How to Counter a Lowball Settlement Offer

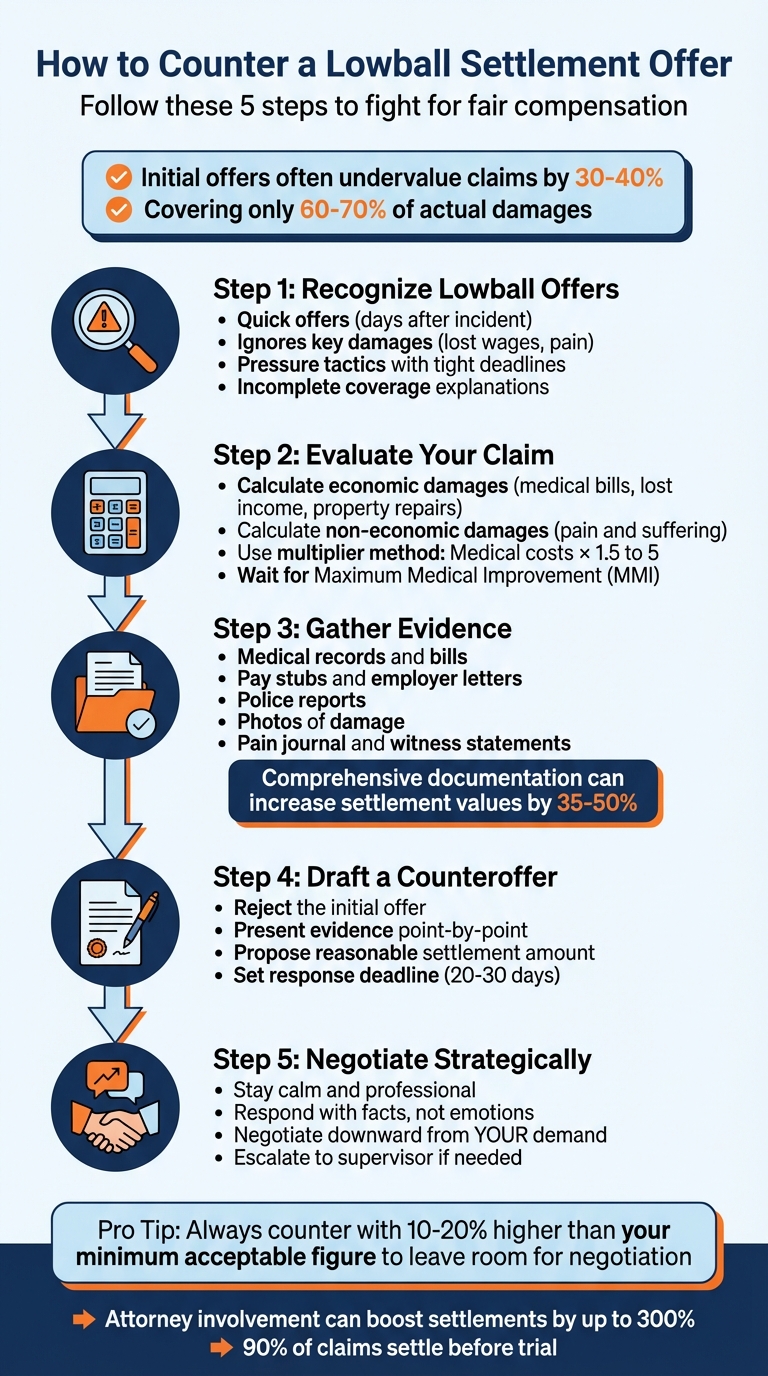

When an insurance company offers a settlement that undervalues your claim, it’s called a lowball offer. This tactic is common, as insurers aim to save money and test if you’ll accept less than you deserve. To counter effectively, follow these steps:

- Recognize Lowball Offers: Offers made quickly after an incident or those that ignore key damages (like lost wages or pain) are often lowball attempts.

- Evaluate Your Claim: Calculate both economic damages (medical bills, lost income, property repairs) and non-economic damages (pain and suffering). Use the multiplier method to estimate fair compensation.

- Gather Evidence: Collect medical records, pay stubs, police reports, and photos to document your losses.

- Draft a Counteroffer: Write a professional letter rejecting the offer, presenting evidence, and proposing a reasonable settlement amount.

- Negotiate Strategically: Stay calm, respond to adjusters’ points with facts, and escalate if necessary.

Waiting until you’ve fully assessed your damages (Maximum Medical Improvement) is crucial, as settlements are final. If negotiations stall, consider involving an expert or attorney to strengthen your position.

Key Tip: Always counter with a higher amount than your minimum acceptable figure, leaving room for negotiation.

5 Steps to Counter a Lowball Insurance Settlement Offer

Injury Lawyer EXPLAINS: How to Counter a Lowball Settlement Offer & Get What You Deserve

sbb-itb-6a9d141

How to Identify and Evaluate a Lowball Offer

Building a solid evaluation is key when responding to an unfair settlement offer. Insurance adjusters often count on claimants being unaware of their claim's true value. By recognizing warning signs and accurately calculating your damages, you can confidently challenge lowball offers.

Warning Signs of a Lowball Offer

There are several clues that an offer might be unreasonably low. Timing is one of the biggest indicators. If an offer arrives just days after the incident - before you've completed medical treatment or fully assessed your injuries - it’s likely an attempt to settle for less than the claim is worth. Data shows that initial offers from adjusters often undervalue claims by 30–40%, covering only 60–70% of actual damages.

Keep an eye out for pressure tactics. Adjusters may set tight deadlines to push you into accepting before seeking legal advice. Another red flag is incomplete coverage - offers that only account for medical bills while ignoring lost wages, property damage, or pain and suffering. If the adjuster refuses to explain how they calculated the offer or dismisses your medical records without review, labeling your injuries as "minor", it’s a strong sign the offer is undervalued.

Spotting these signs early is essential before you start calculating the true worth of your claim.

Calculating What Your Claim Is Actually Worth

A fair claim includes both economic losses (special damages) and non-economic losses (general damages).

- Special damages cover tangible costs like medical bills (past and future), lost wages, reduced earning potential, property repairs, and expenses for tasks you can no longer perform.

- General damages address subjective losses such as physical pain, emotional distress, disability, or disfigurement.

To estimate a fair settlement, many use the multiplier method. This involves multiplying your total medical costs by a number between 1.5 and 5 to account for pain and suffering. Moderate injuries typically use a multiplier of 2 or 3, while severe or permanent injuries warrant a multiplier of 5 or higher. For example, if your medical bills total $10,000 and you use a multiplier of 3, your non-economic damages would be $30,000, bringing the total claim to $40,000.

It's crucial not to settle until you've reached Maximum Medical Improvement (MMI). Settling too early could prevent you from seeking additional compensation if your condition worsens.

Gathering Documentation of Your Losses

Strong documentation is your best tool in negotiations. Collect detailed records to support every aspect of your claim:

- Medical Records: Include hospital bills, therapy notes, diagnostic reports, and pharmacy receipts. Using precise medical terms like "herniation superimposed on a disc bulge" can highlight the seriousness of your injuries.

- Lost Wages: Obtain pay stubs and an official letter from your employer confirming missed work and lost income.

- Police Reports: These establish fault and document any citations issued at the scene.

- Photos and Receipts: Take clear pictures of vehicle damage and the accident scene as soon as possible. Keep receipts for out-of-pocket costs like childcare, transportation for medical visits, or home modifications.

- Pain and Suffering Evidence: Maintain a daily journal describing your struggles and gather statements from family, friends, or coworkers about how the accident has impacted your life.

Did you know? Comprehensive medical documentation alone can increase settlement values by 35–50%.

| Documentation Category | What to Collect | Why It Matters |

|---|---|---|

| Medical | Records, bills, MRI/X-ray reports, specialist notes | Proves the severity and cause of injuries |

| Financial | Pay stubs, HR letters, tax returns | Verifies lost wages and reduced earning capacity |

| Property | Repair estimates, photos, negotiate a total loss settlement | Details vehicle and property damage |

| Liability | Police reports, witness statements, dashcam footage | Establishes the other party's fault |

| Daily Impact | Pain journals, testimony from loved ones | Supports claims for pain and suffering |

A well-documented claim lays the groundwork for a strong counteroffer. If your vehicle is declared a total loss, you may need to dispute the insurance company's valuation to ensure you receive fair market value.

Writing a Strong Counteroffer

Once you've gathered all the necessary evidence using car accident guides and determined the actual value of your claim, the next step is to draft a formal counteroffer. This letter should not only reject the low offer but also present a well-supported, evidence-based settlement amount.

What to Include in Your Counteroffer Letter

A strong counteroffer letter needs to cover six key elements:

- Claim Identification: Clearly list your claim number, the accident date, and the parties involved.

- Rejection Statement: Firmly state that the initial offer is unacceptable.

- Point-by-Point Rebuttal: Address each reason the adjuster gave for the low offer. Whether they question the severity of your injuries, claim shared fault, or dispute your treatment, use your documentation to refute these points systematically.

- Detailed Justification of Damages: Offer a thorough breakdown of your losses. This includes medical costs, lost wages, property damage, and non-economic damages like pain and suffering.

- New Settlement Figure: Propose a counteroffer amount that falls between your initial demand and the adjuster's offer.

- Response Deadline: Set a clear deadline - usually 20 to 30 days - for the adjuster to respond, encouraging timely progress.

For a quick summary, here's a helpful table:

| Component | Purpose |

|---|---|

| Claim Identification | Lists your claim number, accident date, and involved parties |

| Rejection Statement | Declares the initial offer unacceptable |

| Evidence Summary | Highlights key facts from police reports or medical records |

| Impact Statement | Explains how the injury has affected your daily life |

| The "Ask" | States your new settlement amount |

| Response Deadline | Sets a timeframe for the adjuster's reply |

Keep your tone professional and stick to facts. Avoid emotional language or personal remarks about the adjuster. If the offer was made over the phone, request it in writing along with their reasoning. This ensures you can address every point accurately.

Tip: Always negotiate downward from your original demand, not upward from the adjuster's low offer.

Supporting Your Counteroffer with Evidence

The strength of your counteroffer lies in the evidence you provide. Attach the documentation you've gathered to back up your claims. This transforms your letter from a simple opinion to a persuasive argument.

Use specific medical terminology when describing injuries - for instance, say "distal fibula fracture" instead of just "broken ankle." If the adjuster disputes your injuries or raises issues about preexisting conditions, include medical records that clearly link your treatment to the accident. Present your medical expenses in a clear chart, listing service dates, providers, charges, and amounts paid or owed.

To ensure your counteroffer is taken seriously, send it via certified mail with tracking. This creates a verifiable record of your communication.

Determining a Fair Counteroffer Amount

The final step is to calculate a counteroffer amount that accurately reflects your damages. Start by adding up all economic damages, such as medical bills, property damage, and lost wages (both past and future). Then, use the multiplier method to estimate your non-economic damages.

If you share some fault for the accident, adjust your total accordingly. For example, if you're 20% at fault on a $50,000 claim, reduce your claim to $40,000. Set your counteroffer slightly higher - 10% to 20% above your minimum acceptable amount - to leave room for negotiation.

Also, consider external factors like the at-fault party's insurance limits and settlement amounts for similar cases in your area. Remember, most car accident claims are resolved out of court, so both sides usually prefer to settle efficiently.

If the adjuster claims your demand exceeds their authority, don't be discouraged. This is often a negotiation tactic. Supervisors may have the authority to approve higher amounts if your evidence is strong. Stay patient, rely on your documentation, and negotiate steadily downward from your original demand. This approach helps you maintain both flexibility and firmness in achieving fair compensation.

Negotiating and Escalating Your Claim

Once you’ve prepared a solid counteroffer, the next step is negotiating effectively and knowing when it’s time to escalate.

How to Negotiate Effectively

Approach negotiations like a transaction - stay calm and objective. Successful negotiators understand that compromise is part of the process: both sides need to give a little to reach an agreement. Start with a higher figure to leave room for adjustments, but make concessions gradually. This shows you’re open to compromise without undermining the value of your claim.

Be aware of tactics adjusters might use to push for a lower settlement. For example, they may claim they’ve hit their "settlement authority" limit. In reality, supervisors often have the power to approve higher amounts if your evidence is strong. If the adjuster won’t budge, politely ask to speak with their manager, who has greater authority.

"Adjusters often cite their limited authority as a negotiation tactic. The adjuster's pay and bonuses depend on how much money they save for the company, so they'll pull out all the stops to get you to settle for less." - Charles R. Gueli, Esq.

Keep a detailed record of all communications. A paper trail is essential. In your counteroffer, set a clear response deadline - 10 to 14 business days is standard - to prevent unnecessary delays. If you don’t hear back by the deadline, follow up with another letter and consider escalating to a supervisor within a week or two.

If negotiations stall despite these steps, it’s time to consider escalating your claim.

When to Escalate Your Claim

If the adjuster doesn’t respond within your specified timeframe or insists on an unreasonably low offer, it’s time to escalate.

Watch for bad faith behaviors, such as "take-it-or-leave-it" ultimatums, ignoring clear evidence of your injuries, or showing bias against your claim. Document these instances carefully, as they can support your escalation or even a complaint with your state’s Department of Insurance.

In cases involving liability disputes - where the insurer wrongly claims you’re at fault despite strong evidence like police reports and witness accounts - or severe injuries like permanent disability or brain damage, it’s best to involve an attorney. These situations are often too complex to resolve on your own.

Be mindful of your state’s statute of limitations, which typically gives you two to three years from the accident date to file a lawsuit. Insurers may intentionally drag out negotiations, hoping you’ll run out of time and lose leverage. However, most claims - around 90% - settle before reaching trial. Insurers usually prefer to avoid court, so escalating to a supervisor or involving legal counsel often pushes them to reconsider their position.

Creating a Comparison Table to Show Undervaluation

A comparison table can be a powerful way to highlight how the insurer’s offer falls short. Use your documented losses to create a clear, side-by-side breakdown.

Include columns for the damage category, your documented amount, the insurer’s offer, and the difference. Cover all areas - medical expenses, lost wages (including overtime and bonuses), property damage, and non-economic damages like pain and suffering. Attach supporting documents for each item, such as medical bills, pay stubs, repair estimates, and doctor’s notes explaining your injuries.

Here’s an example:

| Damage Category | Your Documented Amount | Insurer's Offer | Difference |

|---|---|---|---|

| Medical Expenses | $18,500 | $12,000 | -$6,500 |

| Lost Wages | $7,200 | $4,000 | -$3,200 |

| Property Damage | $8,300 | $6,500 | -$1,800 |

| Pain and Suffering | $46,250 (2.5× multiplier) | $15,000 | -$31,250 |

| Total | $80,250 | $37,500 | -$42,750 |

Include this table in your counteroffer letter and use it during discussions to keep the focus on hard numbers rather than subjective opinions.

If the adjuster questions your pain and suffering multiplier, point out that industry standards typically range from 1.5 to 5 times the total medical costs, depending on the injury’s severity. Back up your chosen multiplier with detailed evidence of how the injury has impacted your life - missed family events, inability to work, ongoing pain, and other personal challenges. This documentation strengthens your case and justifies your calculations.

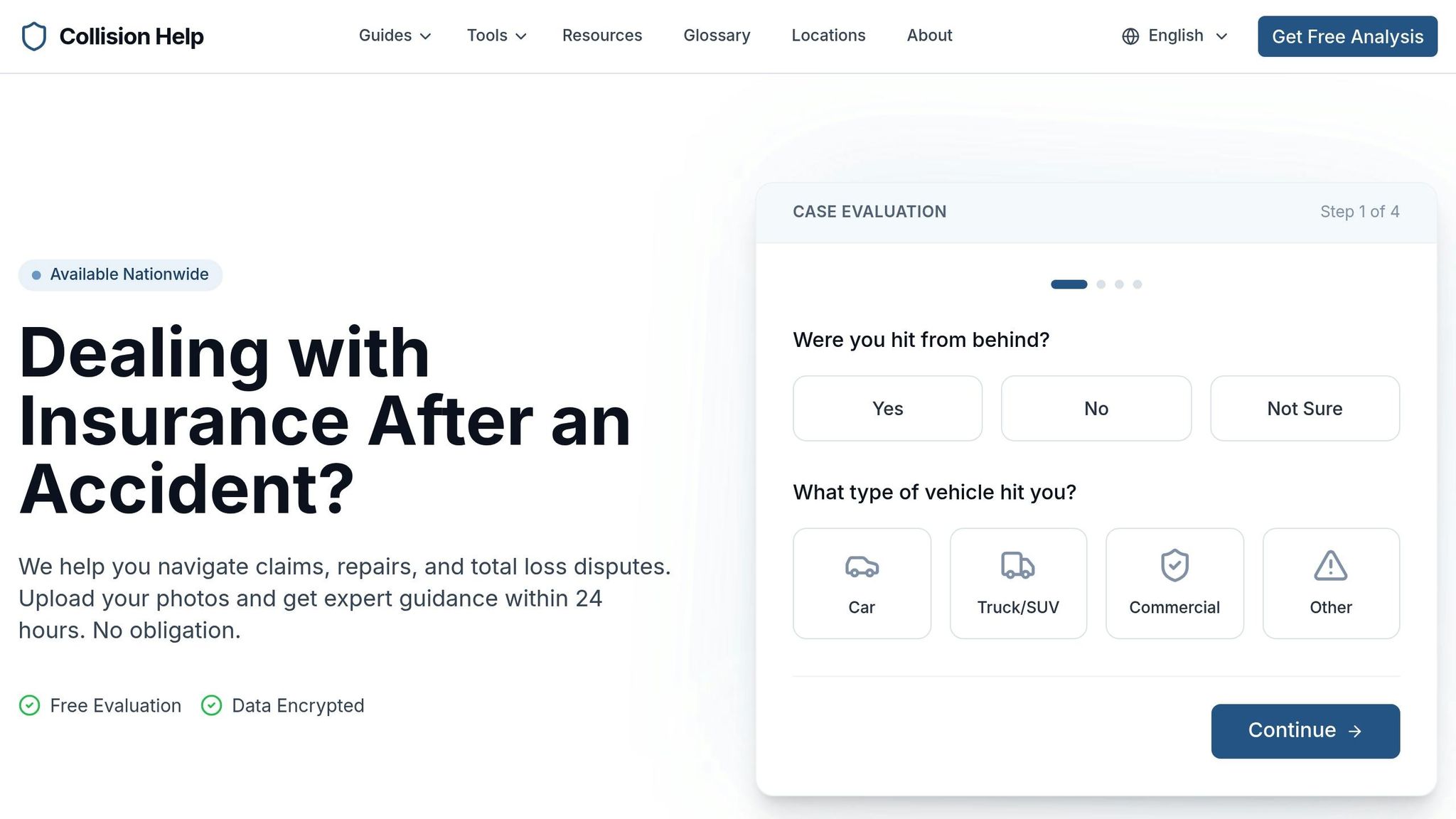

Getting Expert Help from Collision Help

When traditional negotiations hit a wall, expert assistance can completely shift the dynamics in your favor. Collision Help strengthens your claim by meticulously evaluating your damages. Through their secure platform, you can upload photos of your vehicle damage along with essential documents like police reports, medical records, and repair estimates. You can also include details regarding rental car coverage if your vehicle is unusable. Within just 24 hours, you’ll receive expert insights into your claim's true value.

How Collision Help Strengthens Your Claim

Collision Help determines the correct pain and suffering multiplier tailored to your situation. Insurers often default to the lowest multiplier - 1.5 times medical costs - but this service ensures a more accurate calculation based on your circumstances. With this evaluation, you’ll be better equipped to prepare a strong counteroffer and navigate negotiations effectively.

The platform also helps you tackle common tactics used by adjusters. For instance, if the insurance company tries to claim partial fault, dismiss necessary medical treatments as excessive, or cite authority limits, Collision Help provides strategies to challenge these arguments point by point in your counteroffer.

Why Expert Guidance Matters

Involving an attorney in a claim can boost settlement amounts by as much as 300%. Even if you don’t hire a lawyer, professional guidance ensures your losses are validated with expert analysis, leveling the playing field against the insurer.

This support also helps you avoid critical missteps. For example, it keeps you focused on the facts and prevents you from settling before reaching maximum medical improvement - a decision that’s irreversible once the settlement is signed. Incorporating expert advice into your claim strategy is a straightforward way to protect your interests and maximize your outcome.

How to Get Started with Collision Help

To begin, visit the Collision Help website and upload photos of your vehicle damage along with supporting documents. They offer a free initial evaluation with no upfront costs, and if legal representation becomes necessary, services are available on a contingency basis.

Within 24 hours, you’ll receive a personalized plan tailored to your situation. This roadmap factors in liability, policy limits, and other specifics, providing a clear guide to creating an evidence-backed counteroffer. It also includes advice for drafting a formal response that addresses every point raised by the adjuster.

Conclusion

Dealing with a lowball settlement offer takes preparation, evidence, and persistence. Stay calm and professional - insurance companies often start with low offers to test if you'll accept less than you deserve. Carefully review the adjuster's reasoning, gather detailed documentation of your losses, and respond with a well-supported counteroffer that addresses their points. This process - negotiating downward from your initial demand - helps prevent further undervaluation of your claim.

As attorney Dan Ray from the University of Missouri–Kansas City School of Law explains:

The insurance company's starting offer will be low. It might be insultingly low. Your first impulse might be anger... Take a deep breath and plan your next steps with a cool head.

A calm and strategic response, backed by evidence like itemized medical bills, proof of lost wages, and witness statements, strengthens your negotiating position and helps you push back against unfair offers.

Timing is also key. Wait until you've reached maximum medical improvement before settling, as agreements are final once signed. If negotiations reach a standstill or you encounter aggressive tactics, seeking expert assistance can make a big difference. For instance, Collision Help | Nationwide Accident Help provides free initial evaluations and works on a contingency basis, allowing you to build a solid case without upfront costs. By sticking to these steps, you can confidently counter lowball offers and work toward a fair settlement.

FAQs

What if I already accepted the low offer?

If you've already agreed to a low settlement offer, it’s generally considered a binding agreement, especially once payment has been made. Renegotiating under these circumstances is usually not an option. However, if you feel the settlement was unfair or you accepted it under pressure, it’s worth consulting a personal injury attorney. They can help determine if there are any legal avenues available to challenge the agreement. While most procedures make it difficult to reopen a claim after acceptance, an attorney can provide guidance tailored to your case.

How do I estimate future medical costs and lost income?

When planning for future medical expenses and lost income, start by keeping a detailed record of your current costs. This includes medical bills, therapy sessions, and medications. For lost income, tally up the workdays you've already missed and think about how your ability to earn might change in the future. It can help to consult a vocational expert to get a clearer picture of potential long-term income reductions.

Don't forget to account for non-economic damages like pain and suffering. These are often calculated using a multiplier, typically ranging from 1.5x to 5x your economic damages. Taking these steps ensures you're considering both short-term and long-term financial impacts.

When should I get help from Collision Help | Nationwide Accident Help?

If you’ve been in an accident and need help navigating insurance claims, vehicle repairs, or total loss disputes, Collision Help | Nationwide Accident Help might be worth considering. They offer a convenient nationwide service where you can securely upload photos of your vehicle's damage and receive expert guidance within 24 hours. Whether you’re dealing with a low settlement offer or complicated insurance concerns, their support can help you explore your options and work toward a fair outcome.