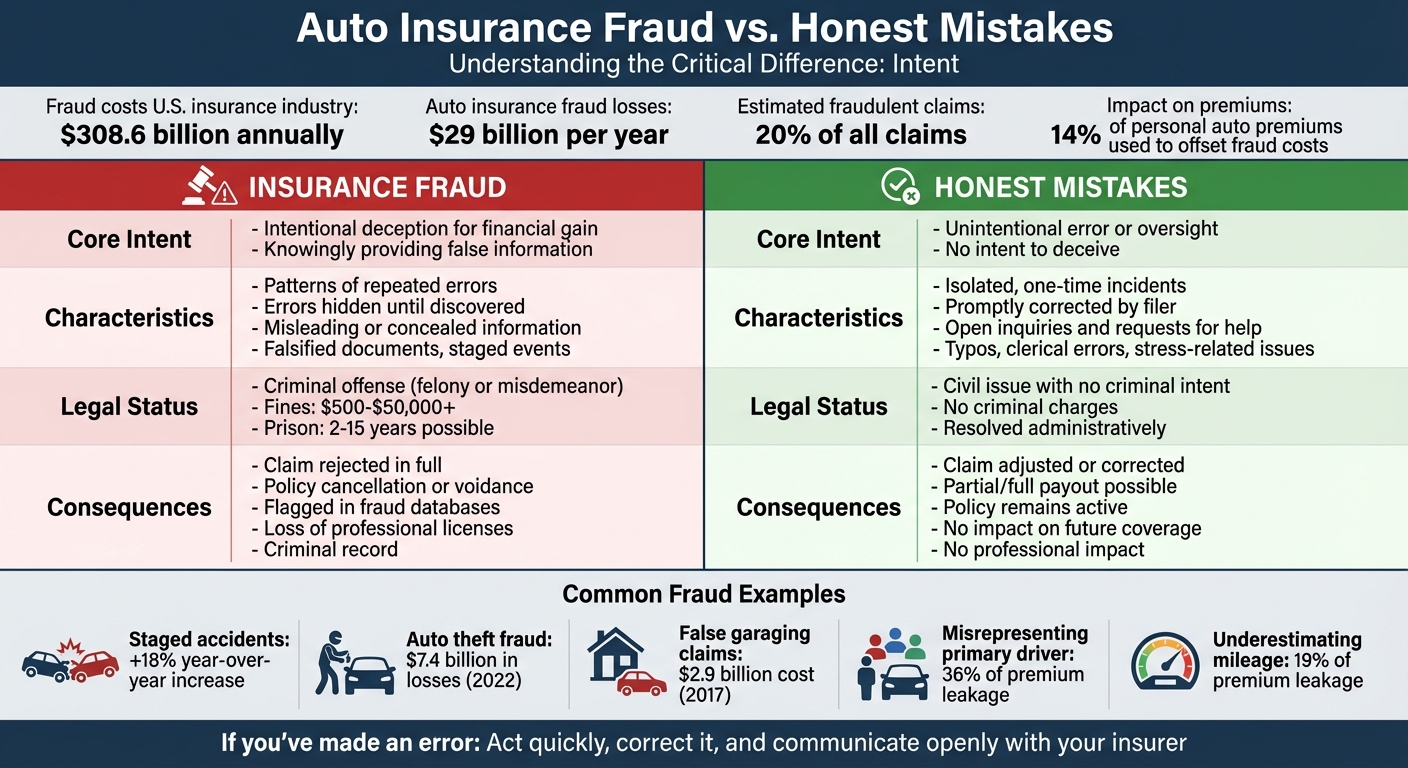

Fraud is a serious issue, costing the U.S. insurance industry over $300 billion annually, with 20% of claims estimated to be fraudulent. Legal penalties for fraud include fines up to $50,000 or more, jail time, and loss of coverage. Honest mistakes, however, are typically resolved through corrections without legal consequences, as long as they are addressed promptly and transparently.

Key Differences:

- Fraud: Intentional deception; criminal penalties.

- Honest Mistakes: Unintentional errors; resolved administratively.

If you’ve made an error, act quickly to correct it and communicate openly with your insurer to avoid complications.

Auto Insurance Fraud vs Honest Mistakes: Key Differences and Consequences

How insurance fraud is caught and stopped!

sbb-itb-6a9d141

What Is Auto Insurance Fraud?

Auto insurance fraud involves deliberately deceiving an insurer for financial gain. It’s not just a mistake or misunderstanding - it requires two key elements: knowingly providing false information and doing so with the intent to mislead the insurer into paying a benefit or claim.

Under U.S. law, fraud is treated as both a civil and criminal offense. To prove fraud, it must be shown that the individual knew their statement was false and intended for the insurer to rely on it. Additionally, the false information must be "material", meaning it could reasonably influence the insurer's decision on a policy or claim.

"Insurance fraud refers to any duplicitous act performed with the intent to obtain an improper payment from an insurer." - Wex Definitions Team, Cornell Law School

Auto insurance fraud typically falls into two categories. Hard fraud involves creating a loss from scratch, such as staging an accident, setting a car on fire, or falsely reporting a theft. On the other hand, soft fraud, or "opportunistic fraud", occurs when someone exaggerates a legitimate claim or lies on an application to reduce premiums. While soft fraud often results in misdemeanor charges and fines, both types of fraud carry serious consequences.

The financial toll is enormous. Fraud costs U.S. consumers about $308.6 billion annually. Auto insurance alone accounts for at least $29 billion each year in losses due to "premium leakage" - which includes unreported drivers and underreported mileage. Shockingly, 14% of personal auto premiums are used to offset these fraudulent costs.

Understanding these distinctions is crucial before diving into the difference between fraud and unintentional errors. Fraud involves intent, while honest mistakes do not - a distinction explored further below. For more information on navigating the complexities of the claims process, see our car accident guides.

Examples of Fraudulent Insurance Claims

Fraud schemes can take many forms, but some are especially common. One of the most notorious is the staged accident, where criminals deliberately cause collisions to collect payouts for fake injuries or vehicle damage. For example, in a "Swoop and Squat" scheme, two cars box in a victim’s vehicle. The lead car brakes suddenly, forcing the victim to rear-end it. These staged crashes have risen by 18% year-over-year.

A bizarre case in January 2024 highlights the creativity of fraudsters. Four men in Los Angeles were arrested for defrauding insurers of $141,839 by claiming a bear had damaged three luxury vehicles, including a Rolls Royce Ghost. Investigators later discovered the "bear" was actually a person in a costume, which was recovered during a search of one suspect’s home.

Other fraudulent tactics include inflated repair costs and medical bills. Dishonest repair shops or medical providers sometimes collude with claimants to overcharge or bill for services that were never performed. For instance, some repair shops install counterfeit parts, like fake airbags, while charging insurers for original equipment manufacturer (OEM) parts. In 2022, auto theft-related fraud alone caused $7.4 billion in losses.

Rate evasion is another common scheme. Applicants lie about details like where their car is kept, how much they drive, or who the primary driver is to secure lower premiums. In 2017, false garaging claims - reporting an incorrect location for a vehicle - cost insurers $2.9 billion. Misrepresenting the primary driver accounted for 36% of premium leakage, while underestimating mileage contributed 19%.

Then there’s vehicle dumping, where someone falsely reports their car as stolen after abandoning, destroying, or hiding it - often to avoid paying off a loan. Other schemes include claiming old damage as part of a new accident or using "title washing" to hide a car’s history of flood damage or total loss by reselling it in states with looser title regulations.

What Is an Honest Mistake in Insurance Claims?

In contrast to fraudulent actions, an honest mistake in the insurance world refers to an unintentional error made during the application or claims process, without any intent to mislead the insurer. Fraud involves knowingly providing false information, but honest mistakes happen when someone unknowingly submits incorrect details. For instance, listing the wrong date for a past medical procedure is typically considered an innocent oversight rather than an attempt to deceive.

The defining factor here is intent. Fraud is rooted in deliberate falsehoods, while honest mistakes lack any intent to deceive. As Leppard Law explains:

"Intent plays a significant role in distinguishing between fraud and honest errors. The law typically requires proof of intent to deceive for a fraud conviction." - Leppard Law

For an honest mistake to be a valid defense, it must also be reasonable - meaning that someone in a similar situation could plausibly make the same error. Correcting such mistakes promptly demonstrates good faith. However, errors involving material facts - those that could affect the insurer's decision on coverage or premiums - carry more weight and scrutiny.

Common Types of Honest Mistakes

Here are some examples of honest mistakes policyholders might encounter:

- Clerical Errors: Simple typos or data entry mistakes, such as entering $3,500 instead of $3,050 for repair costs, can happen without malicious intent.

- Policy Misinterpretation: Insurance policies often contain complex or ambiguous terms, leading to genuine misunderstandings about what is covered.

- Stress-Induced Errors: The stress following an accident can cause memory lapses or inaccuracies when filling out paperwork or recalling details. Knowing what to do after an accident can help you stay organized and avoid these common pitfalls.

- Technical Issues: Errors can arise from unclear online instructions or software glitches during the submission process.

- Lack of Knowledge: A policyholder might not be aware of a specific issue with their car or property, unintentionally providing inaccurate information about its condition.

While these mistakes are unintentional, addressing them quickly and transparently is crucial to maintaining trust with your insurer.

How Fraud and Honest Mistakes Differ

The key difference between fraud and an honest mistake boils down to intent. As Spodek Law Group explains, "Fraud requires you 'knowingly' made a false statement. That's the legal standard". In simple terms, fraud is an intentional act of deception aimed at financial gain, whereas honest mistakes lack this deliberate intent.

Insurance investigators rely on error pattern analysis to tell the two apart. A single error on a claim form - like a typo or a momentary oversight - is usually seen as an innocent mistake. But when multiple similar errors appear across several claims or applications, it raises suspicion and can be used as evidence of fraudulent intent. Timing also matters. Correcting an error immediately - before any investigation begins - demonstrates good faith. On the other hand, waiting until you're caught to disclose an error can suggest an intent to deceive. These nuances are crucial for investigators as they dig deeper into claims.

Fraud typically involves hiding facts, staging events, or submitting falsified documents. Honest mistakes, in contrast, are marked by transparency. For instance, if you're unsure how to fill out a form and email your insurance agent for clarification, that communication creates a record of your efforts to act correctly - not deceptively.

Investigators also use the Fraud Triangle to assess claims. This framework examines three elements: pressure (like financial struggles), opportunity (such as system vulnerabilities), and rationalization (justifying dishonest actions). Combined with error pattern analysis, it helps differentiate between deliberate fraud and accidental errors. Understanding these distinctions is essential for policyholders to manage claims properly and avoid legal trouble. This includes knowing how insurance calculates total loss to ensure your settlement is fair and accurate.

Comparison Table: Fraud vs. Honest Mistakes

Here's a quick breakdown of the key differences:

| Feature | Insurance Fraud | Honest Mistake |

|---|---|---|

| Core Intent | Intentional deception for financial gain | Unintentional error or oversight |

| Frequency | Patterns of repeated errors | Isolated, one-time incidents |

| Correction | Errors hidden until discovered | Promptly corrected by the filer |

| Communication | Misleading or concealed information | Open inquiries and requests for help |

| Evidence | Falsified documents, staged events | Typos, clerical errors, or stress-related issues |

| Legal Status | Criminal offense (often a felony) | Civil issue with no criminal intent |

Legal and Financial Penalties for Auto Insurance Fraud

Auto insurance fraud comes with harsh legal and financial consequences. The first and most immediate concern is criminal charges. In California, for example, fraudulent claims under $950 are usually treated as misdemeanors, which can result in up to six months in county jail. Claims exceeding $950, however, are often prosecuted as felonies, carrying much steeper penalties.

Felony convictions can lead to prison sentences ranging from two to five years, with the possibility of up to 15 years in extreme cases [28,29,31].

The financial penalties are equally severe. Misdemeanor fines typically range from $500 to $10,000, while felony fines can climb as high as $50,000 - or even double the amount defrauded, whichever is greater [28,29]. For instance, in Michigan, offenders may face fines of up to $50,000 and up to four years of incarceration. Courts often require restitution, which means offenders must repay not only the fraudulent claim amount but also the insurer’s investigative and legal expenses [27,30]. Additionally, some states allow insurers to seek treble damages in civil court, forcing offenders to pay three times the defrauded amount [27,30].

A fraud conviction doesn’t just end with fines and jail time. It’s recorded in industry databases like CLUE and ISO ClaimSearch, making it almost impossible to find affordable insurance afterward [32,14]. For professionals in fields such as law, healthcare, or finance, the fallout can be even worse, potentially leading to the loss of professional licenses [27,29]. Insurers also have the right to rescind policies, retroactively voiding coverage as if the policy never existed. This is a stark contrast to how unintentional errors are handled.

The penalties hinge on intent, as fraud requires deliberate deception. Failure to pay restitution or civil judgments can result in liens, wage garnishments, or even asset freezes [27,32,30].

The California Department of Insurance sums it up clearly:

"Insurance fraud is a felony punishable by up to five years in state prison and a $50,000 fine".

Ultimately, the risks far outweigh any perceived benefits of committing fraud.

What Happens When You Make an Honest Mistake

When you make an honest mistake on an insurance claim, the situation is usually handled administratively rather than as a criminal issue. The key factor here is intent - insurers understand that people make errors, and these are generally resolved through corrections, not legal action. This process is entirely different from how fraud investigations are conducted.

If you realize you've made a mistake, take action quickly. Provide any missing documents and clarify the situation with your claims adjuster. If your claim gets denied due to the error, you can file an internal appeal. Along with your appeal, include corrected evidence like updated repair estimates, medical records, or receipts, and send everything via certified mail to ensure proper documentation.

Timing is crucial. Spodek Law Group explains:

"If you found the mistake yourself and fixed it immediately - before any investigation, before anyone asked questions - that's powerful evidence of innocent intent".

Resolving these errors typically involves reconciling documents and confirming policy details. Once everything is verified, your claim can be adjusted, potentially leading to a partial or full payout. Importantly, your policy stays active, and you won’t face criminal charges or end up flagged in fraud databases.

"Exaggerations by an insured, if offered as mere opinion or innocent overvaluation, constitute honest mistakes and do not contain the level of intent necessary to show insurance fraud".

Act quickly and transparently. If you discover an error after filing your claim, notify your insurer in writing and correct it immediately. Avoid deleting emails or documents, as this could be seen as an attempt to hide something, even if that wasn’t your intention.

Comparison Table: Consequences of Fraud vs. Honest Mistakes

Here’s a side-by-side look at how the outcomes differ, emphasizing why intent matters so much:

| Feature | Honest Mistake | Insurance Fraud |

|---|---|---|

| Legal Outcome | No criminal charges; resolved administratively | Felony or misdemeanor charges, fines, and jail time |

| Claim Status | Claim adjusted or corrected; partial/full payout possible | Claim rejected in full; recovery of past payments |

| Policy Impact | Policy remains active; possible premium adjustment | Policy cancellation or retroactive voidance |

| Future Coverage | Unaffected | Flagged in fraud databases, leading to higher premiums or denial of coverage |

| Professional Impact | No impact | Loss of professional licenses and employment |

How Insurance Companies Investigate Claims

Insurance companies use a mix of advanced technology, forensic techniques, and expert analysis to distinguish between honest claims and potential fraud. The process begins as soon as you file a claim, with adjusters on the lookout for any inconsistencies - though they understand that not every discrepancy points to fraud.

One key tool is pattern analysis, which relies on massive databases like ISO ClaimSearch. This system, containing over 1 billion historical claims, helps insurers spot suspicious trends. For example, multiple claims tied to the same address, individuals cashing checks from several companies, or unusually high claims compared to the reported damage can all raise red flags. Fraudulent claims are no small issue - industry estimates suggest they cost the U.S. about $40 billion annually, adding $400 to $700 to the average consumer’s insurance premiums. Once flagged, these claims are handed off to specialized investigation teams.

If a claim seems questionable, Special Investigation Units (SIUs) step in. These teams, often staffed with former law enforcement officers and medical experts, conduct in-depth reviews. They rely heavily on digital forensics, analyzing data from Event Data Recorders (EDRs) and GPS systems. Forensic specialists Shady Attalla and Liam Rodgers highlight how this works:

"If the damage is consistent with a relatively severe collision, and no event is recovered [from the EDR], this would indicate that the vehicle was most likely off at the time of the collision, and the reported sequence of events is likely untruthful".

Physical evidence analysis adds another layer of scrutiny. Investigators examine paint transfers to determine if a car hit another vehicle or a stationary object, like a pole. They also study dent patterns, tire marks, and the height of damage to verify whether the accident details align with the physical evidence. Meanwhile, social media monitoring has become a standard tool. Public posts can sometimes reveal contradictions - like a claimant alleging total disability while sharing gym workout videos.

Alongside these technical methods, interviews and recorded statements play a crucial role. Adjusters compare your account of events with findings from digital data and surveillance. The National Insurance Crime Bureau provides investigators with a list of 23 "suspicious loss indicators" to help identify potential fraud. That said, investigators are careful not to jump to conclusions. They understand that nervousness or small discrepancies in your story don’t necessarily mean fraud - they focus on the "totality of the circumstances" to determine whether a claim involves intentional misrepresentation or an honest mistake.

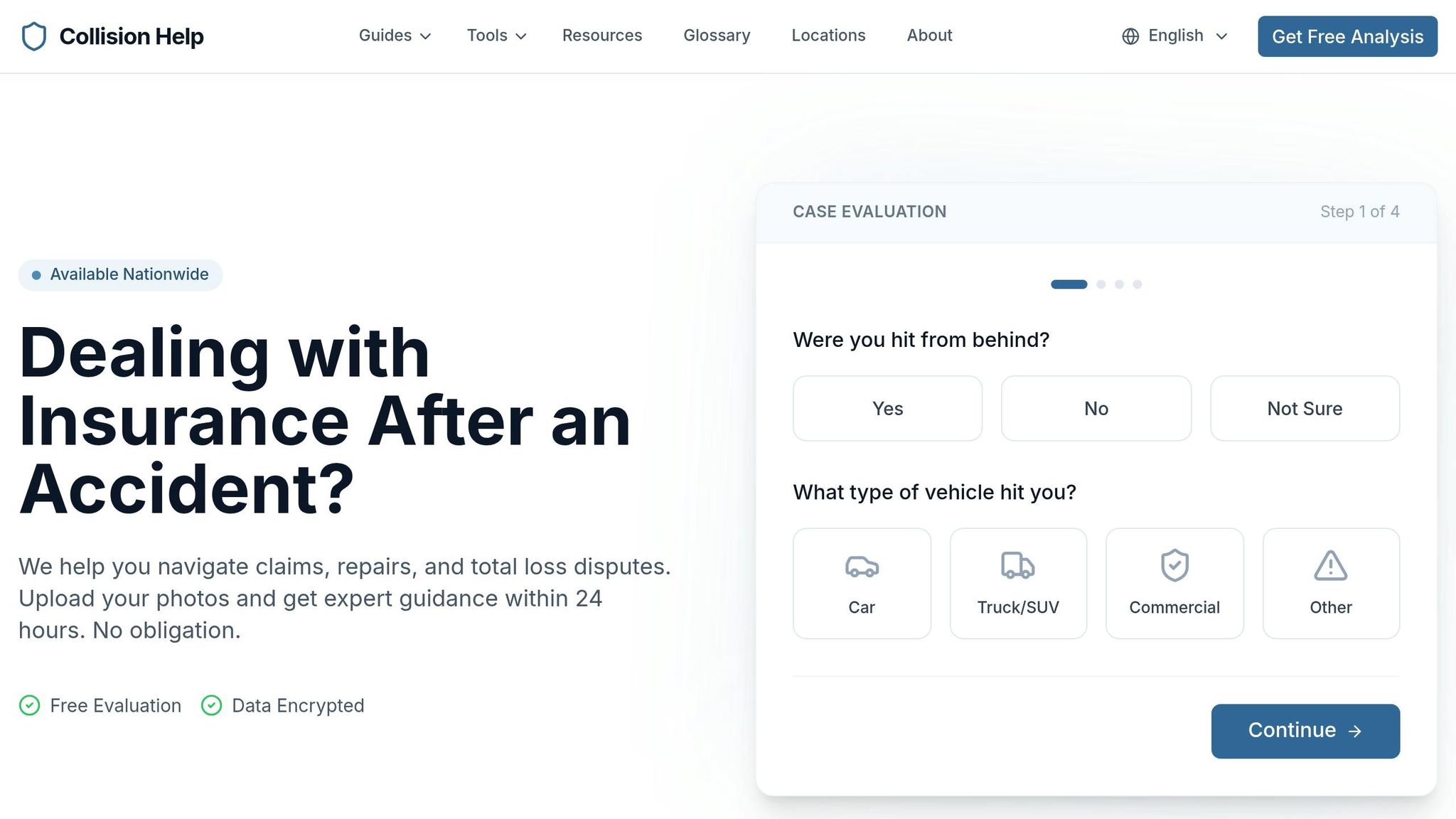

Getting Help with Honest Claims Through Collision Help

If you've made an honest mistake on your insurance claim, getting help quickly can make all the difference. Collision Help | Nationwide Accident Help offers a simple and effective way to address errors before they escalate into disputes or penalties. This service emphasizes the importance of intent and taking immediate action.

The process is designed to be fast and straightforward. You can upload photos of the damage through a secure system and receive an expert review within 24 hours. This quick documentation can help identify and correct errors early, reducing the risk of suspicion or potential legal issues.

Expert guidance can also help you avoid common pitfalls, like misinterpreting your policy or failing to dispute a total loss valuation - a mistake that could lead to fraud allegations. By ensuring your actions align with industry standards, this support reinforces your defense if your intent is ever questioned. Considering that federal prosecutors secure convictions in over 90% of cases, keeping your claim from reaching that stage is crucial.

Acting quickly is key. Correcting errors promptly and documenting every step shows clear evidence that any inaccuracies were unintentional. A strong paper trail of your efforts to clarify and resolve issues can further demonstrate your honest intent.

For claims under $50,000, there's even a chance that prosecutors may accept restitution and a civil settlement instead of pursuing criminal charges. With expert help, you can keep your claim administrative and avoid more serious legal consequences.

Conclusion

The line between auto insurance fraud and honest mistakes lies in intent. Fraud involves a deliberate effort to deceive an insurer for financial gain, while honest mistakes stem from unintentional errors - like typos, misinterpreting policy terms, or simple oversights. Legally, this difference matters. Prosecutors must prove "specific intent to defraud" to secure a conviction, highlighting the importance of intent in these cases.

Honesty and promptness can make all the difference. Reporting errors as soon as possible shows good faith and can prevent misunderstandings from escalating. Keeping a detailed record of your communications - emails, notes, and questions - can further demonstrate your integrity if any issues arise.

With over 90% of fraud cases leading to convictions, it’s essential to protect yourself from any suspicion of wrongdoing. Correcting errors immediately can help you avoid serious legal consequences.

If you're unsure how to navigate the claims process, services like Collision Help | Nationwide Accident Help provide expert support. Their secure photo upload system and 24-hour expert review ensure your claim is documented accurately, helping you avoid mistakes that could lead to fraud allegations. Professional guidance keeps your claim clear, honest, and moving forward smoothly.

FAQs

What should I do if I realize I filed something wrong on my claim?

If you spot an error in your claim, reach out to your insurance company or claims adjuster as soon as possible. Clearly explain the mistake and back it up with any relevant evidence to show it was unintentional. Taking the time to review your claim thoroughly and addressing the issue openly can help resolve it faster and prevent any legal or financial complications down the line.

Can an honest mistake still get my claim denied or delayed?

Yes, making an honest mistake can lead to delays or even denials of an insurance claim, even if there was no malicious intent. That said, mistakes are not the same as fraud, which involves deliberate misrepresentation. Insurers usually consider the context and intent behind the error before deciding on the next steps.

What kind of proof helps show my mistake wasn’t fraud?

To prove that your mistake wasn’t intentional, you’ll need to provide evidence showing it was an honest error. This might include detailed explanations of any misunderstandings, examples of mistakes made under pressure, or witness statements verifying that you had no plans to mislead anyone. The key is to highlight that the misrepresentation occurred unintentionally, not as a deliberate act.