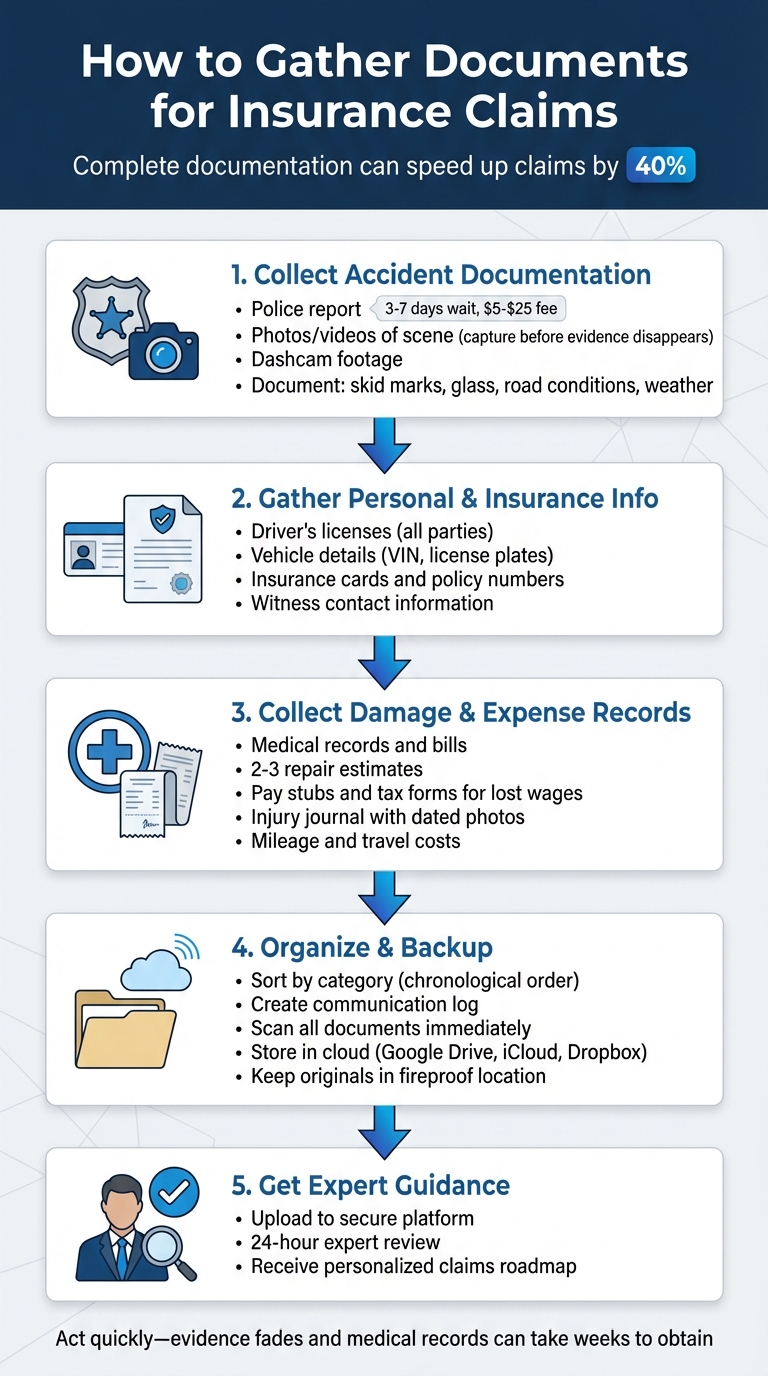

How to Gather Documents for Claims

When filing an insurance claim, having the right car accident guides and resources is critical. Complete and accurate records can speed up the process by 40% and ensure you get the compensation you deserve. Here’s what you need to know:

- Accident Documentation: Get a police report, take photos/videos at the scene, and secure dashcam footage.

- Personal and Insurance Info: Collect licenses, vehicle details, and insurance policies from all parties involved.

- Damage and Expense Records: Keep medical bills, repair estimates, and proof of lost wages (pay stubs, tax forms, etc.).

- Organize and Backup: Sort documents into categories, digitize them, and save backups in the cloud.

Act quickly - evidence like skid marks and medical records can fade or take weeks to obtain. Organized documentation ensures a smoother claims process and helps avoid delays or denials.

5-Step Document Gathering Process for Insurance Claims

First steps before filing an insurance claim

sbb-itb-6a9d141

Step 1: Collect Accident and Incident Documentation

Start by gathering all relevant documents from the accident scene and official sources. Acting quickly ensures you capture evidence before it disappears.

Get a Copy of the Police Report

First, determine which agency responded to the accident - this could be local police, the county sheriff, or the state highway patrol. At the scene, ask the officer for the incident or case number, along with their name and badge number. This information makes it easier to request the report later.

Typically, police reports are available within 3 to 7 days, though some areas, like Maricopa County, Arizona, may take up to 14 days. You can request the report through the agency's online portal, by mail, or in person at their records department. Be prepared to provide the crash date, time, location, and the names and license numbers of the drivers involved. Fees for reports generally range from $5 to $25, depending on the jurisdiction.

"A police report can go a long way toward gaining negotiation leverage in any personal injury dispute." - Ty McDuffey, J.D., FindLaw

Once you receive the report, review it carefully for errors, such as incorrect names, dates, or details of the incident. If you spot any inaccuracies, contact the department to request a correction or to submit a supplemental statement. Keep multiple copies for your records and share them with your insurance company.

Take Photos and Videos at the Accident Scene

If it’s safe to do so, take photos of the scene before any vehicles are moved. Capturing their exact positions at the time of impact is crucial. Physical evidence, like skid marks, shattered glass, or fluid trails, can disappear quickly, so act promptly.

Take a mix of wide-angle shots to show the entire area, including traffic signals and landmarks, and close-ups to highlight vehicle damage. Be sure to photograph license plates and the VIN on the driver-side windshield. Document other important details, such as road conditions, traffic signs, and weather.

"Photographs taken at the car accident scene are powerful evidence that will help you get maximum compensation." - Charles R. Gueli, Esq., Licensed Attorney

Avoid editing your photos or applying filters. Save the original files and back them up using cloud storage or email to preserve metadata like timestamps and location information. If you have a dashcam, secure the footage immediately to prevent it from being overwritten. You can also record video while walking around the scene, narrating key observations. Audio can capture critical details, such as admissions of fault or the tone of conversations.

Once you've documented the scene thoroughly, the next step is to gather personal and insurance information.

Step 2: Gather Personal and Insurance Information

Once you've documented the scene, the next step is to collect personal and insurance details from everyone involved. These details are critical for filing your claim, and any mistakes or missing information could delay the process or complicate a total loss dispute later on. By combining this information with the evidence from the scene, you'll have a complete record to support your claim.

Driver and Vehicle Information

Always request to see each driver's license - don’t rely on verbal information. As Mary Bonelli, Senior Vice President of Public Information at the Ohio Insurance Institute, cautions:

There are situations where people make up information

This is especially common when someone doesn’t have insurance. To avoid issues, take clear, close-up photos of each license, capturing essential details like the full name, license number, issuing state, phone number, and home address.

For vehicle details, record the year, make, model, color, license plate number, and the 17-digit VIN (visible at the base of the driver-side windshield or inside the door frame). If the driver isn’t the vehicle’s owner, make sure to get the owner’s name and contact information. Additionally, if there are witnesses - whether passengers, pedestrians, or bystanders - collect their names, phone numbers, and addresses.

Insurance Policy Details

Verify each driver’s insurance coverage by asking for their insurance card, whether physical or digital. Note the insurance company name, policy number, and expiration date. William Brower, Assistant Vice President for Claims at Liberty Mutual Insurance, emphasizes the importance of capturing this information at the scene:

The information that your insurer will need to investigate your claim is normally available at the accident scene. However, it can be very time consuming to collect this information, if the details aren't captured at the accident scene

.

For your own policy, locate your declarations page, which outlines your coverage limits, deductibles, and effective dates. Confirm your policy number, the named insureds, and any additional coverages, such as personal injury protection (PIP), rental car reimbursement, or uninsured/underinsured motorist coverage. Keep proof of premium payments handy to confirm your policy was active at the time of the accident.

Step 3: Collect Records of Damages and Expenses

At this stage, your priority should be documenting every financial loss stemming from the accident. This includes medical bills, property damage, and lost income. Without detailed records, you risk losing out on compensation - insurers won’t cover what you can’t prove.

Medical Records and Bills

Medical documentation forms the foundation of your claim. As Vadim Sigal, Attorney at Sigal Law Firm, emphasizes:

Official medical records are one of the most important pieces of documentation in a personal injury claim.

Gather all medical records, from emergency room visits to hospital stays, diagnostic tests, and doctors' notes. Save receipts for medications, medical equipment (like crutches or wheelchairs), and related expenses. If you required in-home care, skilled nursing, or household assistance, document those costs as well. Don’t overlook smaller expenses like mileage, parking fees, or travel costs for medical appointments.

Even if you feel fine after the accident, seek medical attention immediately. This helps establish a clear link between the accident and your injuries. Keep an injury journal to log daily pain levels, symptoms (e.g., headaches or dizziness), and how your injuries affect your daily life. Take dated photos of visible injuries - such as bruises, swelling, or stitches - right after the accident and throughout your recovery. Be thorough when describing your symptoms to doctors because insurers may deny compensation for undocumented complaints. As Simmons and Fletcher, P.C. explains:

Juries do not tend to reward people who 'tough it out.' They tend to think that someone who is seriously injured will seek care without concern for cost or inconvenience.

Once your medical documentation is in order, shift focus to property damage evidence.

Repair Estimates and Property Damage Evidence

When it comes to property damage, photos are your best ally. Take multiple photos of the damage from different angles to capture both context and detail. For damaged appliances or belongings, include serial numbers and model information. Also, document surrounding conditions - skid marks, broken glass, road conditions, weather, and traffic signals.

To strengthen your case, get two or three independent repair estimates. Keep in mind that initial estimates may change if hidden damage is discovered during a detailed inspection. This is handled through a supplement process. If your property or vehicle is declared a total loss, provide receipts or photos showing its condition before the accident to support a fair valuation. Avoid discarding damaged items until an adjuster has inspected them - unless they pose a safety hazard. Keep all repair quotes and related invoices as part of your financial records.

Proof of Employment and Lost Wages

Proving lost income requires accurate documentation. Gather pay stubs, tax forms, and bank statements to verify your earnings. Request a letter from your employer confirming the dates you missed work due to your injuries. Additionally, obtain a note from your doctor stating that your injuries prevented you from performing your job duties.

If you’re self-employed, collect tax returns, Form 1099s, profit and loss statements, and records of canceled contracts or missed opportunities. Don’t forget to include proof of lost benefits, such as employer retirement contributions, transportation stipends, or accrued sick leave and vacation time (PTO). As Terms.Law points out:

What separates a strong claim from a weak one is not flowery language or legal threats - it is organized, credible, and complete documentation.

Even if PTO was used to cover your absence, track it - these are earned benefits you’ve lost. Document cash tips and irregular payments as well. You might also be eligible for compensation if you missed job interviews, promotions, or professional development opportunities that could have led to a raise.

Step 4: Organize Documents for Submission

Keeping your records organized is essential once you've gathered all the necessary paperwork. A well-organized system not only saves time and reduces frustration but also helps your claim move along more smoothly. The trick is to group related documents and maintain both physical and digital copies.

Create a Filing System

Start by sorting your documents into categories like correspondence, medical bills, repair estimates, witness accounts, and employment records. Within each category, arrange the paperwork in chronological order (oldest to newest) to create a clear timeline for the insurance adjuster.

For physical storage, use a file box with labeled folders or a three-ring binder with tabbed dividers and pocket pages. At the front of your file, keep a communication log to document every interaction with your insurer. Include details like the date, time, the name of the person you spoke with, and a brief summary of the conversation. When you receive physical mail, record the date it arrived - delivery delays can sometimes impact response deadlines. Understanding how long an insurance claim takes can help you manage these deadlines effectively. Always retain personal copies of everything you submit to the insurer to avoid complications if something gets lost.

Digitize and Back Up Your Files

Digital backups are a lifesaver when it comes to protecting your records from being misplaced, damaged, or destroyed. As Insurance Panda suggests:

"The safest approach is to store originals digitally and keep at least two backups (for example: one on your phone/computer and one in the cloud)."

Scan or photograph every document as soon as you receive it, especially receipts printed on thermal paper, as they can fade quickly. Avoid editing or applying filters to original digital photos so that timestamps and metadata stay intact; this information is often crucial for proving when and where damage occurred. Save these files to secure cloud platforms like Google Drive, iCloud, or Dropbox, and keep a secondary backup on your computer or phone.

To make your digital files easy to locate, label them by category (e.g., "Medical_Bills" or "Repair_Estimates") and follow a consistent naming format like "YYYY-MM-DD_DocumentType_Provider." Many insurance companies now offer mobile apps where you can upload photos and documents directly to your claim file. Even after digitizing, it's wise to store original physical documents in a fireproof and secure location, as insurers may request them for verification.

With your documents neatly organized and backed up, you're ready to move on to the next step in the filing process, which involves using Collision Help for expert guidance with your claim.

Step 5: Use Collision Help for Expert Guidance

Once your files are neatly organized and backed up, the next step is seeking expert advice. This is where Collision Help comes in. Their team offers tailored guidance to ensure your claim process runs smoothly and efficiently. By reviewing your documentation and providing personalized advice, they help you build on your organized files to simplify and strengthen your claim submission.

Upload Photos and Documents Securely

Collision Help provides a secure online platform for uploading your accident-related photos and documents. Make sure to take clear, well-lit photos of your vehicle damage, the accident scene, and any relevant paperwork - like repair estimates or medical bills. Their experts review your submissions within 24 hours to ensure that everything is complete and accurate. This quick review process helps catch any missing items early, avoiding unnecessary delays. Plus, their secure system keeps your sensitive information safe while giving you easy access to your files if you need to add more documents later.

Get a Personalized Claims Roadmap

With your documentation in place, Collision Help offers a customized claims roadmap tailored to your situation. This includes advice on submitting your claim and handling potential disputes over total loss valuations. They take into account factors like the extent of the damage and your specific insurance policy. As Gigi Walker, President of Walker's Autobody and Fleet Repair, puts it:

"Documentation and photographs are very important. Sometimes adjusters fundamentally don't understand how difficult some of these repairs are."

Conclusion

Well-organized documents can make all the difference when it comes to speeding up claims and avoiding unnecessary delays. Keeping thorough records doesn’t just help streamline the settlement process - it also protects your legal rights if disputes arise. A solid paper trail, including photos, receipts, and communication logs, helps establish fault, accurately calculate damages, and prevents insurers from downplaying your recovery.

Expert guidance takes this process to the next level. With tools like Collision Help, you can access professional reviews and receive a personalized roadmap for your claim, ensuring everything is submitted correctly and securely.

Start compiling and digitizing your documents as soon as possible to secure the compensation you’re entitled to under your policy. Each piece of evidence you collect strengthens your case for a fair and timely settlement. With proper preparation and the right support, achieving a full and fair claim is well within your grasp.

FAQs

What if I can’t get the police report yet?

If the police report isn’t immediately accessible, don’t wait to start gathering other evidence to back up your claim. Snap photos or record videos of the scene, making sure to capture any visible damage and key details. Jot down important observations and, if possible, collect contact information from witnesses who can support your account. While a police report can be useful, insurance companies often consider other forms of evidence. Once the report becomes available, make sure to follow up and obtain a copy for your records.

What documents do I need to prove lost wages?

To demonstrate lost wages, you'll need to collect documentation that confirms both your income and the time you missed work due to your injury. Key records include payroll or timekeeping logs, a wage verification letter from your HR department or supervisor, medical notes that outline work restrictions, and pay-related tax forms or bank statements. If your earnings fluctuate, additional documents like tax returns, invoices, or a detailed earnings history may help establish your average income more effectively.

How long should I keep claim documents?

When it comes to keeping claim documents, the general rule of thumb is to hold onto them for 3 to 7 years, depending on the type of claim and any relevant statutes of limitations. For policies like auto, homeowners, or umbrella insurance, it's a good idea to keep records for at least 3 years after the policy ends. However, if the claim involves injuries, disputes, or ongoing litigation, it's safer to retain those documents for 7 years or more to ensure you're covered for any legal requirements.